- US: Fed keeps rate trajectory for 2024 in latest FOMC; high rates reflect strong underlying demand as seen in resilient economic data

- Japan: BOJ ends regime of negative rates and yield curve control; impact on real economy to be limited

- China: Emerging bottom-up recovery signs with pick up in manufacturing growth and strong external orders in the pipeline

- India: Markets will be focused on political stability and continuation of economic reforms as the elections draw near

- Indonesia: BI’s timing of a dovish pivot will hinge on the US rate cycle; Indonesia’s growth to stay supportive

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

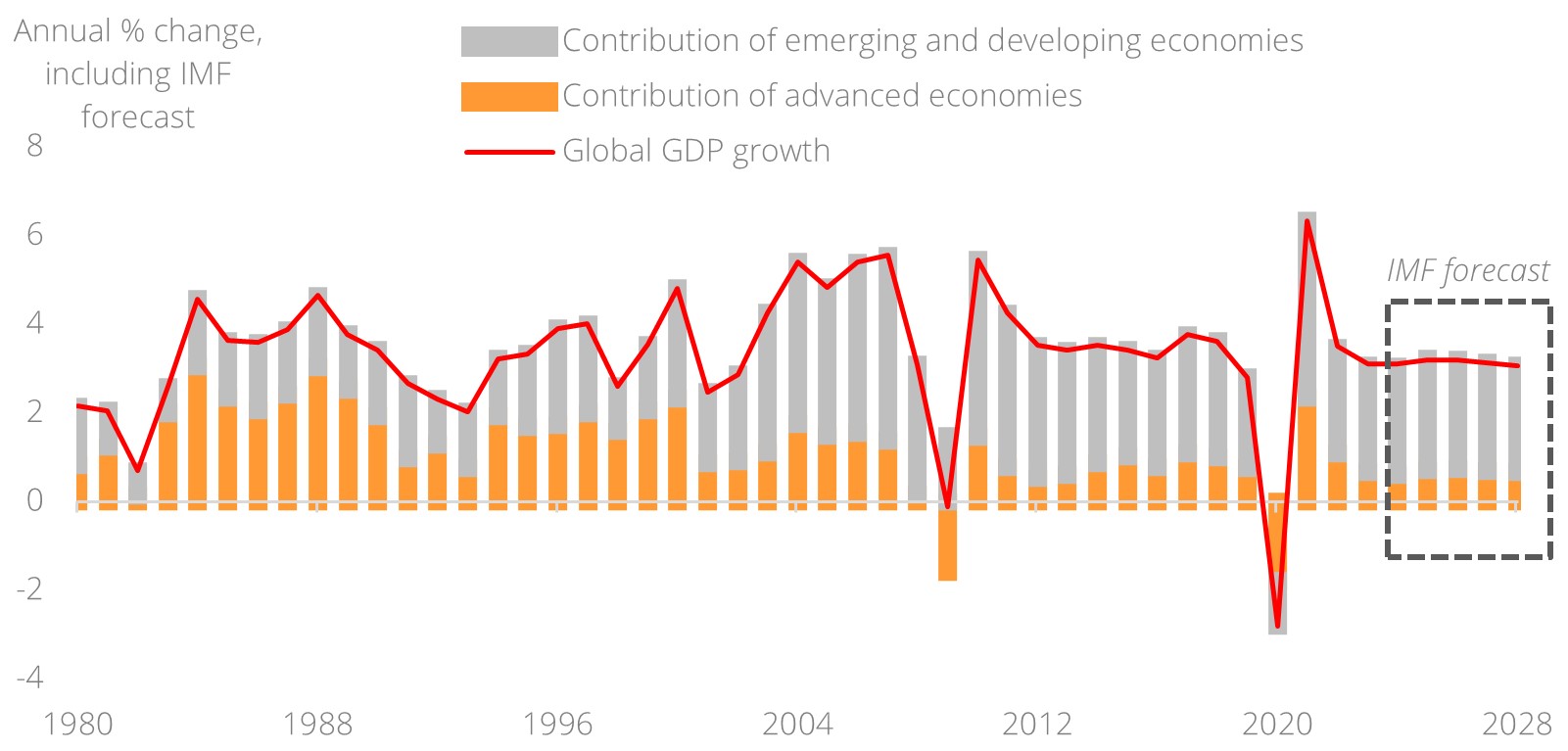

Global: Steepening yield curve a reflection of strong demand. The narrative of 2024 being a year of sizeable interest rate cuts, so prevalent just a few months ago, has been upended rather dramatically. A few months of sticky inflation data and growing evidence of demand resilience have pushed up yield curves around the world. The markets are not giving up on rate cuts, rather expecting them to take place later and to be fewer.

There is little apparent consternation in financial markets owing to these developments. Public and corporate debt issuances and refinancing are progressing without a hitch, stock markets are in rally-or-stable mode, volatility markers are at five-year lows, financial conditions are on the easy side, and currency markets are largely gyration-free.

The key reason for fixed income market repricing causing barely a ripple in wider markets stems from economic data. The inflation surprises so far do not reveal any supply side distortions or demand shocks. Labour markets in the US are tight, keeping services inflation high, but goods and energy prices are well-behaved, reflecting soft demand in China and ample supply/production. Even China and Europe, a laggard on the demand side relative to the US, have stopped from yielding negative dataflow. Exports have bottomed out, tourism and travel continue to thrive, and shocks from various wars and inclement weather have been absorbed remarkably well.

As long as high rates are a reflection of strong underlying demand, which in turn reflects higher rate of return on capital, the fixed income market capitulation should be seen in a constructive light. Typically, a higher-than-expected interest rate horizon would bode ill for debt holders, but if their incomes, wages, and profits are growing at the same time, then a higher debt service cost need not be a net negative. There is a delicate balance in place in this context—climbing rates, if they are countered by healthy outturns in other items in the balance sheet, can be readily absorbable.

Figure 1: Stable economic growth ahead

Source: LSEG Datastream, DBS

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024

Related insights

- Macro Insights Livestream: Thursday May 9th - 4pm SGT 03 May 2024

- Singapore Equity Picks02 May 2024

- Global Sports Apparel: Reposition against Rising Players02 May 2024