Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

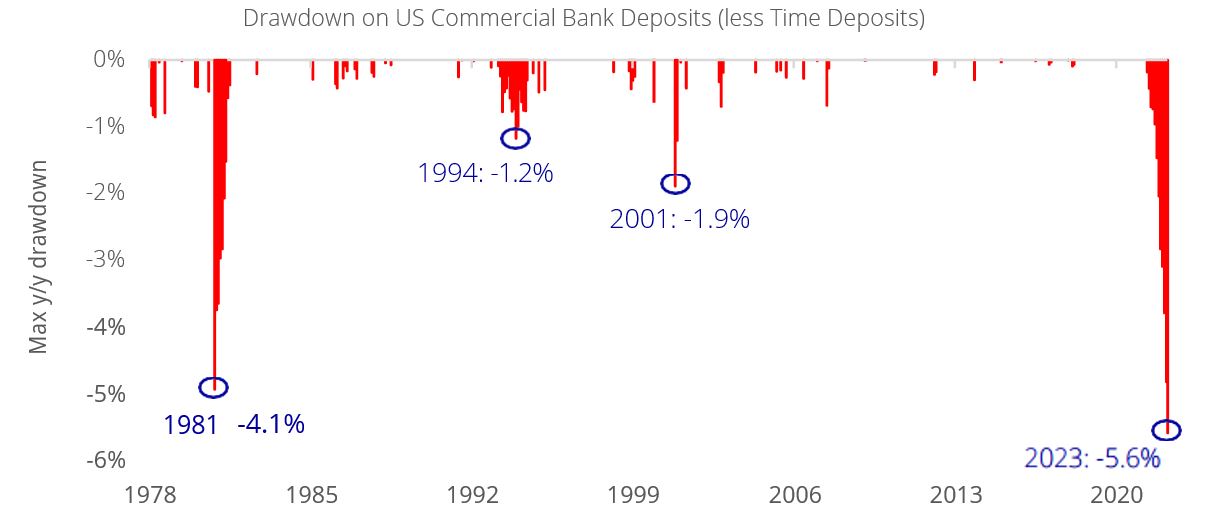

Cash can only be king when its palace is secure. Nothing agitates the markets quite as much as the news of failing banks, given how conditionally the financial system relies on confidence and confidence alone. From the likes of the Silicon Valley, Signature, and First Republic banks in the US, to Credit Suisse across the Atlantic, investors who have been in the market long enough would feel an eerie chill reminiscent of the years leading up to the GFC in 2008. Yet it isn’t just risk-adept investors feeling the nervousness; even risk-averse depositors are taking strides to ensure that their savings are not under threat from a banking crisis. Notably, 2023 saw the largest year-on-year drawdown in US commercial bank deposits (less the stickier large time deposits) in decades, dwarfing even that of the 1981 Volcker-era decline.

Figure 1: 2023 bank run is the worst deposit y/y drawdown since the Volcker era

Source: Bloomberg, DBS

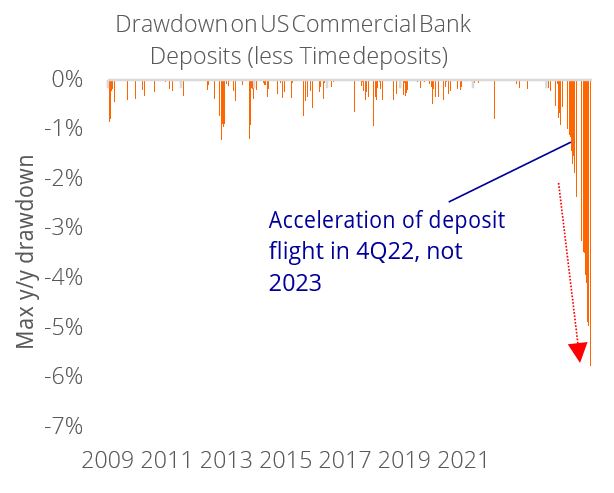

From bank run to bank sprint. While it is easy to blame the banking crisis for the dearth of confidence, the data shows that the acceleration in deposit outflows had already begun months before the bank failures over the past weeks. In the age of proliferation of banking and investment mobile apps, along with broader virality through social media, bank runs become more like bank sprints. Case in point – Washington Mutual failed when depositors attempted to withdraw c.USD17b in deposits over nine days in 2008. That same amount was gone from Silicon Valley Bank within just half a day.

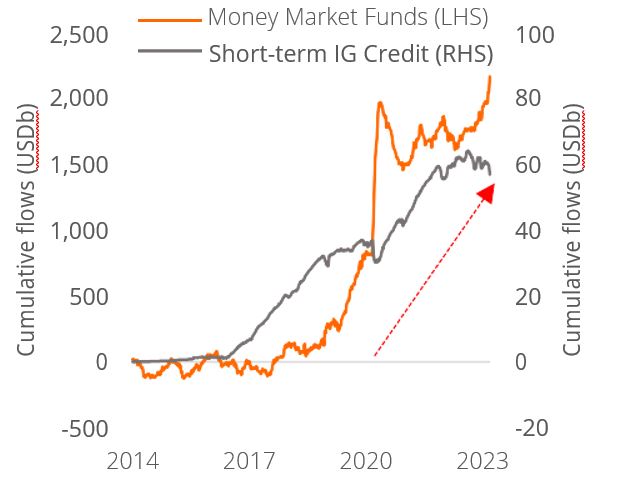

Figure 2: Money flowed from deposits to Money Market/Quality credit funds

Source: Bloomberg, EPFR Global, DBS

Where has all the money gone? Yet money can’t just disappear. Flow of funds data showed that the markets have flocked towards cash-proxies – either with Money Market funds or high-quality, short duration credit funds. If that sounds familiar, it is because that is precisely the premise of our Liquid+ Strategy – that investors are better off being well-diversified in safe and liquid assets as the world navigates a tricky environment of stubborn inflation , slowing growth, and rising uncertainty . We see the flow of funds data as affirmation that we are not alone in this line of thinking.

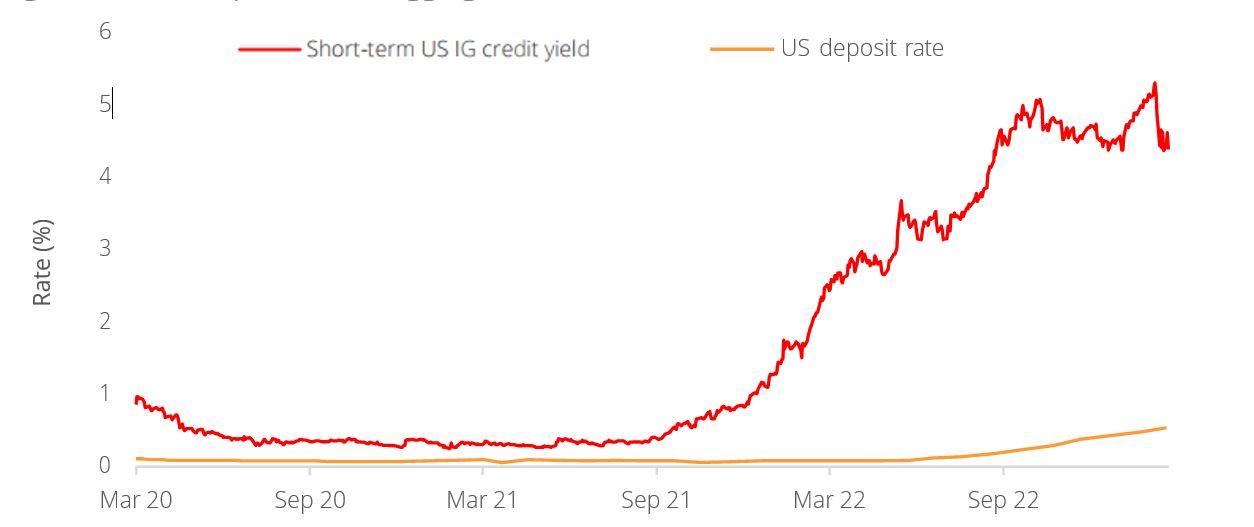

Figure 3: Cash deposit rates lagging far behind other safe alternatives

Source: Bloomberg, FDIC, DBS

Go with the flow. This flow of funds from deposits to fixed income could still have legs. As we stand, such safe alternatives are yielding between 4-5%, a far cry from the average rates on jumbo deposits of 0.5-1%, according to the US Federal Deposit Insurance Corporation. The moment the market realises that we are nearing the end of the rate hike cycle, the demand for longer duration fixed income assets would surely accelerate the flows that we are already seeing in the markets over the last several months. It might be true that deposit rates would rise in tandem to compete for demand for funds, but as we are already seeing signs of banking stress, such higher deposit costs of funding would hurt bank profitability, which does not instill the confidence from depositors that they should remain concentrated in their exposure to the financial sector, given the stresses that banks are already facing today.

Stay with the Liquid+ Strategy. The track record for markets trying to perfectly time peaks and troughs is abysmal. As such, rather than trying to catch the peak in interest rates to fully switch into fixed income, we believe investors should start to progressively switch excess liquidity into these cash alternatives in order to (a) obtain a higher yield while they are available, and to (b) diversify away from concentration risk in bank deposits while the financial sector faces strain. As they say, better late than never.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related Insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024