Related insights

- Cognizant Technology Solutions11 May 2026

- Expedia Group11 May 2026

- USD Rates: Labour Market Firms Up11 May 2026

Following our earlier upward revision of 2026 GDP and CPI forecasts (to 9.4% and 1.9%, respectively), we also revise our interest rate forecast, adding one 12.5bps rate hike in 3Q, which would lift the policy discount rate from 2.00% to 2.125%.

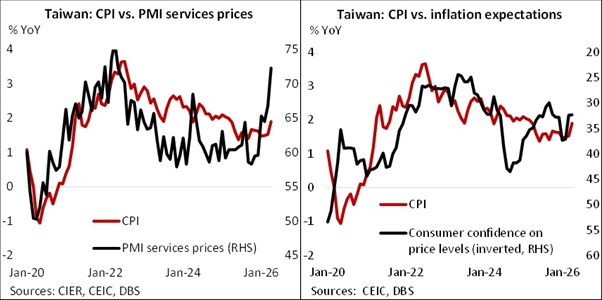

Recent data suggest that the central bank is likely to remain on hold at the June policy meeting. Headline CPI rose from 1.2% yoy in March to 1.7% in April. On a sequential basis, CPI also recorded a notable 0.5% mom increase (sa). The pickup was driven mainly by a 2.1% yoy increase in transportation and communication costs, reflecting partial increases in retail fuel prices amid the surge in global oil prices following the Middle East conflict, despite subsidies provided by state-owned CPC. Core CPI remained relatively stable at 1.9%, suggesting that pass-through into broader goods and services prices has so far remained limited.

Looking ahead, however, tightening pressure is likely to build in 2H as pipeline inflation pressures continue to rise. PPI surged to 8.5% yoy in April, approaching the 14.2% peak seen during the 2022 Russia-Ukraine war. PMI price subindices also rose sharply, with the manufacturing PMI raw material prices index jumping to 87.3 and the services PMI prices paid index rising to 72.3, both close to their respective 2022 peaks of 87.5 and 76.1. These leading indicators suggest that headline CPI could rise above 2% from May onward and reach around 2.5% by mid-year. Some pass-through into core inflation is also likely, potentially pushing core CPI toward 2.5% in 2H.

Taiwan’s central bank remains vigilant against second-round inflation effects stemming from higher energy costs. As reflected in the March MPC meeting minutes, several members highlighted the need to closely monitor public inflation expectations, which could warrant a monetary policy response. Although inflation expectations, as measured by the consumer confidence survey, had not deteriorated sharply as of April, such indicators tend to move coincidently with CPI rather than act as leading indicators. If CPI rises more noticeably from May onward, inflation expectations could also begin to increase. In addition, CPI for frequently purchased items (purchased at least monthly or quarterly) rose more visibly in April, suggesting that consumers are becoming increasingly sensitive to rising prices, which may further reinforce inflation expectations in the coming months.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

Explore more

E & S FlashGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related insights

- Cognizant Technology Solutions11 May 2026

- Expedia Group11 May 2026

- USD Rates: Labour Market Firms Up11 May 2026

Related insights

- Cognizant Technology Solutions11 May 2026

- Expedia Group11 May 2026

- USD Rates: Labour Market Firms Up11 May 2026