- Innovative drug license-out transactions to MNCs surged 161% to USD136bn in 2025

- The Hang Seng Innovative Drug Index rose c.79% in 2025, outperforming the Hang Seng Index by 44 %pts

- In Sep 2025, the US government drafted an executive order to impose tighter restrictions on the licensing-in of Chinese innovative drugs

- Bullish on “less Chinese” players

Related insights

- Research Library24 Feb 2026

- DACS: Lesser impact from US tariffs24 Feb 2026

- India markets: Cautious relief from US tariff ruling, domestics sway bonds24 Feb 2026

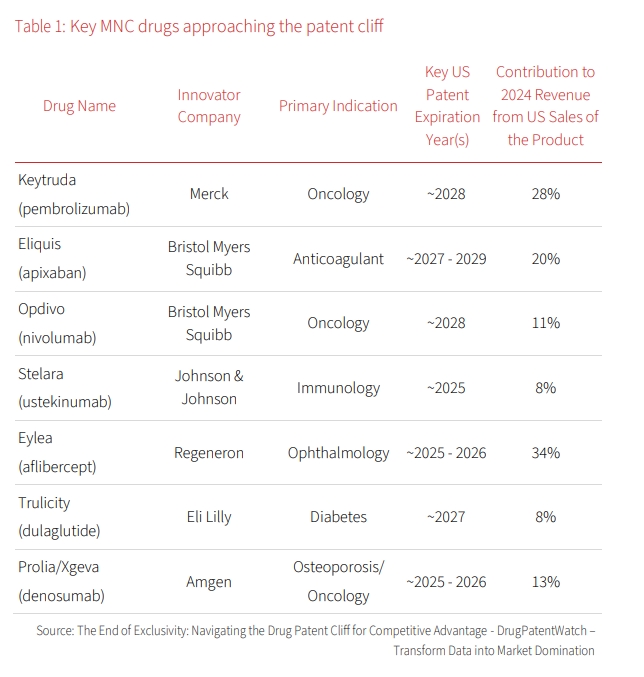

Innovative drug license-outs are expected to remain a key driver of sector performance. MNCs are increasingly seeking to replenish their drug portfolios through external innovation, as reflected in a y/y 161% surge in innovative drug license-out transactions to MNCs amounting to USD136bn in 2025. This lifted the Hang Seng Innovative Drug Index up c.79% in 2025, outperforming the Hang Seng Index by 44% pts. This trend is expected to continue as a large proportion of branded drug sales face patent expiry over the next five years. The US remains a critical target market given significantly higher drug pricing at >3x more than the rest of the world. White House data shows US buyers accounted for >40% of license-out deals last year.

Uncertainty around US license-ins of Chinese drugs. In Sep 2025, the Hang Seng Innovative Drug Index corrected the following news report that the US government was drafting an executive order to tighten restrictions on the licensing-in of Chinese innovative drugs (see: White House Officials Drafting Executive Order Enforcing Harsh Restrictions on Treatments Discovered in China: Report | PharmExec). Proposed measures include: 1) mandatory review by the Committee on Foreign Investment, a US national security body, for the acquisition of rights to China-based medicines; 2) discouraging the use of clinical trial data collected from patients in China; and 3) an increase in regulatory fees. These measures clearly target Chinese companies.

Prefer “less Chinese” players. With the US government targeting Chinese companies, we believe companies perceived as “less Chinese” carry lower risk. Key indicators could include: 1) production plant located in the US; 2) US-based auditors for financial reporting; 3) >50% long term assets held overseas; and 4) CEO, Chairman, and largest shareholders are US citizens or US-based entities.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Research Library24 Feb 2026

- DACS: Lesser impact from US tariffs24 Feb 2026

- India markets: Cautious relief from US tariff ruling, domestics sway bonds24 Feb 2026

Related insights

- Research Library24 Feb 2026

- DACS: Lesser impact from US tariffs24 Feb 2026

- India markets: Cautious relief from US tariff ruling, domestics sway bonds24 Feb 2026