- Venezuelan President Nicolas Maduro captured by US, facing charges of narco-terrorism conspiracy; “Monroe Doctrine 2.0”, which seeks to reassert US sphere of influence, in full effect

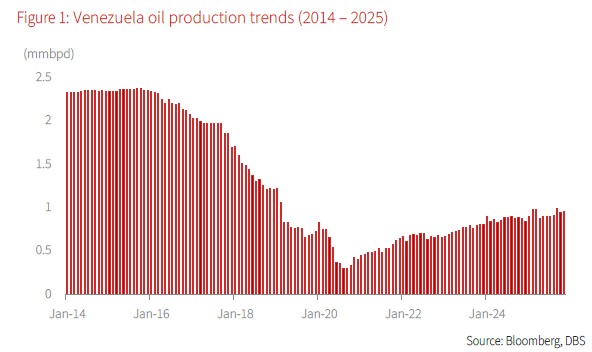

- Key aspect at play is Venezuela’s large oil reserves, though actual output has significantly declined, limiting any immediate global supply fears and geopolitical risk premium spikes

- Venezuela's oil is predominantly extra-heavy crude, requiring high oil prices and substantial investment for viability

- Long-term development of Venezuela's vast reserves is highly uncertain and unlikely to cause a substantial oil price crash even in the future

- Beneficiaries from the new era of US intervention and heightened geopolitical tensions include safe haven gold and defence contractors

Related insights

Another year, another armed conflict. Long-standing tensions between the US and Venezuela finally reached a tipping point this year; on 3 Jan 2026, the US launched military strikes on Venezuelan targets, capturing its president Nicolas Maduro and his wife in Caracas. Maduro has since been indicted in a federal court in New York and is facing charges of narco-terrorism conspiracy. Concurrently, Maduro’s former deputy Delcy Rodriguez has assumed leadership in Venezuela, though President Trump has announced that senior US officials will oversee an interim governance period until a safe transition is arranged. This operation confirms the “Monroe Doctrine 2.0”, reasserting America’s sphere of influence and accelerating a regional shift toward market-friendly governance. Reactions to this paradigm-shifting event have been starkly divided, with some critics, including Venezuela’s allies and other Latin American leaders, decrying the strikes as a clear violation of international law, while others have praised the downfall of an authoritarian regime. While the morality of the situation is subjective, the impact on markets is clearer; there is a clear reignition of regional (and perhaps global) geopolitical risk and that will have broader spillover effects on risk assets.

No significant short-term impact on oil prices. Seeing as how Venezuela holds the world’s largest proven oil reserves on paper – higher than Saudi Arabia (though this should be taken with a pinch of salt, as explained later) – oil is perhaps the most logical place to begin our analysis. Will the conflict in Venezuela move the needle when it comes to oil prices? Years of mismanagement, underinvestment, and sanctions have reduced Venezuela’s output to a fraction of historical levels, and it is no longer a significant player in global oil supplies. In the short term, we do not think there will be direct material impact on global crude supply amid current oversupply trends, but risk premiums could inch up along with higher volatility – amounting to a spike of up to 10% before re-adjusting. For now, our view on oil prices remains – rangebound at USD60-65/bbl levels for Brent in the near term. Nonetheless, Venezuela’s heavy crude grade is difficult to replace in certain refining processes, so prolonged disruption could tighten specific refined product markets like diesel and jet fuel.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.