Related Insights

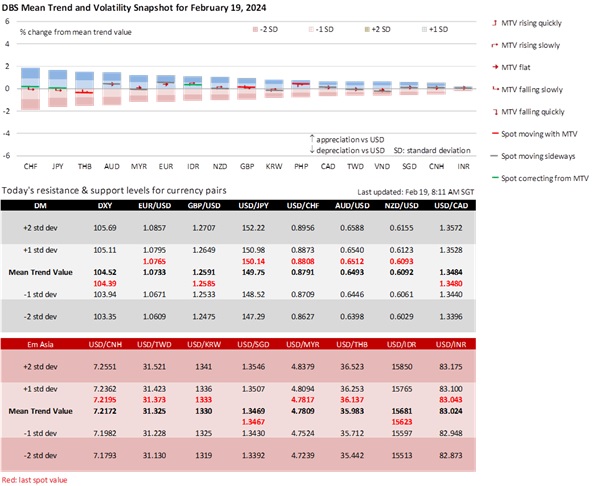

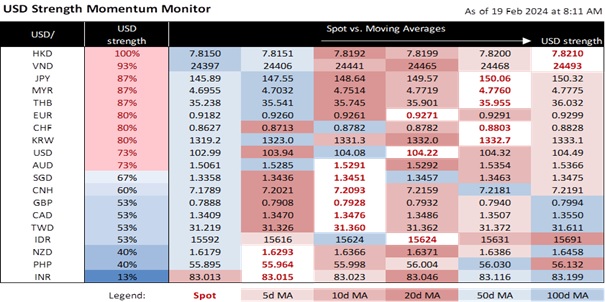

DXY appreciated by 0.2% to 104.28 last week, closing above its 100-day moving average for the first week since mid-November. Fed officials are adhering to their forecast of three rate cuts in December’s Summary of Economic Projections. The US calendar is light in terms of data, focusing mainly on Fed events, especially the FOMC minutes on 21 February. Seven Fed officials are scheduled to speak on Wednesday-Friday. They are Vice Chair Philip Jefferson, Governors Michelle Bowman, Lisa Cook, and Christopher Waller, and Presidents Raphael Bostic (Atlanta), Patrick Harker (Chicago), and Neel Kashkari (Minneapolis). Unless they sound overly hawkish, Fed officials have already pushed back against the market’s aggressive rate cut bets. Since mid-December, interest rate futures have pulled back their stakes from seven to four cuts this year, and for the first reduction to start in June instead of March.

Hence, DXY did not push above 105 last week when the US 10Y bond yield was capped at around 4.33% or its 100-day moving average. Japanese officials also stepped up verbal intervention with USD/JPY above 150. On the other hand, the market is not rushing to dump the greenback ahead of possible surprises in next week’s PCE deflators. Moreover, the US economy has proven resilient compared to the technical recessions in Japan and the UK amid underwhelming growth in other economies. Meanwhile, China returns from its week-long Lunar New Year holidays. Investors are still holding out for more stimulus measures despite the skepticism over the Chinese economy.

EUR/USD remains pressured below 1.08. The European Central Bank is divided over whether to cut rates too soon or too late. ECB member Francois Villeroy de Galhau (France) preferred gradual cuts over waiting too long to cut rates. Eurozone GDP growth has been stuck in a ±0.1% QoQ sa range for five quarters into 4Q23. The European Commission downgraded this year’s GDP growth outlook to 0.8% from its autumn forecast of 1.2%. On the other hand, ECB President Christine Lagarde and member Isabel Schnabel (Germany) did not want to rush rate cuts for fear that inflation may rebound. With wages becoming an important driver of inflation, the ECB will wait for the Eurozone wage talks to conclude after the April meeting to determine if it could start cutting rates in summer. At 2.8% YoY and 3.3% in January, headline and core inflation were still too high above the 2% target.

GBP/USD is hemmed between 1.25 and 1.2650 this week with a downside bias. With the UK economy in a mild technical recession and the Tory Party losing two significant by-elections over the weekend, expect more pressure on the Bank of England to lower interest rates. Real GDP contracted by 0.4% QoQ sa in 4Q23 after declining 0.1% in 3Q23. However, retail sales turned positive by 3.4% MoM in January from its -3.3% growth in December, suggesting a short-lived downturn. Over the weekend, BOE Chief Economist Huw Pill wanted several months of data to be sure inflation was on its way to the 2% target before considering rate cuts. Although CPI inflation fell 0.6% MoM in January following a 0.4% rise in December, headline and core inflation were high in YoY terms, at 4% and 5.1% in December. Do not expect Chancellor of the Exchequer Jeremy Hunt to dole out generous tax cuts at the Budget announcement on 6 March. Hunt is constrained by the reduced fiscal headroom provided by the Office for Budget Responsibility (OBR) forecasts and the IMF pushing the UK towards the path of fiscal consolidation.

Quote of the day

”Men are not the enemy but the fellow victims. The real victim is women’s denigration of themselves.”

Betty Friedan

19 February in history

In 1963, American author and activist Betty Friedan published The Feminine Mystique, a landmark work that was a catalyst for the second-wave feminist movement.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.