- Indonesia's equity market experienced a significant decline of more than 8% following the index provider’s concerns regarding its transparency and low liquidity

- Failure to implement mitigating actions by May 2026 could lead to a reduction in the weighting of Indonesian equities within EM indices, and potentially a reclassification of the country's market status from EM to FM

- While we view Indonesia’s removal from EMs as unlikely, in the worst-case scenario where it is reclassified into FM, Indonesia will be the biggest market since it is about half the size of all FMs combined. Investors will still have a meaningful allocation to Indonesia

- We maintain our overweight stance on Indonesia and recommend investors pick up strong large cap names at lower valuations

- Their attractiveness lies in strong 2026 earnings growth, driven by domestic factors, relative cheap valuations, demographic dividends, and benefitting from its current sweet spot in commodities

Related insights

- Mondelez International09 Feb 2026

- Japan’s election and possible JPY surprises09 Feb 2026

- Mizuho Financial Group09 Feb 2026

Indonesia's equity market experienced a significant decline of more than 8% following the index provider’s latest free float assessment of local securities. The assessment highlighted concerns regarding the transparency of shareholding structures and other trading practices, prompting the agency to call for improvements. While an interim freeze on certain index-related changes is in effect, the index provider has set a deadline of May 2026 for relevant reforms. Failure to implement mitigating actions could lead to a reduction in the weighting of Indonesian equities within emerging market (EM) indices, and potentially a reclassification of the country's market status from EM to frontier market (FM). Despite Indonesia equities expected to register the strongest 2026 earnings growth in ASEAN, driven by domestic factors and offering healthy dividend yields, the near-term outlook remains pressured by concerns over a potential downgrade in the market status.

We believe the sell-off as a result of the confusion has been stamped out. The index provider’s plan, announced last year, to review the free float classification, may have also hindered major inflows. This has led to relatively low foreign ownership after persistent foreign investor outflows in 2025. Indonesia’s largest bank has announced IDR5tn in share buyback plans, and other large conglomerates have existing share buyback plans, which may be triggered. The Financial Services Authority (OJK) has also responded promptly, announcing a minimum free float requirement of 15% for public companies.

What can happen with the reclassification? There has been precedence in the past that countries have been downgraded from EM to FM status by major index providers. These downgrades usually occur when a country's stock market fails to meet the required criteria for size, liquidity, or accessibility for foreign investors.

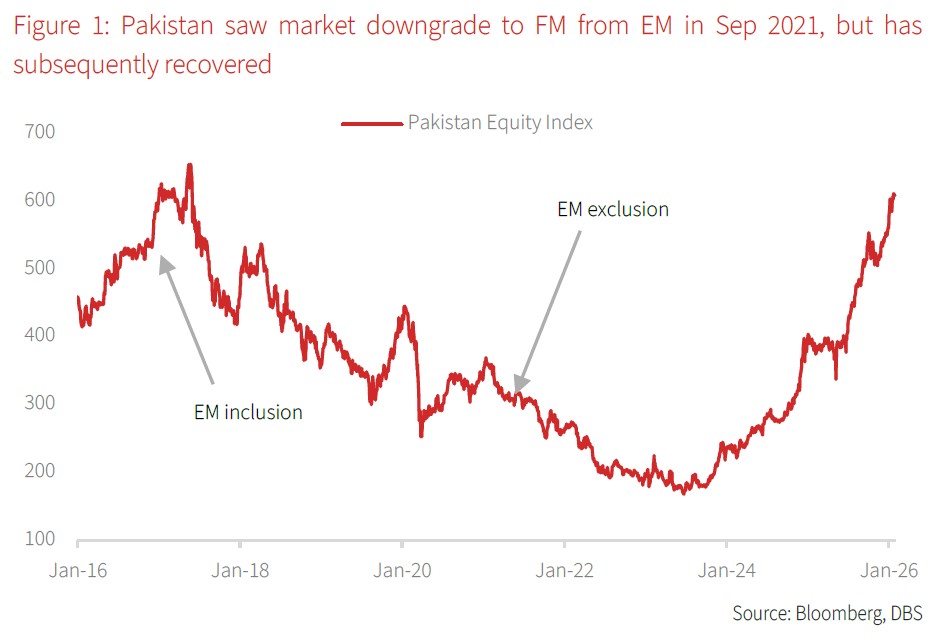

As an illustration, the most recent example of an EM to FM downgrade was with Pakistan in Sep 2021. The decision was driven by the Pakistan equity market no longer meeting the minimum size and liquidity standards for EMs, following a previous promotion to EM status in 2017. Pakistan’s equity market experienced a significant decline by 13% over a month. However, the equity market has seen a remarkable recovery, more than tripling in value since 2023. This robust performance is largely attributable to the nation's successful economic turnaround from its 2023 crisis. Key factors underpinning this recovery include the securing of IMF programs, the implementation of stringent fiscal and monetary policies to combat high inflation, and the subsequent stabilisation of its currency.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Mondelez International09 Feb 2026

- Japan’s election and possible JPY surprises09 Feb 2026

- Mizuho Financial Group09 Feb 2026

Related insights

- Mondelez International09 Feb 2026

- Japan’s election and possible JPY surprises09 Feb 2026

- Mizuho Financial Group09 Feb 2026