Related insights

China reopening hopes to safeguard global economy; inflation a “poison”. As world leaders met and concluded the World Economic Forum in Davos, discussions were centred around recession, China reopening, global debt pile, inflation, and climate issues. While making a call on recession is tricky, sentiments were unanimously more upbeat than in the same meeting last May when the Russia-Ukraine crisis started. China’s reopening hopes and an impending end to the global hike cycle this quarter also cushioned earlier global hard landing fears. Despite the cyclical hopes, frustration was apparent over structural issues, namely deglobalisation, and the lack of real climate actions.

Between a rock and a hard place, central banks raised concerns about inflation risks which they are determined to “stay the course” (on the fight against it), while feeling more hopeful about the global economy. Here are the key takeaways:

- A mild recession

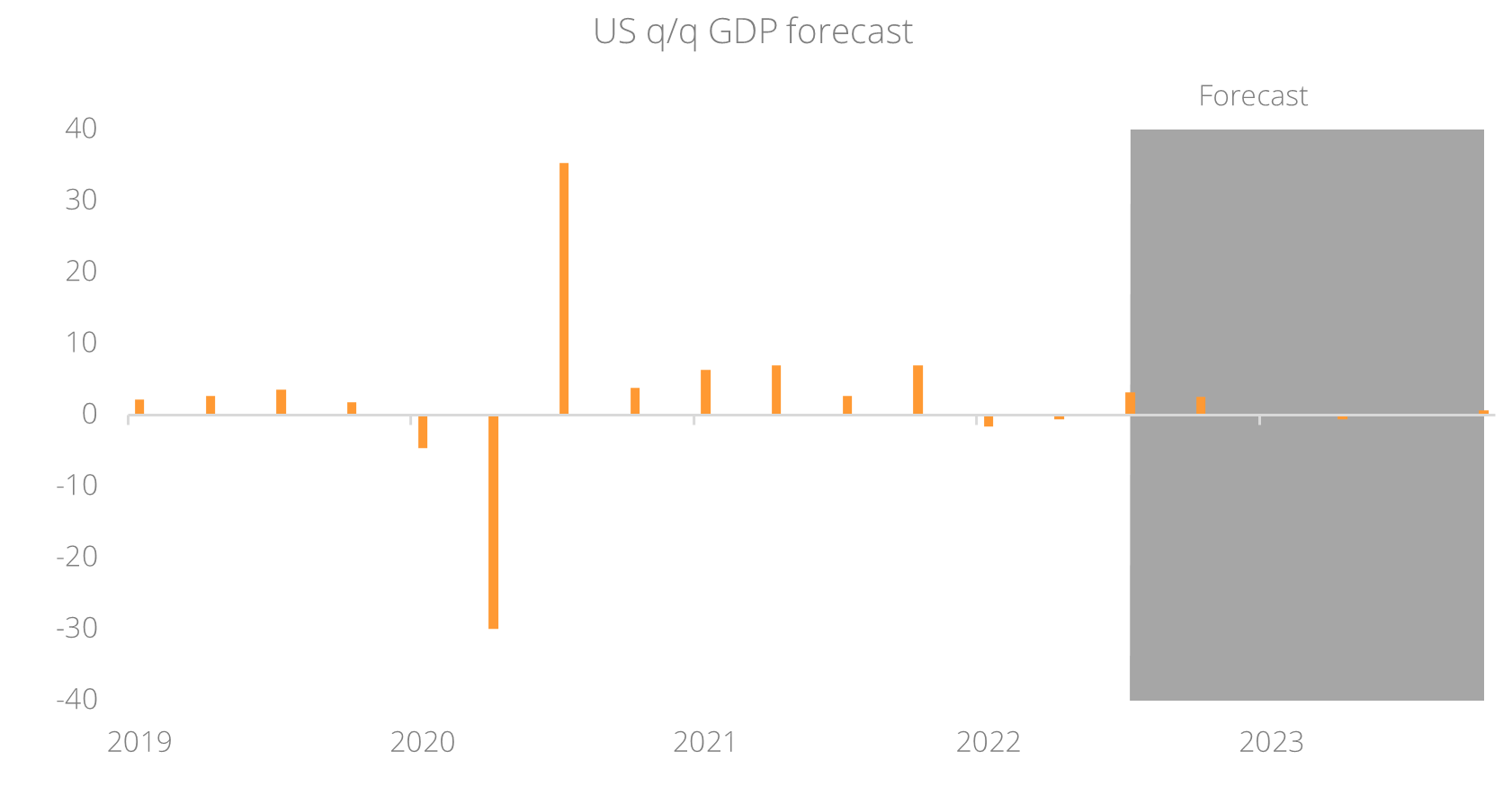

CEOs of major global banks remain optimistic about a “mild” recession which is going to be shorter and shallower than previously thought. Despite ongoing geopolitical and economic uncertainties, the business environment remains resilient – unemployment is low and companies are still investing. China's reopening after a multi-year Covid-related shutdown would help jumpstart the global economy. Gloom about the economy was seen in the rear-view mirror – confirming our view that many negatives have already been priced in.Figure 1: A recession can be avoided

- Central banks to ‘stay the course’

Calling inflation “poison”, the message from central bankers present at the meeting, including International Monetary Fund and European Central Bank chiefs, was that rates are likely to go higher as inflation is way too high by all accounts, and they shall stay the course on fighting inflation.

We continue to look for two more 25 bps Fed hikes by 1Q before pausing. And if it does pause, a soft landing shall thus become more likely. A Fed pivot is unlikely this year as inflation remains a bigger concern than growth risk, in our view. - Oil price

Oil majors are optimistic on oil demand as China’s reopening is seen as a major boost to oil demand as it was down significantly last year during China’s lockdown. Near-term boost to oil prices include US SPR refilling to start in February.

Meanwhile we forecast oil prices at around USD80-100 in 2023. This should support earnings and cashflow for the European oil majors to continue buybacks and pay high dividends.Figure 2: Oil price to stay supported with upside risks

- Warmer China ties

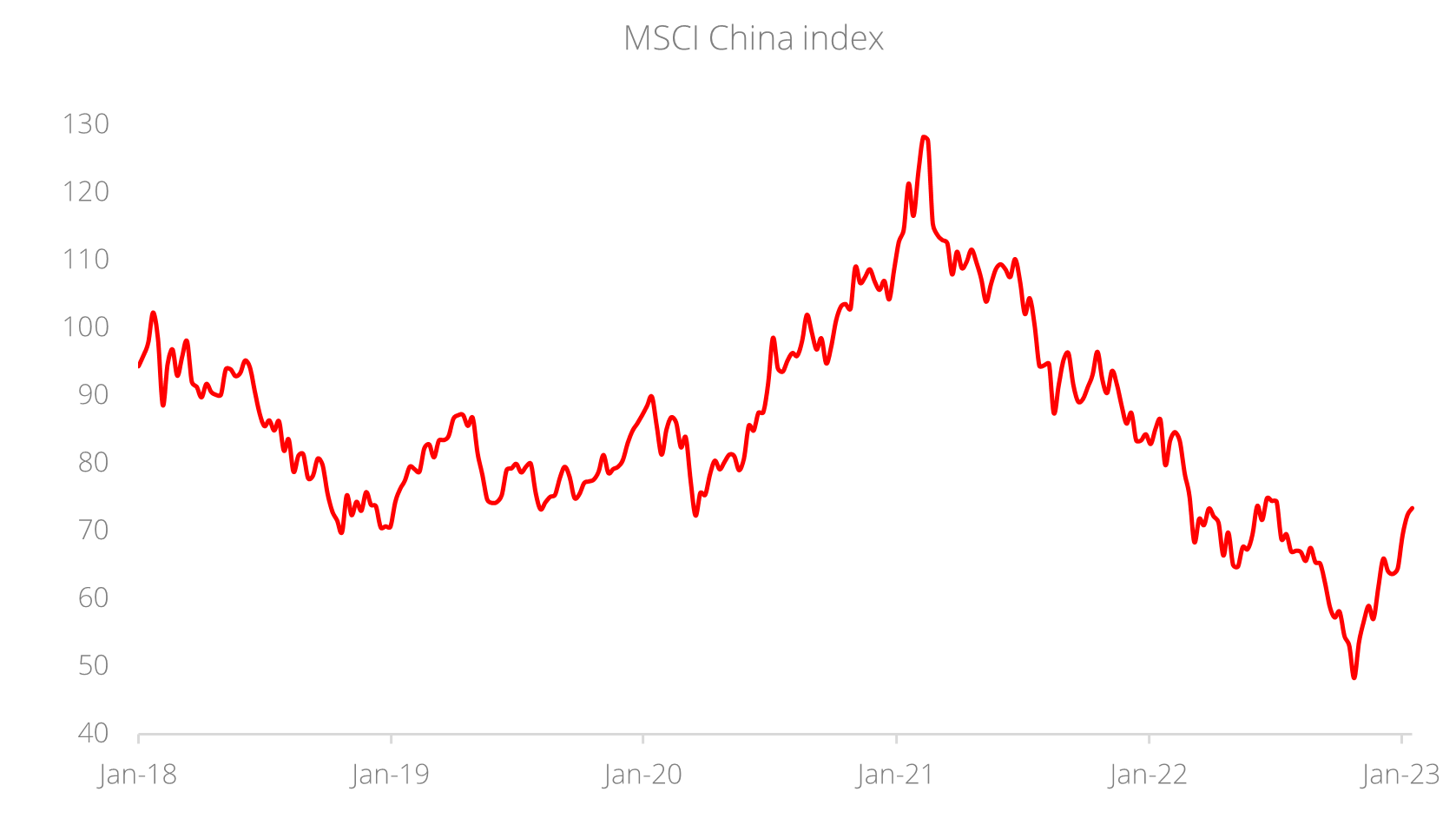

China’s Vice Premier Liu He’s constructive meeting with US Treasury Secretary Janet Yellen in Davos was a step toward improving dialogue, with plans announced for Yellen to visit Beijing later in the year. We see this as a sign of thawing US-China relations – a major catalyst for better China equity performance this year. Meanwhile, France says the European Union should engage China and not oppose it, suggesting that China will be back on the world stage.Figure 3: China equities index trading below pre-US/China trade war levels

- CEOs signal M&A ramp up

CEOs of large banks and corporates signaled that the pace of mergers and acquisitions (M&A) is likely to ramp up despite persistent uncertainty about the outlook for 2023, taking advantage of more sensible valuations to improve on productivity and invest in future growth. Indeed, our analysis concludes that large quality companies have strong earnings and cashflow to take advantage of current market conditions to boost investments and acquisitions for future growth. Valuations of some of these companies also look enticing for private equity and activist funds as a lot of value can be harnessed at these levels.

What it means for your portfolio

The investment environment is likely to be challenging on the back of recession and inflation risks, but windows are open to be engaged in the long term, in a multi-asset portfolio of equities and bonds. We reinforce our view that portfolios should stay invested based on the following:

- Stay engaged in bonds particularly Investment Grade credit with 3-5 years maturity. It would take at least 200 bps of rate hikes by the Fed for this asset class to start registering negative return. Given our view of terminal rate at 5%, this will be a good risk-reward.

- Stay engaged with equities. Growth and Technology equities as part of our barbell strategy make sense as they were the worst hit in 2022 from fear of rate hikes, so the expected slower trajectory this year would act as a tailwind.

- Stay with Gold as a risk-diversifier and hedge against black swan events to add overall resilience.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.