Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- FX Quarterly 2Q 26: Less De-Dollarisation, More Polarisation30 Jun 2026

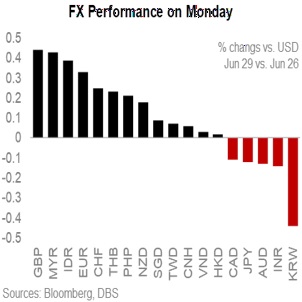

European currencies capitalized on a softening greenback overnight. Tensions in the Middle East stabilized following a temporary pause in hostilities between the U.S. and Iran over the weekend, alongside reports of an Israel-Lebanon peace deal. Easing geopolitical tensions enabled GBP/USD and EUR/USD to recover above their key 1.32 and 1.14 levels, while USD/CHF returned below 0.80. The main highlight was Andy Burnham, the frontrunner to succeed Keir Starmer as British Prime Minister, using his first major policy to prioritize fiscal responsibility in his 10-year economic and devolution strategy under the banner of “Manchesterism.”

In Southeast Asia, the IDR was bolstered by the Indonesian government’s liquidity support for the banking sector. In addition to extending the placement of IDR 281 trillion in state cash funds within state-owned banks through the end of December 2026, an additional IDR 100 trillion in standby funds will be set aside at Bank Indonesia. The finance ministry reported that the state budget deficit reached 0.7% of GDP in May, on track to remain below the statutory 3% ceiling by year-end amid low oil prices. Sentiment improved last Friday, when the finance ministry scaled back President Prabowo Subianto's flagship Free Nutritious Meals program, which will be reviewed every two months for implementation and budget absorption following intense scrutiny over a corruption investigation.

In Northeast Asia, the JPY’s weakest level in 40 years is attracting attention despite the KRW’s steeper losses. The JPY has brushed aside the return of oil prices to around pre-war levels. Markets appear to be hedging the USD’s post-PCE depreciation against other currencies, with JPY. If so, the Ministry of Finance needs to remind markets of the high risk of direct currency intervention supported by the US Treasury. Bank of Japan officials have openly discussed the estimated 2% neutral rate as a goal of the current hiking cycle. The JPY could get some relief if Fed Chair Kevin Warsh, amid lower energy prices, dilutes the latest hawkish FOMC dots to make his case against forward guidance at the European Central Bank Forum in Sintra tomorrow.

Quote of the Day

“Truth never damages a cause that is just.”

Mahatma Gandhi

June 30 in history

Mahatma Gandi’s first arrest in 1914 for campaigning for Indian rights in South Africa.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- FX Quarterly 2Q 26: Less De-Dollarisation, More Polarisation30 Jun 2026

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- FX Quarterly 2Q 26: Less De-Dollarisation, More Polarisation30 Jun 2026