- Positive on the US data centres space as stable profitability underpins rising dividends over the years

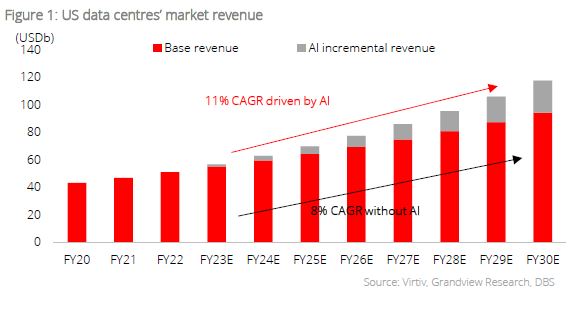

- US data centres to register 11% CAGR from FY23 to FY30 as result of AI advancement

- China’s data centres industry to grow 15% in FY24 amid stabilising domestic cloud businesses

- Longer-term, the China public cloud market is expected to deliver 32% CAGR in the next five years

- Expect US names to outperform Chinese peers given positive market conditions and dividend merits

Related Insights

US data centres possess strong track record of stable dividends. In the 4Q23 earnings season, US data centres reported y/y growth in adjusted EBITDA ranging from 9% to 10% as result of higher rental rates. Looking ahead, we are bullish on this space given:

- US data centres have consistently been increasing dividends as profitability is underpinned by stable net profit margins of 7-10%

- The market is set to accelerate with AI advancement, with US operators seeing rising AI demand (in contrast, China’s data centres industry is hampered by the lag in AI commercialisation)

US data centres industry growth to hit 11%, buoyed by advancement in AI. According to Grandview Research, the US data centres industry is expected to register 11% CAGR from FY23 to FY30 (surpassing the 8-9% growth in FY21 and FY22) as a result of AI advancement. The largest carrier-neutral operator in the US stated that AI will account for 15% of data centres’ total addressable market (TAM) of USD140b in 2026. Moreover, research firm Dell’Oro is also predicting stronger data centres infrastructure growth in the coming years.

The US, being an early mover in AI development, has seen many of its software companies incorporating AI capabilities into their offerings since early last year. According to Preqin, US leads the way in AI investment, drawing USD26.6b in 1H23 (vs USD4b in China).

China’s data centres industry: Cautious optimism. The China data centres industry is expected to deliver 15% growth in FY24 and the overall subdued momentum is attributed to slower business demand for domestic public cloud service providers (who are major end-users of data centres). But longer-term, the China Academy of Information and Communications Technology (CAICT) believes that the China public cloud market will register 32% CAGR in the next five years and this supports the longer-term growth trajectory of data centres’ TAM.

We believe investor sentiment in this space will gradually improve given (1) Prevalence of a steady market outlook and (2) Operators’ commitment to deleverage (for instance, the largest carrier-neutral data centre operator in China is aiming to lower the net debt/adj. EBITDA for its China business to

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.