- G3: While the Fed kept rates unchanged at the first Warsh-led meeting, the dot plot was hawkish and consistent with the sizable increase in inflation projections; we expect another 25 bps BOJ hike by end-2026 and mid-2027, with Middle East de-escalation and continued AI investment cycle strength supporting further policy normalisation

- China: Industrial activity strengthened on resilient external trade; domestic consumption and investment remained weak; the RMB2tn AI infrastructure plan should act as a catalyst for future FAI growth

- South Korea: We add another 25 bps hike in 4Q26 to our forecast, with inflation expected to remain elevated for an extended period despite lower oil prices

- ASEAN-6: Moderation in currency depreciation and reduced inflation concerns following the Middle East interim deal should ease central banks’ aggressive monetary policy moves

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- European currencies and IDR hold ground amid JPY’s historic slide 30 Jun 2026

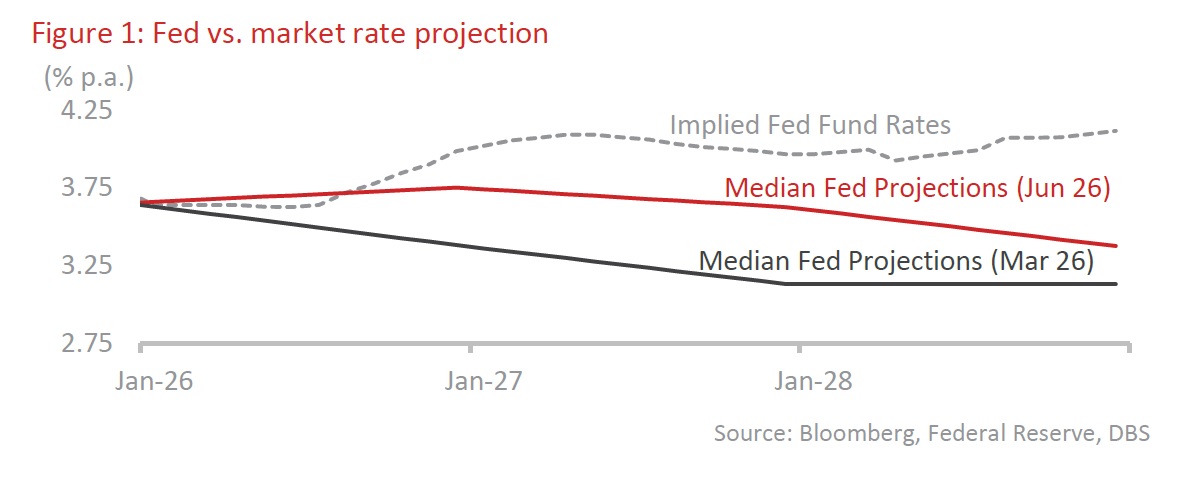

G3: Fed’s hawkish jolt; BOJ to continue policy normalisation. While the Fed kept rates unchanged, as expected at the first Warsh-led meeting, the dot plot was hawkish (nine members saw the need for one or more hikes, pushing the median projection to 3.8 for this year). This is consistent with the sizable increase in core PCE inflation projection to 3.3% (2.7% previously) and 2.5% (2.2% previously) for 2026 and 2027, respectively. Below, we lay out some observations: First, forward guidance is greatly diminished. Signs of this are already apparent from the much shorter FOMC statement and Warsh’s refusal to submit a projection in the dot plot. Second, sweeping changes to how the Fed operates could be announced by the end of the year. Several task forces have been formed to examine communications, the balance sheet, data collection, AI/jobs/productivity, and the inflation framework. These broadly echo some of his comments, including a preference for less communication, a smaller Fed balance sheet, and perhaps a tweak in the preferred measure of inflation (from the current core PCE to some form of trimmed mean inflation). Following the meeting, the futures market is bringing forward its expectations for the next potential Fed hike to Sep 2026.

Meanwhile, the Bank of Japan (BOJ) raised the overnight call rate by 25 bps to 1.00% at its June policy meeting, as expected. Deputy Governor Uchida, who chaired the post-meeting press conference in Governor Ueda’s absence, adopted a cautious tone and avoided delivering any policy surprises. The meeting offered limited guidance on the future policy path, including the pace of further rate hikes and the eventual terminal rate. From a fundamental perspective, the recent easing of Middle East tensions, together with continued strength in the AI investment cycle, has reduced stagflation risks for Japan’s economy and reinforced the reflation narrative. This strengthens the case for further policy normalisation over the coming quarters. The swap market is currently pricing in a c.70% probability of 25 bps rate hikes every six months, implying a policy rate of 1.25% by Dec 2026 and 1.50% by Jun 2027. This trajectory is consistent with the midpoint of the BOJ’s estimated neutral rate range of 1.0-2.5%. We now also expect the policy rate to rise to 1.25% by end-2026 and to 1.50% by mid-2027.

The European Central Bank (ECB) raised the deposit facility rate by 25 bps to 2.25%, marking its first hike in nearly three years. President Lagarde noted the build-up of inflationary pressures and warned of the risk that they could become more broad-based. Baseline ECB projections for GDP growth were tempered, while inflation was revised up. Growth in 2026 is projected at 0.8% y/y before improving to 1.2% in 2027. Headline inflation is set to peak at 3% this year before cooling to 2.3% in 2027. Core inflation is expected to stay above target in 2026 and 2027 at 2.5% before easing to 2.2% in 2028. While officials did not commit to a future course of action, the ‘insurance’ hike was intended to stay on top of price developments, rather than fall behind the curve, in the event the Middle East conflict spills over into 2H26. We maintain our call for another 25 bps hike in 3Q26, with uncertainty surrounding the trajectory of the Middle East conflict likely to keep the policy decision finely balanced between a pause and a modest rate hike.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- European currencies and IDR hold ground amid JPY’s historic slide 30 Jun 2026

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- European currencies and IDR hold ground amid JPY’s historic slide 30 Jun 2026