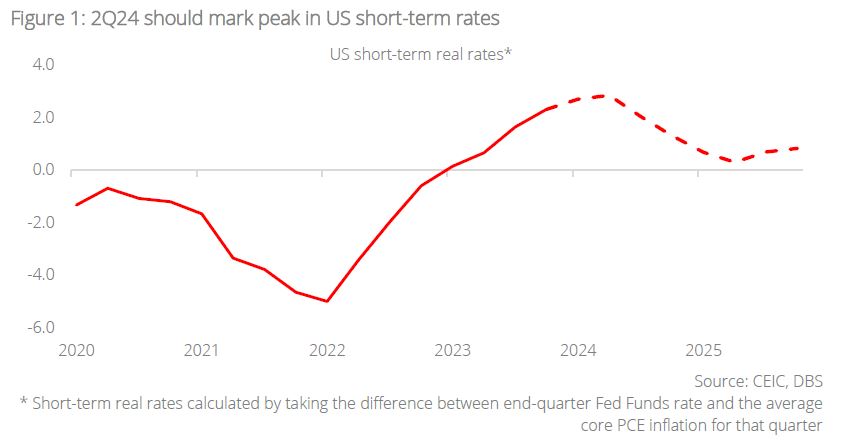

- US: Fed reaffirms focus on cautious rate cut trajectory; we believe 2Q24 will mark the peak in US short-term real rates though room for rate cuts will be limited by sticky inflation

- Singapore: Steady MAS policy in upcoming April review; lower inflation forecast ahead with external-led demand to drive growth recovery

- Thailand: Worst is likely over following the late-March approval of the delayed FY2024 budget; tourism and private consumption to remain key growth drivers

- Vietnam: On track for gradual growth recovery driven by uptick in export-oriented activity; strong FDI inflows continue to surpass pre-pandemic highs

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

US: Fed sticks to cautious rate cut strategy. In line with expectations, Fed Chair Jerome Powell affirmed this week that the Fed would reduce the restriction in monetary policy weighing on aggregate demand once it was confident that inflation was on a sustainable path to the 2% target. He noted that accelerated immigration and increased prime-age participation brought a better balance between labour supply and demand.

Prices paid fell a second month to 53.4 from 58.6, its lowest level since March 2020, suggesting negative surprises for next week’s US Consumer Price Index inflation. Services employment increased from 48 in February to 48.5 in March, less than the 49 consensus and below the breakeven 50 level for a second month. Today (5 Apr), markets are bracing for nonfarm payrolls to fall to 213k in March from 275k in February.

According to a US Treasury press release, US Treasury Secretary Janet Yellen will visit China on a diplomatic trip to manage their bilateral economic relationship, and advance American interests. Yellen will likely follow up on China’s “unfair trade practices and non-economic practices,” an issue US President Joe Biden raised during his call with China President Xi Jinping earlier this week and seek more insights on China’s economy.

Peak in US short-term rates. We believe 2Q24 will mark the peak in US short-term real interest rates, defined as the difference between Fed Funds rates and core PCE inflation. Fed policy rate cuts are on the cards from mid-year onward even if core inflation does not ease much more. However, we do not expect negative real rates in this cycle as room for rate cuts through 2024/25 may well be limited by some stickiness in inflation and resilient demand.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024