Related insights

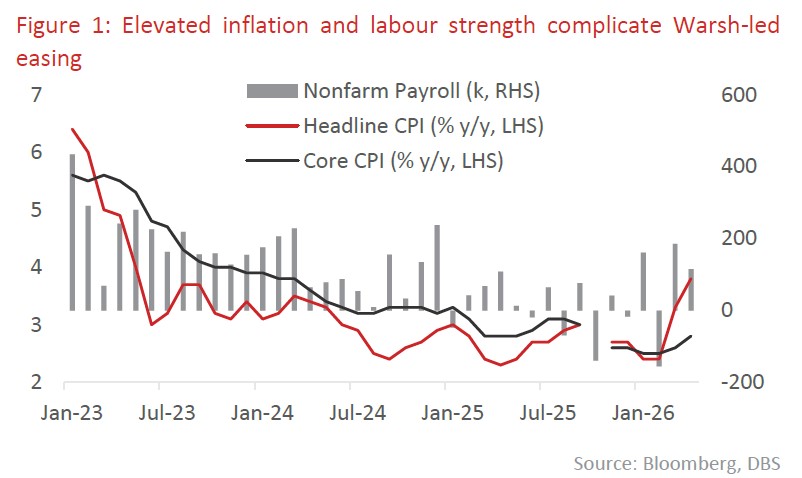

US: Labour market resilience amid sticky inflation to constrain a Warsh-led Fed’s easing cycle. After flip-flopping for several months, US nonfarm payrolls (NFP) finally registered two consecutive months of gains. April’s NFP hit 115k (vs a consensus of 65k), while the net negative revision was modest at 16k. Private payrolls were particularly robust, coming in at 123k. We note that job gains were broad-based, helping to keep the unemployment rate steady at 4.3%. The upshot is that the US labour market has not been materially affected by the Middle East conflict.

US inflation data for April surprised to the upside. Headline CPI rose 0.6% m/m, with annual inflation accelerating to 3.8% y/y in April from 3.3% y/y in March. Core CPI likewise came in above market expectations, rising 0.4% m/m. Importantly, the acceleration was not solely driven by food and energy prices, but reflected broader underlying price pressures, including core services. Meanwhile, AI-related supply bottlenecks have continued to push IT goods prices sharply higher. Rental costs are still rising, though part of the increase appears to reflect a one-off adjustment linked to anomalous data omitted during the October government shutdown. Against this backdrop, inflation expectations have continued to reprice higher. The 1Y breakeven inflation rate has rebounded from 2.98% last week to 3.23%, which is likely to constrain the easing cycle under the Warsh-led Fed.

Meanwhile, amid various trade deals and exemptions, US tariff collections have been ebbing since last October. Following the February Supreme Court ruling invalidating tariffs imposed under the International Emergency Economic Powers Act, and the May court ruling declaring section 122 tariffs illegal, customs duty collections are likely to decline further in the coming months. Expectations that tariffs could generate at least 1% of GDP in revenues to support the US fiscal position will need to be scaled back. These developments would add further pressure on the budget deficit.

The focal point for a shift in sentiment will be the Trump-Xi Summit in China on 14-15 May. The Centre for Strategic & International Studies has framed the agenda as the US’s “Five Bs” (Boeing, beef, beans, Board of Trade, and Board of Investment) vs China’s “Three Ts” (Taiwan, tariffs, and technology). Markets are looking for more than just rhetoric. Investors want a concrete mechanism to manage trade relations and limit further tariff escalations, an easing of US semiconductor export curbs, and a loosening of China’s grip on rare earth shipments. Ultimately, the prize is a joint diplomatic signal that provides an “off-ramp” for the Iran conflict, as reopening the Strait of Hormuz could finally set crude oil prices on a sustainable path below USD100/bbI.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.