- The Liquid+ strategy has continued to perform well as a cash alternative for investors since its introduction, despite having to navigate an aggressive monetary hiking cycle, a bubbling banking crisis, US sovereign debt downgrade, and emerging new wars

- As the hiking cycle draws to a close, we believe now more than ever that the Liquid+ strategy has a strong chance to outperform cash over the following years

- Higher starting yields of today are reminiscent of the post-2006 Fed pause; Bonds had performed well with good risk-adjusted returns in the following years

- We also consider long-duration exposure premature, considering that (a) the yield curve remains inverted, (b) economic data continues to support the soft-landing narrative, and (c) the fiscal trajectory of the US remains a concern

- The Liquid+ strategy of short-duration/ high-grade credit remains the best way to position one’s Fixed Income allocation for this next phase of the policy cycle

Related insights

Navigating rough seas. It was while the world was wrestling with the highest inflation in 40 years that we proposed the unintuitive Liquid+ strategy back in September 2022 – a focus on short-duration, high-quality Bonds as a complementary alternative for Cash, giving investors both yield and liquidity in an age of ever-growing volatility. Certainly, pro-bond strategies amid high inflation were not consensus at the time. It was also not without trial; the world has since had to navigate an aggressive monetary hiking cycle, a bubbling banking crisis, US sovereign debt downgrade, and emerging new wars that repeatedly put the whole asset class of Fixed Income to the test. Now that we are approaching the end of the hiking cycle, we find it apt to briefly review how this Liquid+ strategy has performed for investors since.

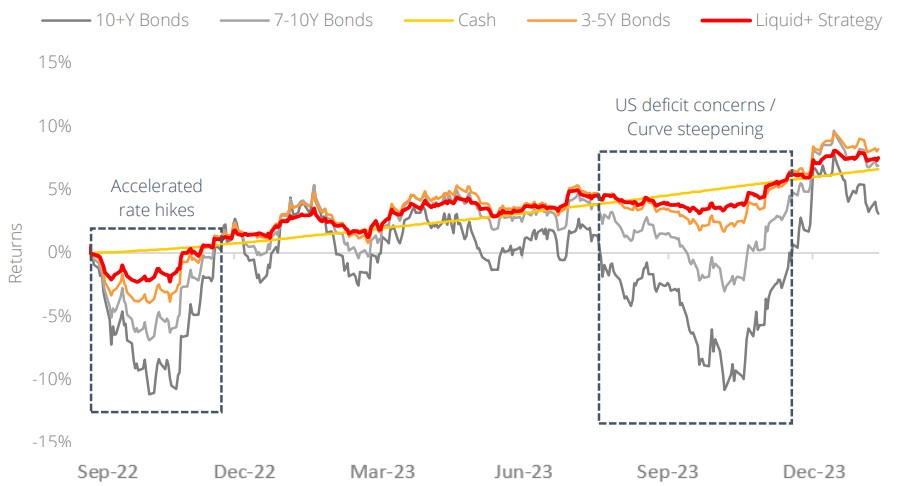

Figure 1: Liquid+ strategy has provided steady returns on relatively low volatility

Source: Bloomberg, DBS

Liquid+ strategy was fit for purpose. While returns on the strategy were almost immediately tested by the hawkish Fed, we note that they have ultimately kept pace with – and even exceeded – returns on cash in this period. Most importantly, the short-duration strategy insulated Fixed Income investors from two significant episodes of large drawdowns faced by longer-duration Bonds, first with the accelerated Fed hikes over 2H22, as well as the sharp yield curve steepening in 2H23 from US deficit concerns. We believe that this is how investors’ bond allocations should function in their portfolios – providing decent price stability with high recurring income despite the occurrences of unanticipated risks across the global markets.

Liquid+ beyond the hiking cycle. Since it has performed commendably despite steeply rising rates, we believe even more now with discussions centered around rate cuts, that the Liquid+ strategy will stand a more than adequate chance to outperform cash over the following years. Yields today remain at elevated levels, providing a good set-up for future returns in Fixed Income judging from past observations (Figure 2).

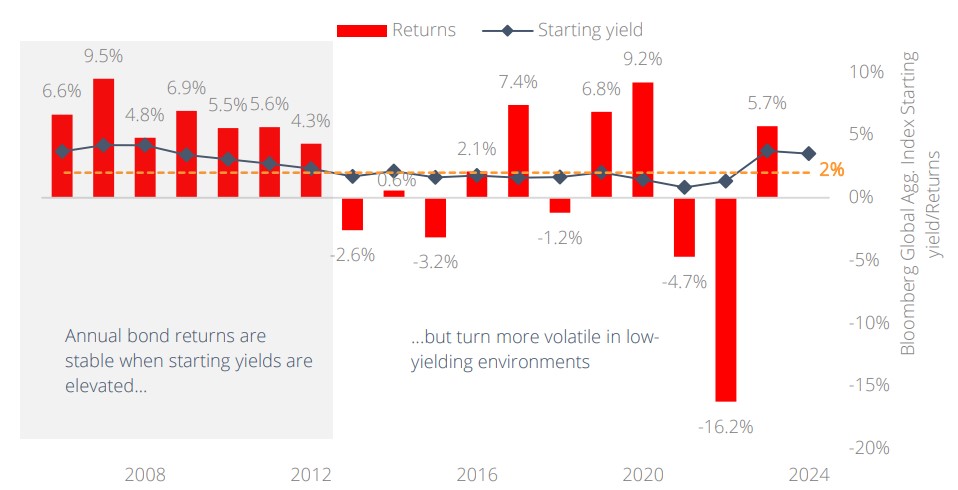

Figure 2: Yields are high enough to maintain stable returns for Bonds

Source: Bloomberg, DBS

Bonds will benefit from higher starting yields. . In the 10-year period from 2013, annual returns for Bonds have fluctuated with a volatility that is unbecoming of what should be the stable portion of a balanced portfolio. This was because yields were anchored by close to zero-bound rates in this period, leaving insufficient coupon returns to mitigate against interest rate volatility and price fluctuations. The higher starting yields of today hearken back to the post-2006 era when rates were held at similarly elevated levels – bond returns in the following years were stable and positive, giving strong risk-adjusted returns for Fixed Income investors. The Liquid+ strategy – we believe – would benefit from similar tailwinds in the years to come through the normalisation of interest rates.

How long before we go long? No doubt, investors concerned with recession would find long-duration Bonds enticing for that expression. We believe this to be premature, considering that (a) the yield curve remains inverted, (b) economic data continues to support the soft-landing narrative, and (c) the fiscal trajectory of the US remains a concern, especially in the vicinity of an election year. As such, it could be too early to conclude that the large drawdowns in longer-duration Bonds are behind us. We continue to advocate a Liquid+ strategy for one’s Fixed Income allocation as the best way to position for this next phase of the policy cycle.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.