- REEs have emerged as one of the most strategically important materials of the decade, positioned at the nexus of industrial transformation, technological competition and geopolitical realignment

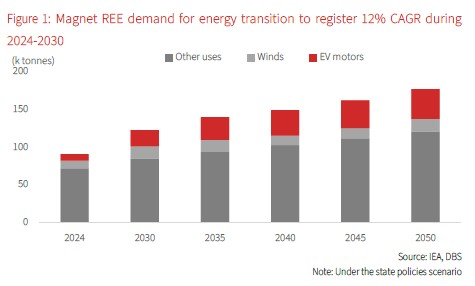

- The demand for REEs is projected to accelerate across advanced technology sectors – energy transition, defence, and AI infrastructure

- China’s overwhelming control of REE supply chain is creating increasingly glaring structural imbalances

- The rest of the world is likely to invest heavily moving forward, though challenges are expected due to the relative lack of scale and cost efficiencies compared to China

- REE’s indispensable role in technologies shaping the future of global order and supply constraint concerns should reinforce their compelling investment narrative

Related insights

- Asia ex-Japan Equities02 Mar 2026

- Research Library02 Mar 2026

- USD Rates: Caution warranted02 Mar 2026

Scarcity and strategic importance drive value. Rare earth elements (REEs) are a group of 17 metallic elements with unique magnetic, battery, and electronic efficiency and thermal properties. REEs have emerged as one of the most strategically important materials of the decade, positioned at the nexus of industrial transformation, technological competition, and geopolitical realignment. As the global economy accelerates electrification, digitalisation, automation, and defense modernisation, demand for REEs is set to grow significantly across advanced technology sectors.

Indispensable role of permanent magnets in modern technology. One of the primary applications of REEs are production of high-performance rare earth magnets – made up of neodymium, praseodymium, and a small amount of dysprosium and terbium. These magnets are crucial to modern technology, including EV motors, wind turbines, defence systems, medical equipment, data centre, and consumer electronics.

Strategic position of REEs in the defence industry amid rising geopolitical risks. While defence and AI infrastructure may not currently represent the largest segment of REE demand, their strategic importance to these sectors is poised to drive significant growth in the foreseeable future. China’s export restriction, albeit at a one-year pause, has spurred notable actions from other countries such as the investment by the US Department of Defence (DoD) in a fully integrated domestic rare earth company for national security purposes. The move has underscored the indispensable role of REEs in the defence industry.

Specifically, REE elements, not limited to those used in magnets, possess unique properties vital for advanced defense technologies. This encompasses a wide range of applications, such as precision-guided missiles, highly sensitive radar and resilient communication systems, advanced drones, and next-generation military aircraft and aerospace platforms.

Critical enabler in AI infrastructure. Every part of the AI supply chain – from data centres to semiconductor and chip-making equipment – use rare earths. Data centres use magnet REEs in hardware, cooling, and power, and erbium and ytterbium in fibre optics networks for optical amplification. Semiconductors rely on REEs for polishing, chip performance, and critical manufacturing equipment like lithography machines, vacuum systems, and robotic controls. Hence, as the world races for AI superiority, rare earth elements will remain a critical enabler at the heart of AI cycle.

Constrained supply - entrenched bottlenecks and structural fragility. The global rare earth supply chain remains heavily concentrated, with China maintaining its dominance across every major stage for magnet REEs – mining (59%), refining (91%) and magnet manufacturing (94%). This dominance is not merely a function of resource endowment, it reflects decades of vertically integrated development, technological expertise, state-directed industrial policy, and willingness to absorb environment externalities. China's established dominance in the rare earth market and its recent use of this position as a diplomatic tool, exemplified by export controls, have compelled other nations to recognise the critical nature of REEs and urgently pursue strategies to reduce their reliance on China.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Asia ex-Japan Equities02 Mar 2026

- Research Library02 Mar 2026

- USD Rates: Caution warranted02 Mar 2026

Related insights

- Asia ex-Japan Equities02 Mar 2026

- Research Library02 Mar 2026

- USD Rates: Caution warranted02 Mar 2026