- Short-term rates have hit a steady statein the US and Eurozone while long-termrates have yet to settle

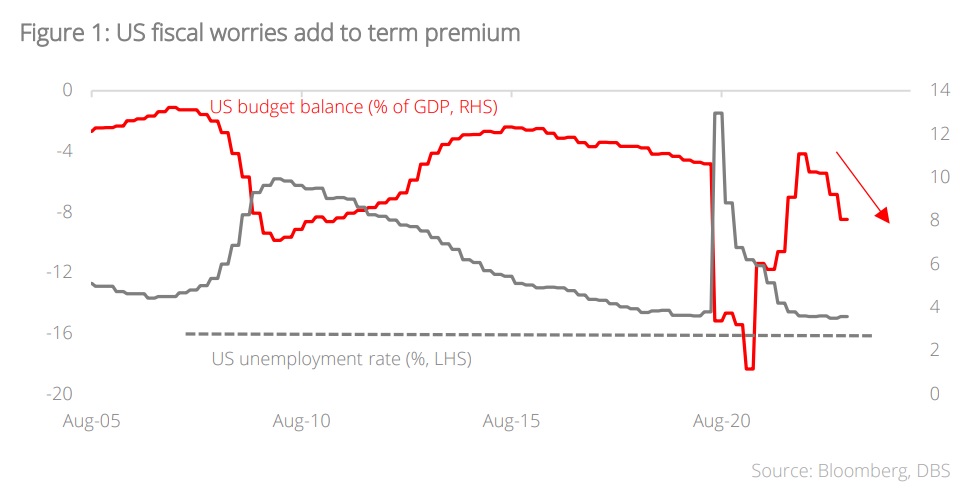

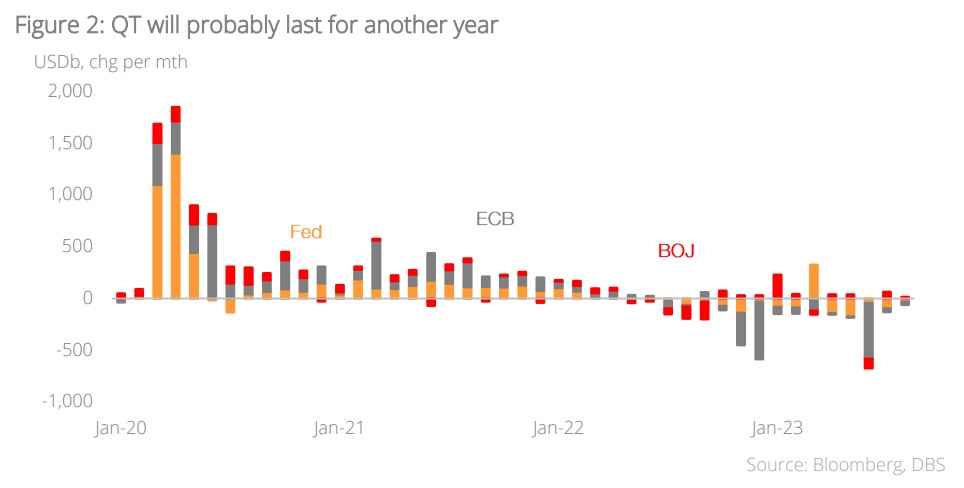

- All else equal, the private sector willhave to finance an increasing amount ofgovernment debt; QT will likely persistfor another year or more

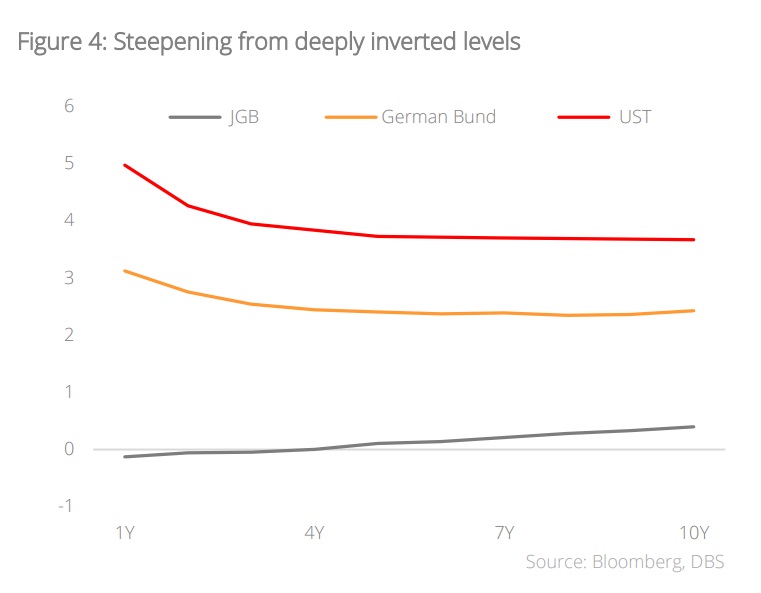

- Greater term premium should beaccorded to the longer-tenors

- We prefer the safety of shorter durationgovvies (2Y out to 5Y), noting that thebulk of tightening is done for the Fedand ECB

- Curve steepening the most likelyscenario; a burst of bear steepeningtook place in recent months but thatcould shift into bull steepening when adownturn becomes clearer

Related insights

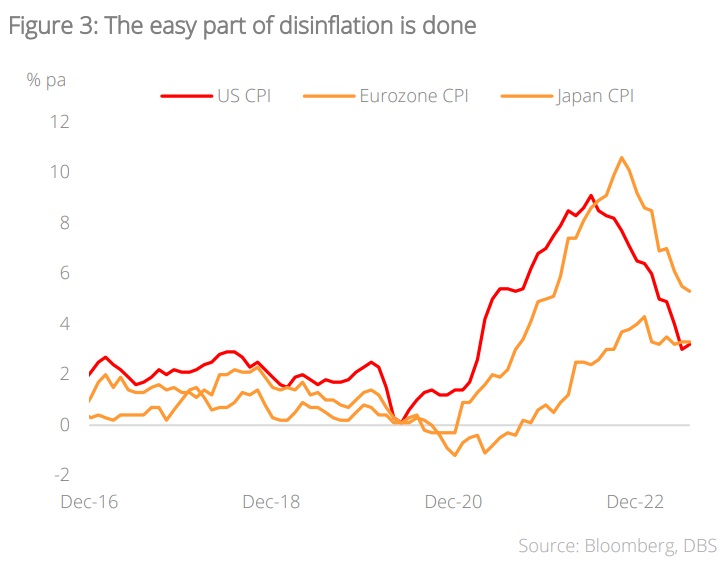

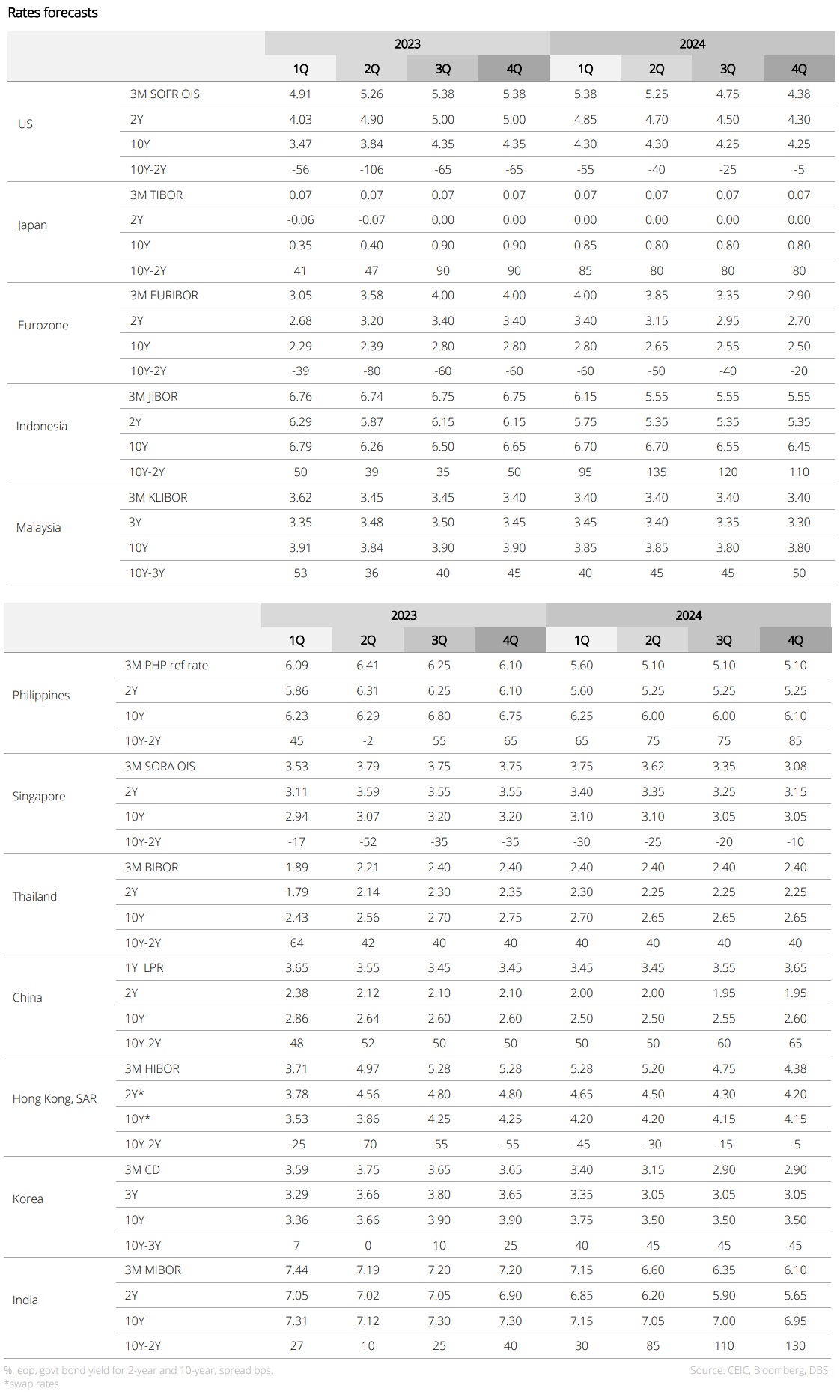

DM interest rates finding a new neutral suited for a volatile environment in the coming years. Cyclically, the Fed and the ECB are probably near to, if not already, at the end of their respective tightening cycles. The Fed and the ECB have already delivered 525 bps and 425 bps of hikes in the current cycle. While the door for further tightening has not been closed, it does seem that policymakers have shifted towards a more balanced outlook. If our view is right, upside to 2Y tenors for UST and EGB should be capped. Within the G3, only the BOJ is seen to still be lagging the rest of the world in dealing with inflation. However, as slow as the BOJ is, it still tightened twice in the cycle, with the 10Y JGB yield cap now set at 1%.

Longer-term rates figuring where to settle as short rates hit a steady state in the US and Eurozone. Fears of a recession were mostly acute for the past few quarters, and this has been reflected in the inversions seen in the US Treasury and German Bund curves. Between jumbo-sized hikes across multiple central banks, stresses in the banking sector, and US debt ceiling woes, investors were concerned about downside risks to the economy and Fed cuts. However, the focus has since shifted to economic resilience, higher-for-longer rates, sizeable US Treasury issuances, and less distortions from the BOJ (allowing the market to play a greater role in determining 10Y JGB yield). We should also be cognisant that QT is still ongoing for the Fed and ECB. All else equal, the private sector will have to finance an increasing amount of government debt. QT will likely persist for about a year more. A minor economic shock (that necessitates a few rate cuts) will probably be insufficient for the Fed or ECB to pause QT. All these suggest that greater term premium should be accorded to the longer-tenors.

We prefer the safety of shorter duration govvies (2Y out to 5Y), noting that that the bulk of tightening is done for the Fed and ECB. With yields in those tenors already elevated (not pricing in too many cuts), these tenors can be a safety play should things go awry for the global economy. Conversely, there are a lot more factors to consider for the longer end. Curve wise, we still see steepening as the most likely scenario. A burst of bear steepening took place in recent months, but that could shift into bull steepening when a downturn becomes clearer.

Asia Rates

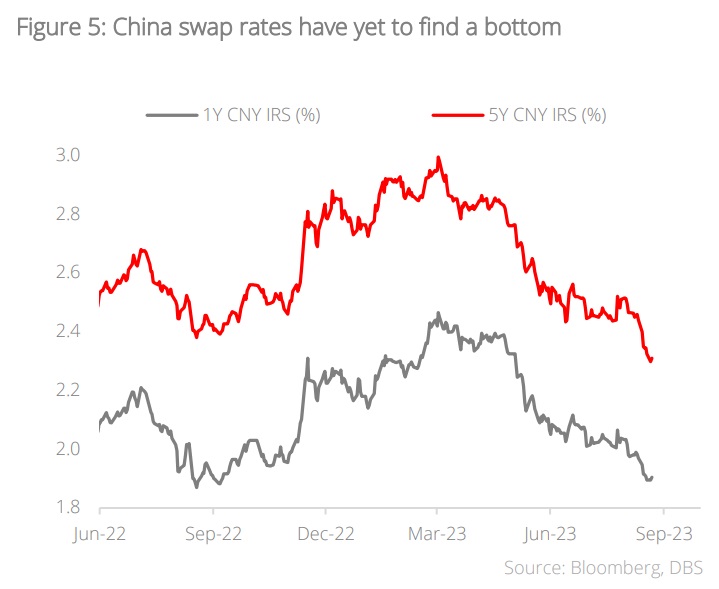

CNY rates: Bearish sentiments on growth

Sentiment towards China outlook remains quite bearish, as economic data continues to disappoint and negative news flow (around property developers and trust companies) creates worries of financial contagion. Policymakers continue to make pledges of economic support. If support remains skewed towards further rate cuts (OMO/MLF/LPR/deposit/ mortgage rates), then IRS rates could fall further. If support pivots towards fiscal (e.g., increasing special LGB issuances) or significantly props up the property sector, it would be easier for IRS rates to find a bottom. Our base case is for CNY Rates to stay stable at current low levels with modest upside room. Liquidity appears to be sufficient but not necessarily flush – 7D Repo fixings are not as low relative to OMO rate, compared to the 2Q-4Q22 period. If we get more liquidity injections to ward off contagion risks, fixings could push lower.

IDR rates: Limited scope for duration to rally

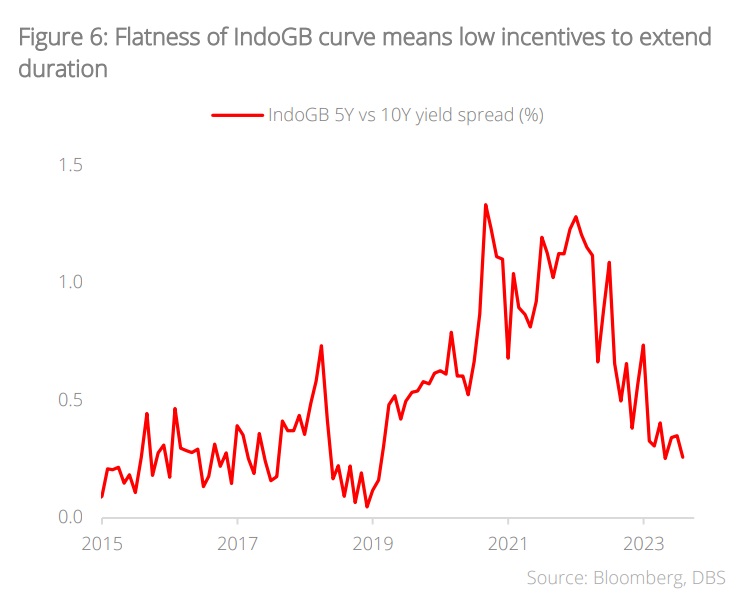

BI unlikely to signal rate cuts as uncertainty on peak Fed rates remains. 10Y IndoGBs are no longer as attractive – the following factors are likely to maintain a relatively high level of 60-80% passthrough from 10Y US Treasury yields. One, a supported US dollar/depreciating IDR would drive a wider FX risk premium and international investors would require higher IndoGB yields to compensate. Two, from a valuation perspective, 10Y IndoGB-UST yield differential should be considered as rich and stretched, and therefore, biased to re-widen. Three, specifically for domestic investors, the case to buy long-tenor IndoGBs is quite weak due to the flatness of the curve and low prospects for near-term BI rate cuts. We think 10Y IndoGB yields would need to further steepen relative to front-end yields (0-3Y) by at least 30 bps, for local investors to generally turn more in favour of extending duration.

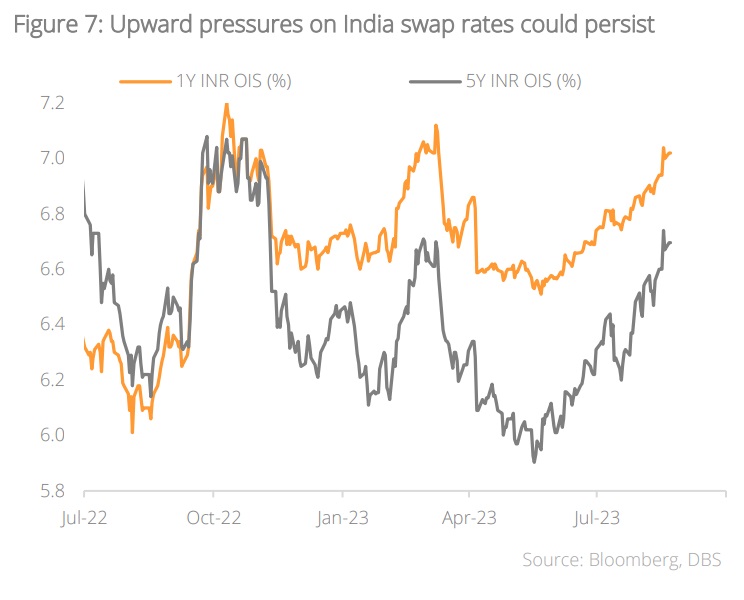

INR rates: Heavy bond supply and volatility in food prices

RBI has acknowledged that the recent firming in food prices would significantly push up near-term inflation prints, but for now, expects inflation to peak in the July-September quarter and moderate in subsequent quarters. However, if price shocks turn out to be more recurrent or persistent, the RBI affirms that it stands ready to hike rates further to anchor inflation expectation. With July and August CPI printing above the top of the RBI’s target range for inflation, we expect OIS curve to be pricing for high chance of hike (more than 50%) at the next Monetary Policy Committee meeting in October. Indian Government Bond supply continues to be heavy and with near-term worries of volatility in food prices, OIS rates could face further upward pressures. Externally, higher US rates also exert a larger passthrough to OIS rates, compared to other regional swap markets. Tactically, any dips in OIS rates could present good risk-reward to enter payers.

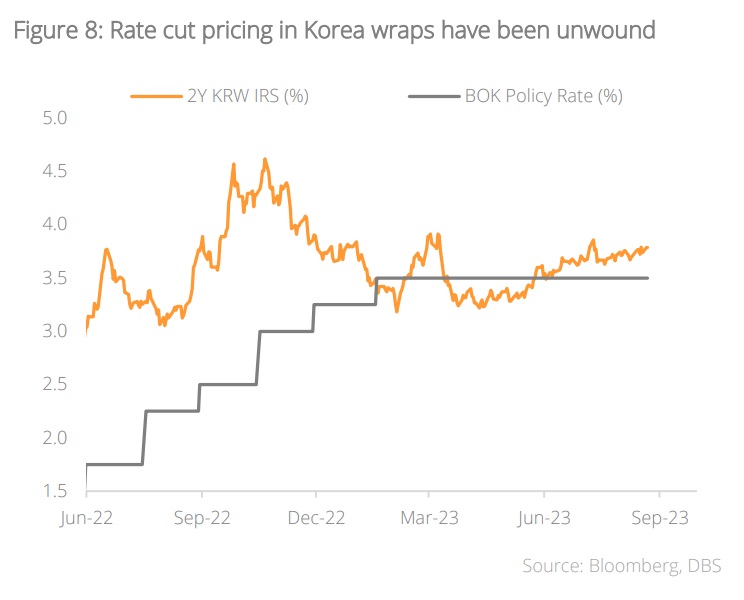

KRW rates: Largely a beta proxy to US rates

Economic outlook seems to be bottoming, recovery in semiconductor sector could be near. We expect the BOK to have hit peak rates, but they remain likely to push back against rate cut expectations amid still-elevated core inflation. Compared to regional central banks, the BOK’s reaction function is relatively more sensitive to Fed policy, due to their focus on Korea-US rate differentials and the potential impact on the KRW FX. With US data still holding up and markets keen to price for more US term premia, pay KRW swaps could be a good beta proxy for rising US rates. That said, passthrough from higher US rates to KRW swaps could be reduced by bullish sentiments towards Korean equities and the associated equity inflows supporting KRW FX. On technicals, much lower net supply of Korea Treasury Bonds in 2023 is a positive.

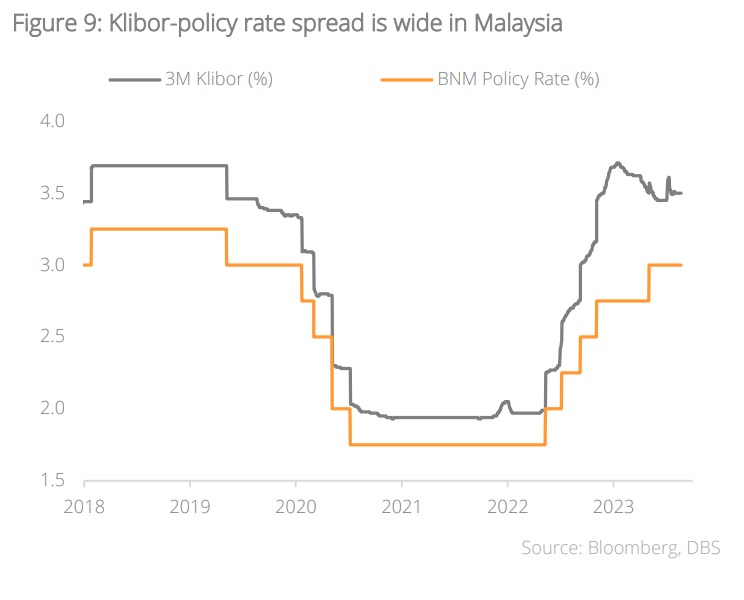

MYR rates: Change in stance

Change in BNM’s stance. Inflation risks are no longer seen as tilted to the upside and the risks of financial imbalances are now perceived to be limited. This change in stance affirms our view that the policy rate would be kept unchanged for the rest of 2023. In addition, the timing of changes to more targeted subsidies and removal of some price controls have been pushed out to 2024, which removes some near-term risks to inflation. KLIBOR-policy rate spread has been widening recently, due to BNM tightening liquidity via increasing sizes of OMOs and Bill issuances. Front-end bond yields and MYR IRS rates look fairly priced for an on-hold BNM at 3.0%. The recent announcement to allow Employee Provident Fund (EPF) members to take out bank loans against their retirement savings could drive expectations of lower EPF demand for long-duration government bonds and result in a steeper curve.

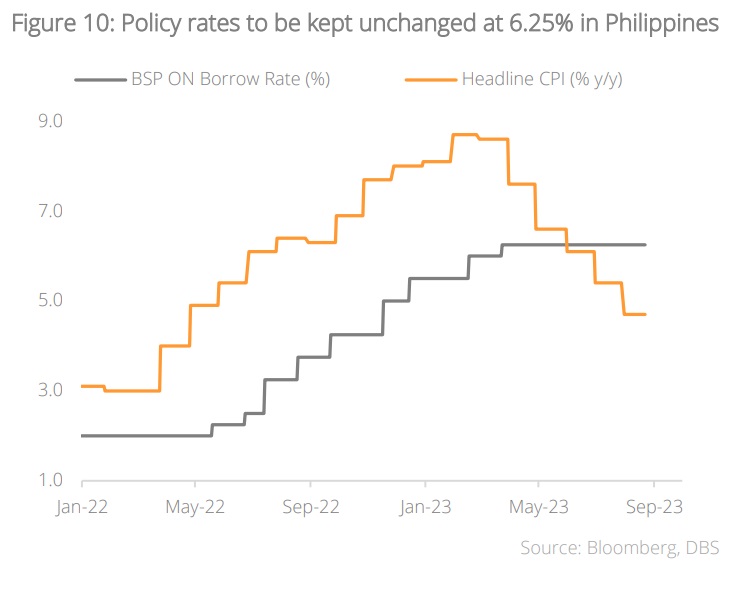

PHP rates: Lower correlations to US rates

BSP expected to stay on hawkish pause, keeping policy rates unchanged, at 6.25% for the rest of 2023. Headline inflation is expected to return to the target by 4Q, but BSP remains concerned about pipeline risks, including the recent climb in global energy and food, as well as domestic catalysts like transport costs, minimum wage increases, utilities, besides a weaker PHP. Despite the low prospects for policy rate cuts, government bonds could outperform regional bonds, due to traditionally low correlations to higher US rates. YTD, fiscal performance has also been strong, and the pace of net issuances is likely to slow in 4Q. Banking liquidity remains elevated and would be supportive of bond demand from banks.

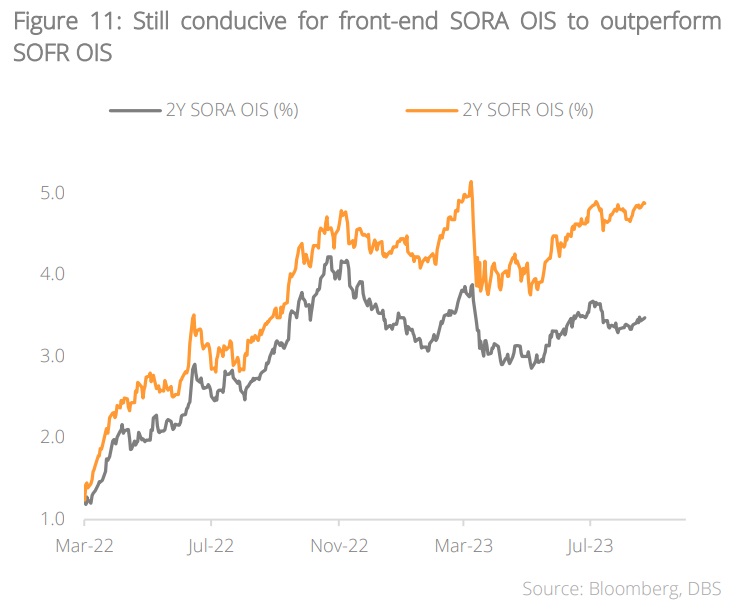

SGD Rates: Front-end outperformance to continue

Tightening cycle likely over, MAS expected to keep policy settings unchanged in October. Considering a still hawkish Fed coupled with expectations of stable O/N SORA and the steep slope of SGDNEER policy, we believe that all-round factors are still conducive for front-end (up to 2Y) SORA OIS and Singapore Government Securities (SGS) bonds to outperform US equivalents. Further out the curve, divergence in bond supply trends would help to anchor SGS yields against rising US Treasury yields. While there are market worries over increasing US Treasury coupon supply, there are no such worries for SGS. At some point in 1H24, when we get closer to both the Fed and MAS’s easing cycles, SGD rates should start to underperform USD rates.

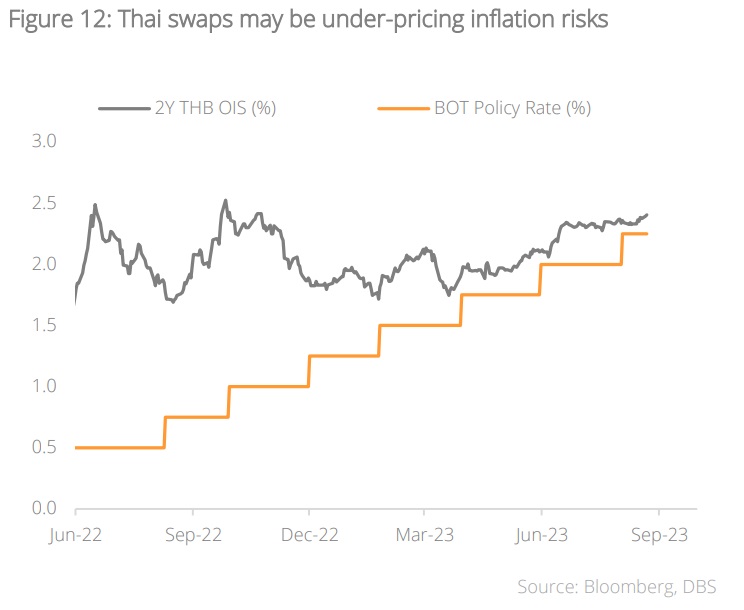

THB rates: BOT in wait-and-see mode

Easing inflation prints helped by favourable base effects and broad decline in commodity-related prices. At the August meeting, the BOT hiked 25 bps to 2.25%, in what we expect to be the last hike of this cycle. Policy statement suggests that the BOT has turned less hawkish on upside inflation risks and could adopt a wait-and-see approach, amid domestic political uncertainty and the associated downside risks to growth. Inflation risks could grow in 4Q when the tourism sector would recover more fully and some of the populist election promises (e.g., cash handouts, wage increases) could be implemented, leading to higher incomes and consumption. Market pricing is for the policy rate to peak at 2.25 or 2.50%, which we think could be slightly under-pricing the inflation risks ahead.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.