- Policy support to capital markets has fostered China brokers’ growth profile in the medium term

- Favour China brokers over US peers given multi-year growth opportunities and more favourable liquidity conditions

- Regulatory overhang on Chinese online brokers largely removed; global expansion the next key growth driver

- Key catalysts include strong retention of existing customers and room to capture overseas Chinese clients

- While higher rates and macro uncertainties remain, prefer players with a more diversified business mix and stronger balance sheet

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

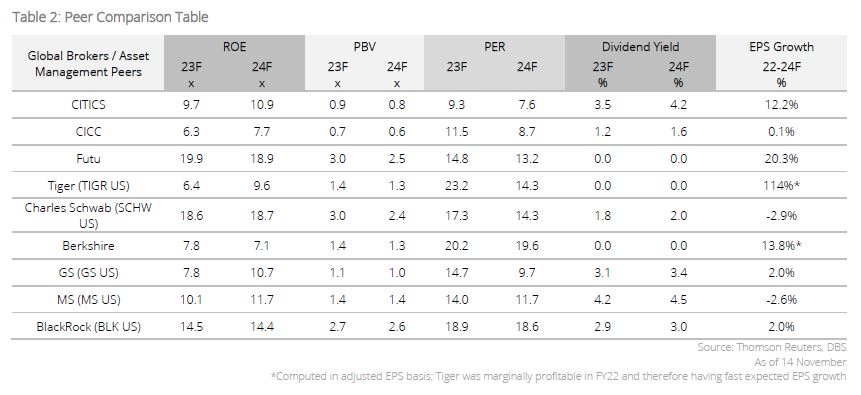

China brokers undervalued vs US peers; expect gap to narrow driven by favorable policy, liquidity support and structural ROE expansion. Policymakers have committed to revitalising the capital market since the Politburo's meeting in July. Key initiatives taken include cutting the stamp duty for equity trading by half, enabling higher market leverage, and promoting long-term funds to raise equity allocation. Despite these concerted efforts, the anticipated benefits have yet to materialise as the equity investing sentiment has remained lackluster, primarily influenced by the prevailing uncertain macro outlook.

While the fade of initial enthusiasm led to significant correction of the sector from the peak in August, we think that presents an opportune entry point for investors, considering (1) the more attractive risk-reward profile, (2) further signs of bottoming out from macro indicators, and (3) the more concrete effort implemented from policymakers.

In particular, the recent relaxation of capital leverage ratio is expected to enhance capital utilisation of top-tier brokers, leading to a medium-term return on equity (ROE) expansion and narrowing the gap vs foreign peers. We favour China brokers over their US peers, considering (1) the multi-year growth opportunities from policy support, (2) more favorable liquidity conditions under lower interest rates, and (3) significantly cheaper sector valuations.

A new chapter for Chinese online brokers; global expansion as next key growth driver. The rectification process for online brokers since early this year has largely come to an end, as signalled by the Chinese regulators’ on-site acceptance of Up Fintech’s final remediation report in mid-July. It is also encouraging to see (1) strong retention of existing customers as per the robust net asset inflows recorded in 1H23, and (2) room to capture overseas Chinese clients, as the regulator clarified that PRC citizens living or working overseas remain eligible to be served by offshore-licensed brokers. Those with stronger profitability also seized the quieter window to broaden their geographical exposure while smaller peers struggle, putting themselves in a better position to capture a potential market rebound.

Challenging macro backdrop for global diversified financials. Many global brokers and asset managers find themselves at a disadvantage in the current higher-for-longer interest rate environment. They grapple with challenges such as diminished inflows in AUM, a shift towards money market funds, dealmaking slump, and reduced equity trading income.

Seek players with more diversified business mix and stronger balance sheets. In this environment, we believe players with a more diversified business mix and stronger capital strength are better positioned to outperform. The smoother earnings volatility should help them navigate the rapidly evolving landscape, and the stronger balance sheet should enable them to seize potential M&A opportunities and further consolidating market share, especially if there is a dip in asset valuations.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024