Related insights

- FX Tactical Ideas: US-Iran Ceasefire Flips USD Outlook10 Apr 2026

- Bangkok Dusit Medical Services10 Apr 2026

- Airports of Thailand10 Apr 2026

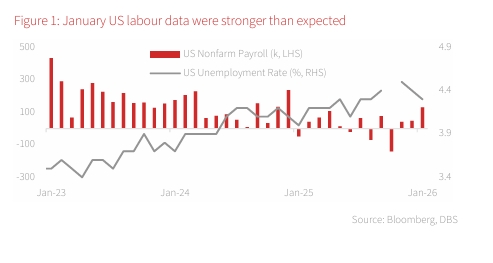

US/Japan: Firm US labour data dampens near-term Fed cut expectations; LDP lands landmark election victory. US nonfarm payrolls rebounded to 130k in January, doubling consensus expectations of 65k. The unemployment rate eased for a second month to 4.3% in January, from 4.4% in December and 4.5% in November. The data convinced Cleveland Fed President Beth Hammack that the stabilising labour market did not need additional rate cuts. Kansas Fed President Jeff Schmid wants the Fed to hold rates at a “somewhat restrictive” level because inflation remains above the 2% target. January’s headline and core CPI inflation are expected to converge at 2.5% y/y, down from 2.7% and 2.6% respectively in the previous month. Labour and CPI data are unlikely to alter the market’s belief that Warsh will deliver a rate cut at his first FOMC meeting as Fed Chair in June.

Shifting to Japan, the Liberal Democratic Party (LDP) secured a two-thirds supermajority in the lower house in the 8 Feb election, marking the largest post-war victory for a single party. This decisive outcome gives the government substantial latitude to enact major legislation with minimal resistance.

The Takaichi administration now has a clear mandate to pursue fiscal expansion. Market attention is focused on the proposed food consumption tax cut. Under the base-case scenario, the government is expected to implement the tax cut in 2H26. Reducing the food consumption tax rate to zero is estimated to lower CPI inflation by nearly 2 %pts, boost GDP growth by close to 0.5 %pts, and widen the fiscal deficit by approximately JPY5tn (0.8% of GDP). While earlier implementation at the start of the new fiscal year in April would require rapid legislative drafting, National Diet approval, and administrative system changes, this remains feasible given the LDP’s victory.

Beyond the consumption tax, the government is likely to prioritise passage of the FY26 general budget before the new fiscal year begins, revise long-term fiscal policy guidelines around mid-year, and prepare a FY26 supplementary budget later in the year. The FY26 budgets are expected to be expansionary, with an emphasis on stimulating growth, promoting investment in strategic industries, and supporting households. The revised long-term fiscal guidelines may place less emphasis on achieving an annual primary balance surplus, instead shifting toward a multi-year assessment framework.

With political uncertainty largely resolved, the Bank of Japan (BOJ) is expected to proceed with further policy normalisation. Under the base-case scenario, the BOJ is likely to raise rates by an additional 25 bps to 1.00% in June or July, after comprehensive Shunto wage data become available. The BOJ is expected to look through temporary GDP and CPI distortions from the food consumption tax cut in 2H26, focusing instead on potential growth and underlying inflation dynamics. This approach could open the door to another rate hike in Dec 2026 or early 2027.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- FX Tactical Ideas: US-Iran Ceasefire Flips USD Outlook10 Apr 2026

- Bangkok Dusit Medical Services10 Apr 2026

- Airports of Thailand10 Apr 2026

Related insights

- FX Tactical Ideas: US-Iran Ceasefire Flips USD Outlook10 Apr 2026

- Bangkok Dusit Medical Services10 Apr 2026

- Airports of Thailand10 Apr 2026