- Equities: Most major global stock markets continue to post record highs boosted by the Fed’s dovish tilt and a stronger than expected economy. However, China and Hong Kong markets were lacklustre due to weakness in China’s property market.

- Credit: Diminishing demand and higher supply of US debt could lead to rising term premium and steeper yield curves, reaffirming our strategy to stay short-duration, preferring 3-5Y duration bucket

- FX: USD/JPY rose despite the end of BOJ’s negative interest rate policy and YCC framework; however, USD/JPY backed off whenever it neared 152

- Rates: Resurgence of sticky inflation pushed bond yields higher; 2Y yields hit above 4.70% and set a new high for the year

- The Week Ahead: Despite divergences amongst central banks, the broad picture of G10 easing (with exception of Japan) remains broadly intact

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

Global equity markets powered higher. The Dow Jones, the S&P 500 and the NASDAQ rose 2.0%, 2.3% and 2.9% respectively for the week, making new highs. A dovish Fed and better- than- expected economic data fueled gains for the US markets. Powell’s dovish tilt and comments that there are no cracks in US’ strong jobs growth boosted market sentiment. US markets registered their best week in 2024. European stock markets benefited from the Fed’s dovish tilt and the eurozone composite PMI rising to 49.9 from 49.2 in February. The STOXX 600 rose 1.0% for the week, near its record high. The Bank of Japan (BOJ) ended Japan’s negative interest rates policy (NIRP), removing an overhang on the markets. Nikkei 225 rallied 5.6% this week. In stark contrast, China and Hong Kong markets declined as China’s property sector sales continue to be weak, dropping 20% in January and March. The Shanghai Composite Index edged down 0.2% while the HSCEI and HSI dropped 1.1% and 1.3% respectively for the week.

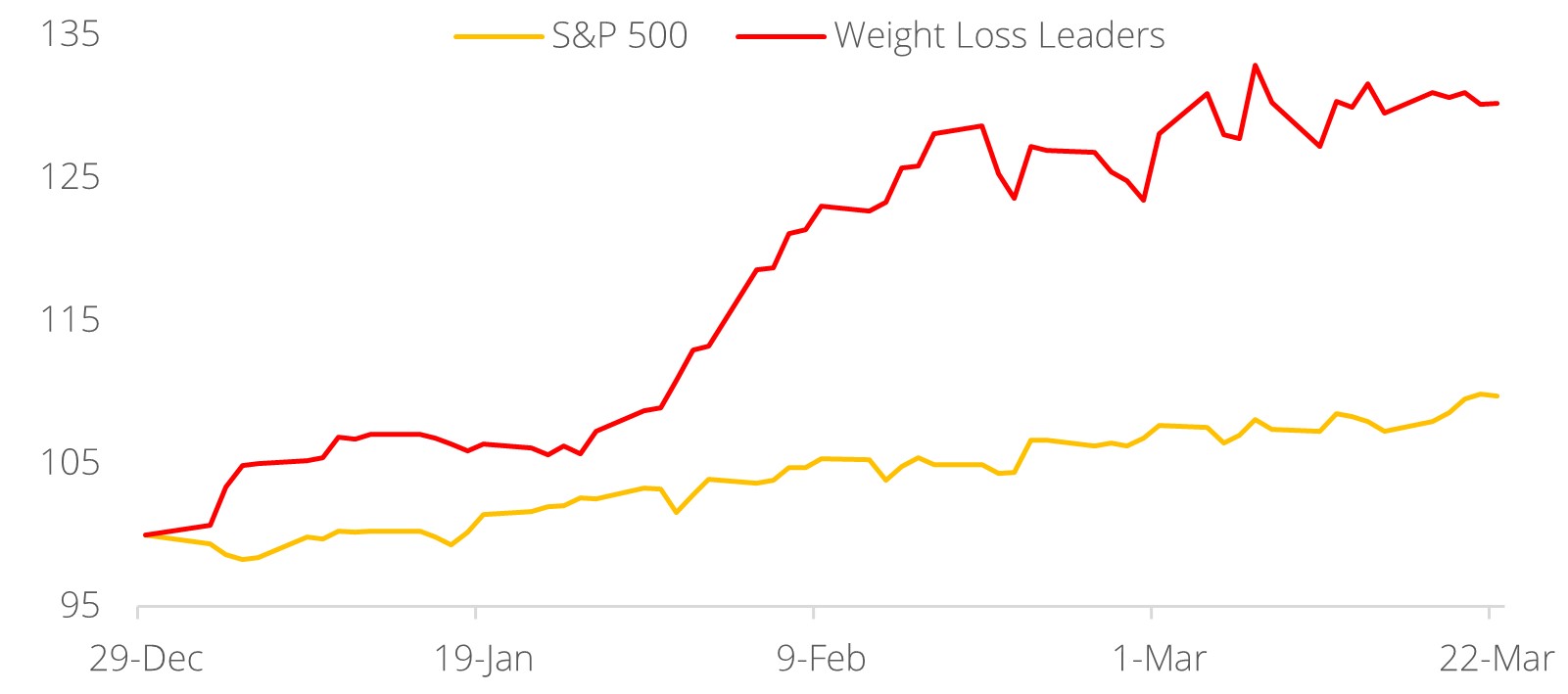

Topic in Focus: Healthcare – Pharma’s latest blockbusters. Since receiving FDA approval for chronic weight management, weight loss drugs such as Tirzepatide and Wegovy from Eli Lilly and Novo Nordisk have been met with record demand. The insatiable demand for these weight loss drugs has propelled Novo Nordisk to beat LVMH, becoming Europe's largest company by market capitalization. YTD the makers of weight loss drugs have outperformed S&P 500 by a staggering c.20%.

This remarkable outperformance is driven by the increasing global obesity epidemic - more than 2.5b adults globally are overweight, creating a surging demand for effective weight loss solutions. Tirzepatide and Wegovy have demonstrated profound efficacy in clinical trials, showcasing not only substantial weight loss but also improvements in cardiovascular health and diabetes markers. The dual benefits have expanded potential market beyond individuals seeking weight loss to include patients managing chronic conditions related to obesity.

Given the strong demand for effective weight loss solutions, combined with positive clinical outcomes and high-profile endorsements, tailwinds for the manufacturers of weight loss drugs to continue outperforming the broader market is well-founded.

Figure 1: Stellar outperformance by weight loss leaders

Source: LSEG, DBS

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024