- Valuations remain attractive, with S-REITs trading at below 0.9x P/B and c.6.2% forward yields, a compelling spread of more than 400 bps over the 10Y SGS, with interest rate risks largely priced in

- Earnings growth is returning, supported by refinancing savings and improving DPU prospects across the sector despite concerns of potential rate hikes returning

- We continue to rank our sector preferences as Office > Industrial > Retail > Hospitality

- Property fundamentals remain resilient, underpinned by healthy occupancy, positive rental reversions, and limited new supply across most asset classes

- Capital recycling continues to create value, with REIT managers actively pursuing accretive acquisitions and divestments to enhance portfolio quality and earnings growth

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- European currencies and IDR hold ground amid JPY’s historic slide 30 Jun 2026

Ongoing rotation into growth and cyclical sectors. S-REITs declined 1.6% m/m in May, underperforming STI’s 2.5% m/m gain. The divergence reflects a continued improvement in investor risk appetite, with capital rotating towards cyclical and growth-oriented sectors at the expense of more defensive yield plays such as REITs.

Valuations remain attractive despite higher-for-longer rate concerns. In our view, much of the interest rate risk is already reflected in current valuations. The sector trades at below 0.9x P/B, close to 1SD below its long-term average, while forward yields of c.6.2% offer an attractive c.4.0% spread over the 10Y Singapore government bond yield. Importantly, prevailing SORA benchmarks remain below the sector's average borrowing cost of above 3.0%, providing continued scope for financing cost savings as legacy debt is refinanced.

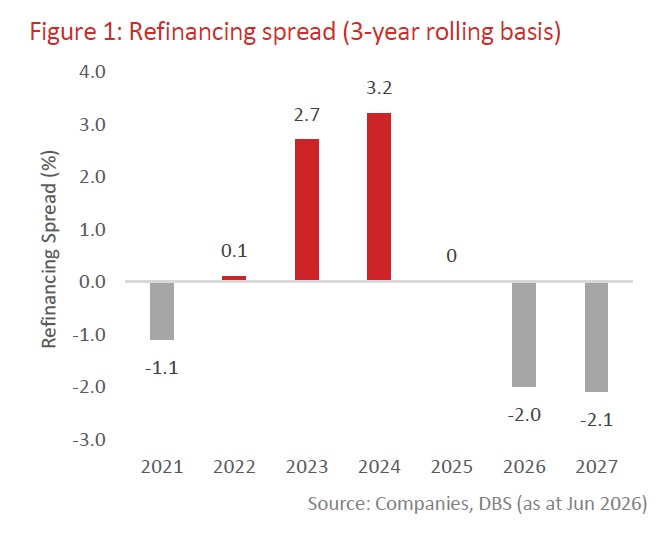

While market expectations have shifted from rate cuts to the possibility of a rate hike by end-2026 amid elevated oil prices and firmer inflation expectations, we believe S-REITs are entering this phase from a much stronger position than in 2022. Unlike the previous tightening cycle, refinancing rates today remain below expiring borrowing costs, allowing contracted borrowing costs to continue trending lower. Based on the sector's refinancing profile, loans maturing in 2026-2027 carry borrowing costs that are more than 200 bps above current refinancing rates, providing a meaningful earnings tailwind over the next two years.

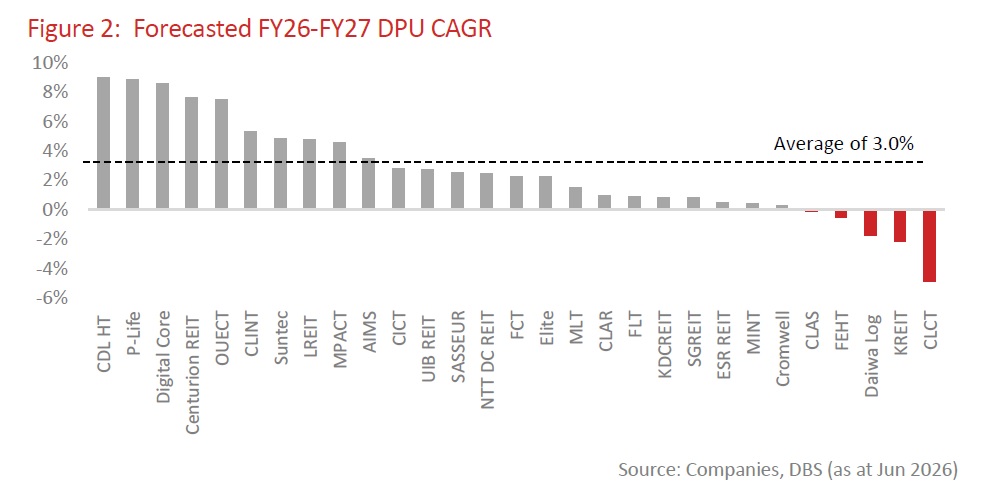

Return to positive earnings momentum is a potential re-rating catalyst. We maintain our forecast for sector-wide DPU growth of 3.0% - 3.4% p.a., marking the first sustained period of distribution growth in three years. We believe this return to earnings growth should support a stabilisation in share prices and potentially drive a broader recovery in valuations. We continue to rank our sector preferences as Office > Industrial > Retail > Hospitality. We remain most constructive on office sector given a multi-year supply drought and improving landlord pricing power. Industrial REITs, particularly those with exposure to logistics and data centres, continue to benefit from structural demand drivers such as digitalisation, cloud adoption, and AI.

Latest 1Q26 results reaffirm sector resilience; capital recycling remains a key earnings driver. Operating fundamentals remain healthy, supported by positive rental reversions, resilient leasing demand and favourable supply-demand dynamics. More than 90% of S-REITs are expected to deliver positive DPU growth over the next two years, reinforcing our constructive outlook on the sector. Meanwhile, strategic capital recycling continues to gain momentum as REIT managers focus on enhancing portfolio quality, strengthening balance sheets, and driving earnings growth. We expect disciplined capital recycling and accretive acquisitions to remain important differentiators for the sector.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- European currencies and IDR hold ground amid JPY’s historic slide 30 Jun 2026

Related insights

- Research Library30 Jun 2026

- USD Rates: Labour market watch 30 Jun 2026

- European currencies and IDR hold ground amid JPY’s historic slide 30 Jun 2026