Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

The Bank of Thailand (BOT) hiked its policy rate for the sixth consecutive time by a gradual 25bps to 2.00% during its May 31 meeting. This increase brought the cumulative monetary tightening to 150bps since the first hike in this cycle in Aug22, and the policy rate is around an 8-year high. With policymakers still flagging the need to monitor upside inflation risks and continued economic recovery, we maintain our terminal rate forecast of 2.25% for now. Piti Disyatat, assistant governor at the BOT, told a briefing after the interest rate decision that ‘It’s still appropriate to continue the current strategy that we have adopted,’. Yet, our expectations imply that Thailand’s interest rate hiking cycle is closer to a pause. We highlight three key takeaways from the BOT’s policy decision.

First, the decision to raise the policy rate was again unanimous within the BOT’s Monetary Policy Committee (MPC). This suggests broad consensus with respect to the assessment of Thailand’s post-pandemic economic recovery and concerns regarding elevated underlying inflation. We will be watching the upcoming meeting minutes, which will shed further light on the detailed discussions within the BOT’s MPC.

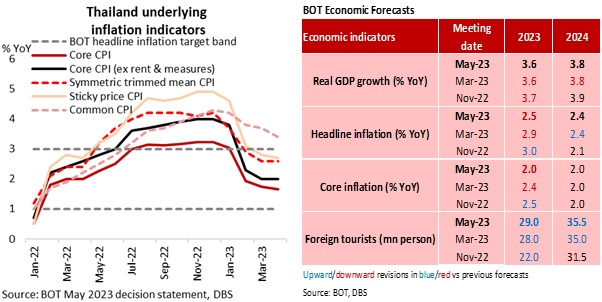

Second, with respect to the BOT’s economic assessment and forecasts (see table), policymakers dialled down their 2023 headline and core inflation projections, but interestingly retained their attention on elevated underlying price pressures and potential upside inflation risks. The BOT’s various underlying inflation gauges already moderated back to its 1-3% headline inflation target in recent months, implying that upside price pressures and threats to price stability are not as acute as previously. Yet, policymakers continue to see upside risks from three areas. These include: 1) prolonged elevated core inflation affecting price-setting behaviour, 2) greater demand pressures and cost pass-through from economic expansion, and 3) upcoming government policies. For growth, the BOT’s 2023 and 2024 forecasts were unchanged, with some upward tweaks in foreign tourist arrivals expectations.

Third, the BOT assistant governor Piti Disyatat also mentioned that Thailand should have positive real interest rate when the economy returns to equilibrium. As we have flagged out in ‘Thailand chartbook: Elections, recovery vs stability risks’, real policy rates are returning to positive zones but still below pre-pandemic levels. We suspect financial stability risks from low real rates would have been part of the BOT’s deliberations, which would also compel them to restrict monetary policy further, although policymakers left the room open to shifts in their future monetary policy stance. In our view, the biggest uncertainty to the Thai economy right now is from the formation of the government after the May 14 general elections. Any delays could shift the economic outlook, and could swing the BOT towards a wait-and-see approach temporarily.

Topic

Explore more

E & S Macro StrategyThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024