- Equities: US Equities reached record highs on expectations of rate cuts, supported by resilient consumer spending and over USD6t sitting on the sidelines

- Credit: Historical widening of credit spreads following a Fed pause underscores need for selectiveness in credit risks. Sweet spot remains with A/BBB Credit in 3-5Y duration segment

- FX: BOJ getting closer to ending its ultra accommodative monetary policy; Potential JPY recovery vs DM currencies amid weak USD bias

- Rates: USD rates undecided on direction after passing through US labour data; 2Y to 10Y yields close to the bottom of recent ranges

- The Week Ahead: Keep a lookout for US Initial Jobless Claims; Japan PPI Number

Related insights

US Equities reached all-time high as Fed signals potential rate cuts. Investor optimism surged as Fed Chair Jerome Powell's testimony before a Senate committee ignited hopes for rate cuts in the June Federal Open Market Committee (FOMC) meeting. Powell's remarks, suggesting the central bank was nearing a point where it could confidently begin reducing interest rates, provided the catalyst to propel US indices to unprecedented levels. The S&P 500 and Nasdaq rallied to record highs on Friday’s (8 Mar) trading session. This remarkable milestone was achieved despite mixed economic data. Despite a higher-than-expected unemployment rate of 3.9% for February, compared with the consensus estimate of 3.7%, the US economy added 275k jobs, surpassing the forecasted 200k figure.

We continue to remain constructive on US Equities as we head into 2024, buoyed by the prospect of the Federal Reserve initiating interest rate cuts as early as June. Complementing this tailwind is the remarkable resilience exhibited by consumer spending, underpinned by a robust labour market and solid wage growth. Moreover, the staggering USD6t parked in money market funds on the sidelines could further propel the rally.

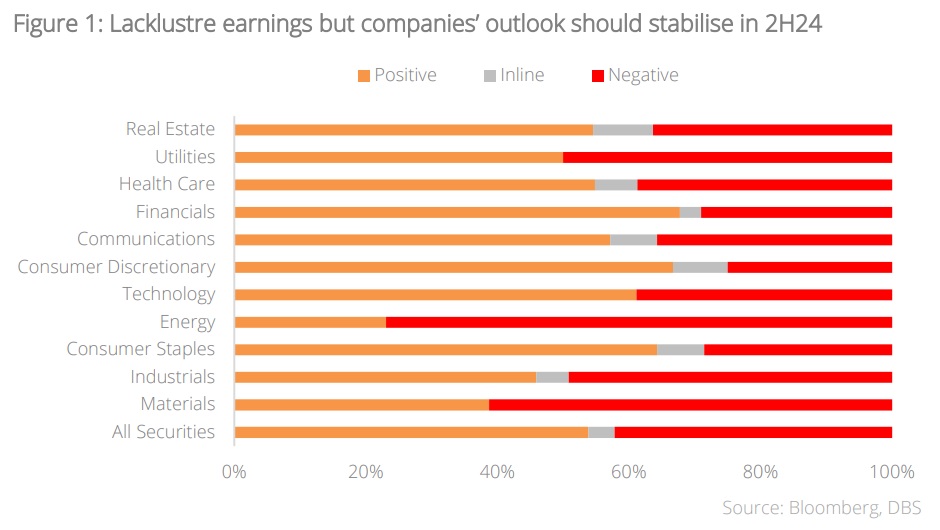

Topic in focus: Europe Equities – Sluggish outlook continue to weigh on earnings. With c.60% of companies having reported earnings, STOXX 600 EPS beats are at a near decade low. Consumer Discretionary, Consumer Staples, Technology, and Financials posted strong earnings beats, while Energy and Materials were among the weakest. Earnings revisions and expectations continue to trend south for Europe Equities, with consensus expecting mid-teens contraction in 1Q24.

On the back of abating inflationary pressures, a more accommodative European Central Bank (ECB), and cyclical recovery in the manufacturing sector, we believe Europe’s economy should show signs of stabilisation in the later half of the year. As we await pivotal factors for upward revaluation, we remain defensive on Europe Equities – we stay overweight on the Tech sector, focusing on upstream semiconductors. In Real Estate, we maintain specific interest in logistics and data centre-related assets. While European banks had a good year in 2023, we expect headwinds from slowing economic growth and declining interest margins. For the luxury sector, we advocate brands which align with the “Quiet Luxury” theme. Healthcare earnings should stay resilient through economic cycles, particularly those specialising in medicines for conditions such as obesity and cancer.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.