- Heightened market volatility should continue to underpin trading and markets income globally

- US banks reported strong 1Q26 results, driven by NII growth and robust non-NII

- For Asia, structural growth in wealth management, alongside resilient investment banking activity, is expected to sustain solid non-NII expansion

- Capital positions of large banks globally remain strong, supporting continued capital returns through dividends and share buybacks

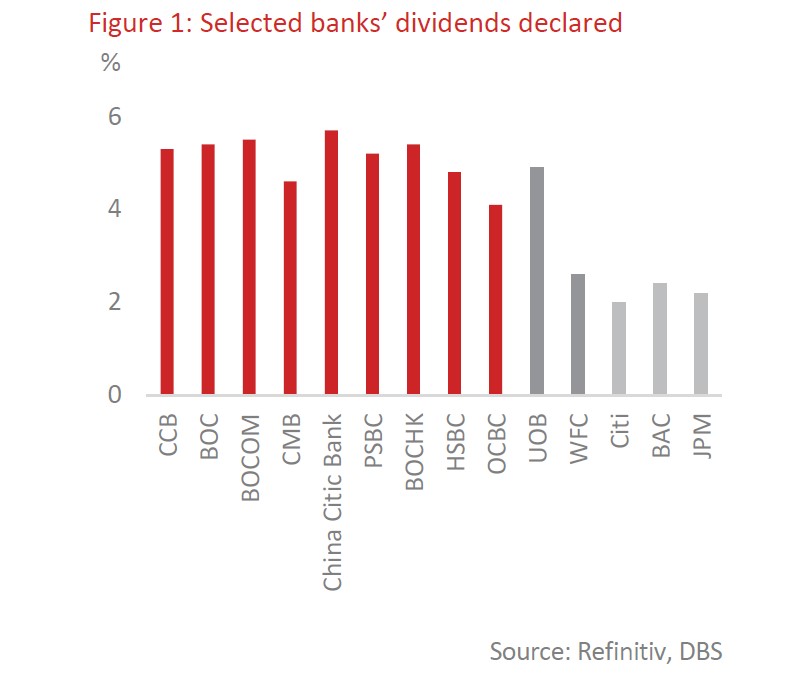

- We remain highly selective in banking stocks; dividend yields across Asia banks continue to be in the spotlight amid a lower yielding environment, offering attractive dividend yields between 4–6%

Related insights

- Taiwan: Mild tightening in 2H11 May 2026

- USD Rates: Labour Market Firms Up11 May 2026

- Alphabet Inc11 May 2026

Resilience amid macroeconomic volatility; asset quality risks remain contained. Ongoing Middle East tensions are likely to keep policymakers cautious on inflation, delaying rate cut expectations. While the base case remains for modestly lower benchmark rates into FY26F, we continue to expect only a marginal decline in net interest income (NII), supported by active balance sheet management and deposits growth. Overall, earnings should still see slight decline with strong growth in non-interest income (non-NII) buffering weaker NII. While US macro uncertainties are building, the economy has remained relatively resilient. For SG/HK/CH banks, exposure to US, China, and Hong Kong CRE remains a key watchpoint, though overall risks appear manageable for now. Provisioning levels remain prudent with buffers built up over the Covid-19 pandemic providing downside protection. We also expect a gradual stabilisation in Hong Kong CRE, led by early signs of recovery in the residential segment.

US banks reported strong 1Q26 results; non-NII momentum remains solid across Asia. Heightened market volatility should continue to underpin trading and markets income globally. US banks reported strong 1Q26 results, driven by NII growth and robust non-NII, including markets, trading, investment banking revenue amongst others. In Asia, structural growth in wealth management (WM) alongside resilient investment banking activity is expected to sustain solid non-NII expansion. Net new money trends remain healthy, supported by regional inflows and a growing affluent customer base. Fee income diversification should continue to offset any cyclical softness in capital markets activity.

Remain highly selective in banking stocks; shareholder returns remain attractive. We believe US banks are poised for high single-digit y/y earnings growth as investment banking fees and trading income continue to boost non-NII. China banks’ margins have begun to stablilise, which will support slight growth for earnings. Singapore banks may continue to see NII pressures on lower benchmark rates which will weigh slightly on overall earnings while Hong Kong banks are at a more resilient position on a y/y basis as HIBOR is back to a normalised level vs its extreme low level in 2Q25-3Q25. Dividend yields across Singapore, Hong Kong, and China banks continue to be in the spotlight amid a lower yielding environment, offering attractive dividend yields between 4–6%. Capital positions of large banks globally remain strong, supporting continued capital returns through dividends and share buybacks. Managements have reiterated commitment to sustainable payout ratios while retaining flexibility for growth. This should continue to underpin investor interest in the sector.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Taiwan: Mild tightening in 2H11 May 2026

- USD Rates: Labour Market Firms Up11 May 2026

- Alphabet Inc11 May 2026

Related insights

- Taiwan: Mild tightening in 2H11 May 2026

- USD Rates: Labour Market Firms Up11 May 2026

- Alphabet Inc11 May 2026