Related insights

- Research Library24 Jun 2026

- USD Rates: Flight-to-safety unlikely to last 24 Jun 2026

- DBS Stock Pulse: Déjà vu for the Nasdaq buy-the-dip trade?24 Jun 2026

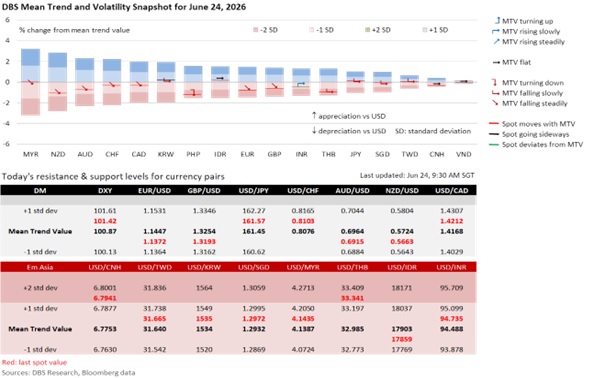

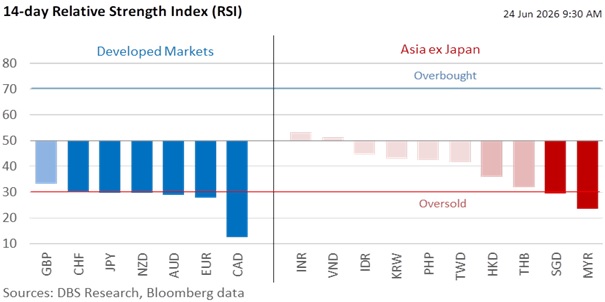

The DXY Index has risen by 1.3% to 101.41, its highest level since May 2025, following the hawkish FOMC meeting on June 16-17. However, the US exceptionalism narrative pushing this USD rally is not supported by the stock market rout amid Fed-hike worries. The futures market has priced in a 54.6% chance of a 25-bps hike to 4.00% at the September 16 FOMC meeting. EUR/USD sank to 1.1380 overnight from its pre-FOMC high of 1.1622 last week, driven by dovish comments by European Central Bank President Christine Lagarde not to expect a back-to-back cut in July. Markets are on alert for JPY intervention after Japanese Finance Minister Satsuki Katayama said that she had a phone call with US Treasury Scott Bessent about taking bold steps on currencies if needed.

Following a 10% sell-off in South Korea’s KOSPI to a two-week low, the intensive unwinding of crowded semiconductor trades spilled over into the US. The Nasdaq Composite Index fell for a second consecutive day by 2.2% to 25,587.04 overnight, more than Monday’s 1.3% decline, driven by increased investor doubts regarding the long-term return on investment for hyperscalers’ heavily leveraged AI infrastructure expansion. Interestingly, USD/KRW rose only 0.1%, with upside capped slightly above 1540 after last week’s FOMC meeting amid exporters’ USD selling. AUD/USD broke below the critical 0.70 mark due to its structural characteristics as a cyclical and risk currency.

The US Treasury 2Y yield eased 2.7 bps to 4.198% while the 10Y yield fell 1.2 bps to 4.497% on another 1.1% decline in Brent crude oil prices to USD 77.10 per barrel, bringing it closer to the 72.50 level before Operation Epic Fury at the end of February. US average gasoline prices continued to decline to USD 4.58 per gallon overnight, down from their peak of USD 5.18 on May 20, but remained above end-February’s level of USD 3.52.

The recent post-FOMC market turmoil could validate Fed Chair Kevin Warsh’s long-standing critique that heavy forward guidance effectively converts a data-dependent central bank into a market-handholding captive. By attempting to pre-commit to a policy trajectory, the Fed inadvertently breeds a market echo chamber that prices in rigid central bank promises rather than evolving economic fundamentals. This leaves the current setup vulnerable to any surprises in tomorrow’s PCE inflation print, where markets are aware that lower crude and pump prices have created a disinflationary veneer ahead on the headline front.

Quote of the Day

“Those who have knowledge, don't predict. Those who predict, don't have knowledge.”

Lao Tzu

June 24 in history

A bloodless coup in 1932 abolished the absolute monarchy in Thailand, transitioning the nation into a constitutional monarchy.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related insights

- Research Library24 Jun 2026

- USD Rates: Flight-to-safety unlikely to last 24 Jun 2026

- DBS Stock Pulse: Déjà vu for the Nasdaq buy-the-dip trade?24 Jun 2026

Related insights

- Research Library24 Jun 2026

- USD Rates: Flight-to-safety unlikely to last 24 Jun 2026

- DBS Stock Pulse: Déjà vu for the Nasdaq buy-the-dip trade?24 Jun 2026