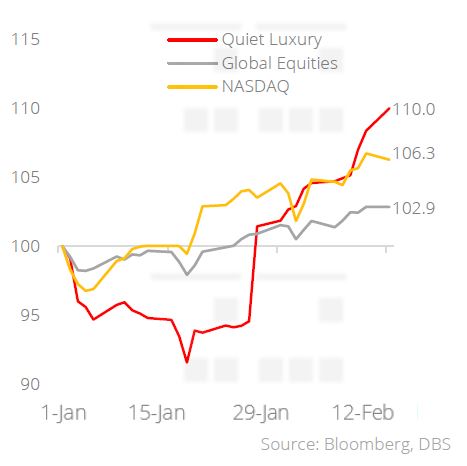

- Quiet Luxury companies have outperformed Nasdaq and Global Equities by 3.7% and 7.1% respectively this year

- The shift towards Quiet Luxury is underpinned by (a) Emergence of uneasy affluence, (b) Changing demographics, and (c) Shift towards sustainability

- Quiet Luxury companies’ operating margin of 17.8% surpassed global equities’ 12.8% margin; Earnings outlook is equally impressive with CAGR of 9.8% for FY23-24

- Demand for Quiet Luxury stays resilient as customers are less impacted by inflation and interest rates

- China’s luxury market showing early signs of rebound and this provides further positive momentum for the industry

Related Insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Consumers gravitating towards Quiet Luxury. Consumers are increasingly drawn to brands that resonate with their refined lifestyle preferences and values. The shift towards Quiet Luxury can be broadly attributed to the following factors:

▪ Emergence of uneasy affluence: Rising wealth gap and the cost-of-living crisis have pushed the affluent towards adopting Quiet Luxury and avoiding ostentatious displays of wealth.

▪ Changing demographics: Younger consumers are increasingly drawn to Quiet Luxury brands that reflect their values and offer a more meaningful luxury experience. These brands focus on heritage and craftsmanship while avoiding overt status symbols.

▪ Shift towards sustainability: The demand for sustainable and ethically produced goods is on the rise. This trend aligns with the broader shift towards environmental responsibility, making luxury brands that prioritise sustainability, craftsmanship, and durable materials more appealing than ever.

Which are the key Quiet Luxury companies? The recent earnings season continues to paint a picture of resilience for Quiet Luxury names whose customers are less impacted by inflation and interest rates. China’s luxury market is also showing early signs of rebound and this provides further positive momentum for the industry. Listed below are the key Quiet Luxury companies and their medium-term outlook:

▪ Hermès International (RMS FP):

▪ Often regarded as the preeminent Quiet Luxury brand, Hermès has always maintained a signature style that is both elegant and understated.

▪ In the recent earnings season, Hermès posted 4Q revenue of EUR3.36b (up 17.5% y/y), beating expectations of EUR3.26b. Hermès’s shares rallied c.6.1% last Friday (9 Feb) after earnings release.

▪ Management Outlook: “In the medium-term, despite the economic, geopolitical, and monetary uncertainties around the world, the group confirms an ambitious goal for revenue growth at constant exchange rates…” (Axel Dumas, Chief Executive of Hermès)

▪ LVMH – Moet Hennessy Louis Vuitton (MC FP):

▪ As the leading luxury conglomerate, LVMH boasts an impressive portfolio of 75 brands spanning five segments. This diverse range of high-end brands positions LVMH at the forefront of the luxury industry, catering to a wide array of preferences. In the recent earnings season, LVMH reported sales of EUR86.2b for the whole of 2023 (up 9% y/y), in line with analysts’ estimates. LVMH shares rallied c.13.9% on 26 Jan, after earnings release.

➢ Management outlook: “Regarding the size of stores in China … there are twice as many Chinese customers as in 2019… It means that the domestic purchase in China has grown significantly, so we have to meet that…” (Bernard Arnault, Chairman and CEO of LVMH)

Quiet by design, solid in fundamentals. On balance, we expect Quiet Luxury stocks to maintain positive momentum given their economic moat qualities and robust financials:

▪ Premium margins: While the global luxury industry already possesses a higher operating margin (OPM) than global equities (14.1% vs 12.8%), the Quiet Luxury segment boasts an even more impressive OPM of 17.8%. This underscores the premium pricing Quiet Luxury companies can command.

▪ Impressive earnings outlook: Quiet Luxury companies in the Bloomberg Global Luxury Goods Index are expected to register average revenue CAGR of 9.8% in FY23 and 24, surpassing the broader market's 8.0%.

Figure 1: Quiet Luxury’s outperformance

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025

Related Insights

- Airbus SE17 Dec 2025

- Indonesia 2026 Outlook: Time to deliver16 Dec 2025

- FX Quarterly 4Q 25: A Lame Duck USD15 Dec 2025