- Global and Chinese ERP players registered decent revenue growth in the recent earnings season despite prevailing macro headwinds

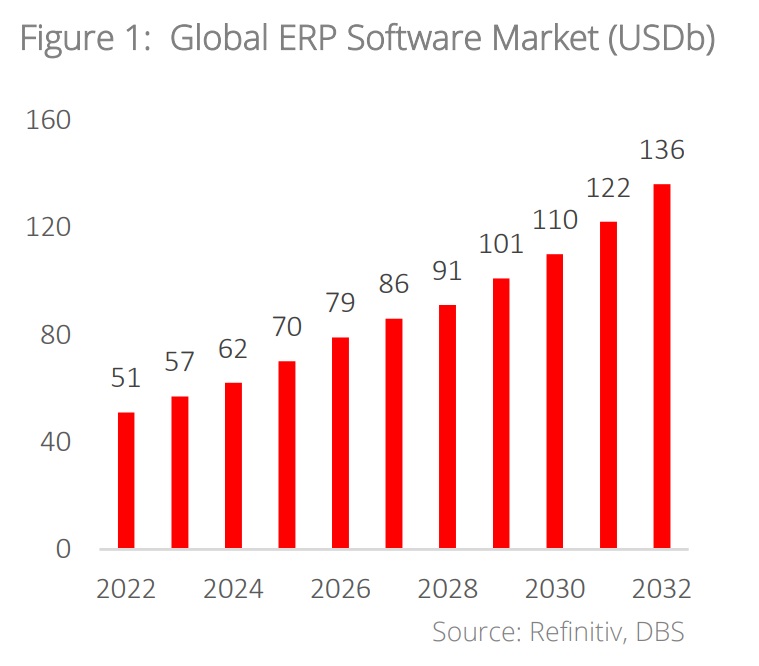

- Global ERP market projected to grow at 11% CAGR in the medium term; ERP is less susceptible to economic cycles and IT budget reductions given its importance to core company operations

- China ERP market to enjoy stronger CAGR of 15% given low ERP penetration rate and localisation trend

- Global ERP players are currently trading at 5-10x forward P/S (price-to-sales) and this is similar to historical average

- Chinese ERP players are trading at 5x P/S, one standard deviation below their historical average; this reflects slower growth during city lockdowns as well as company restructuring

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Global ERP industry registered decent growth despite economic headwinds. In the Global IT Outsourcing industry, growth of the Enterprise Resource Planning (ERP) segment correlates closely with enterprise IT spending and the overall economic environment. Global ERP names reported y/y revenue growth ranging from 5% to 12% in their latest quarterly results, underpinned by c.20% growth in their cloud ERP business segments despite economic challenges.

Furthermore, these global ERP companies have recorded robust earnings growth ranging from 12% to 50%, thanks to improved operating efficiency. In the case of China, while one of the domestic leaders has recently undergone organisational restructuring, the other key leading player has managed to achieve impressive 17% y/y revenue growth, buoyed by 22% growth in its cloud ERP segment.

Looking ahead, global ERP companies are expected to sustain their business momentum and they are targeting to achieve full-year revenue growth like their recent quarterly numbers. For the Chinese players, while they do not offer specific guidance, we anticipate stronger business growth in 2H23, driven by favourable policies supporting enterprise digitalisation and localisation.

Expect sustainable growth amid resilient ERP demand. Growth of the ERP market is expected to be more resilient than other software applications and public cloud services. ERP tools are vital during and after the pandemic for core company operations, such as financial reporting and employee performance tracking. For instance, while public cloud demand has waned post-pandemic, the ERP space has remained resilient, rendering them less susceptible to economic cycles and IT budget reductions.

We expect sustainable growth for the ERP market as it rides on the global enterprise digitalisation trend given strong business reliance on ERP to enhance operational efficiency and make data-driven decisions. Grand View Research expects the market to register CAGR of 11% from 2023 to 2030.

China ERP market to enjoy faster growth amid low penetration and localisation trend. China accounts for c.4% of the global market and is poised to deliver 15% CAGR growth, surpassing the global average of 11%. ERP adoption in China stands at c.25%, lower than the 40%+ observed in mature markets like Europe and the United States. In recent years, the Chinese government has enacted policies to encourage enterprise ERP digitalisation (e.g. tax benefits) and to promote software localisation, which aim to bolster adoption of domestic software. Key domestic players, Kingdee and Yonyou, have been gaining market share from foreign ERP incumbents and this trend is expected to persist in the years ahead.

While China’s ERP sector enjoys faster growth, we are also expecting steady growth for global ERP companies given their diversified geographic reach. On balance, improvement in the global economy and by extension, global IT spending, will support re-rating for both global and Chinese ERP players.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024