- 3Q25 earnings momentum was strong, with engine OEMs outperforming on aftermarket and prompting multiple guidance upgrades

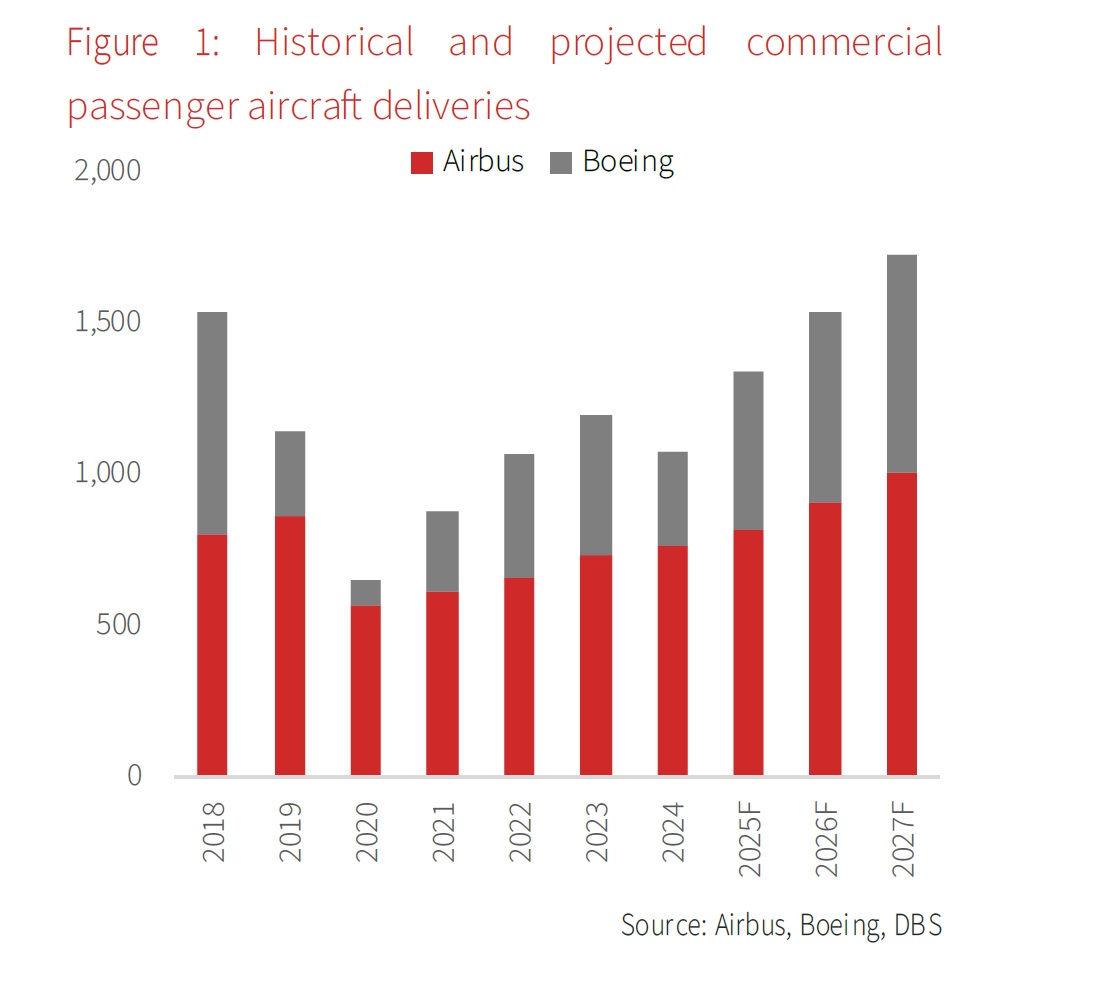

- Airbus reaffirmed its 820-aircraft target and Boeing returned to positive free cash flow, though execution risk remains with the 777X delay

- Aftermarket strength remains broad-based, driven by an expanding installed fleet, higher shop visit requirements and rising material throughput, while tariff impacts remain well contained through effective mitigation measures

- Aerospace sector is poised for growth in 2026, supported by c.4% global traffic expansion, rising aircraft utilisation and improving propulsion supply chains that enable higher aircraft deliveries

- We continue to prefer aircraft OEMs as rising build rates and improving engine availability offer greater operating leverage, while engine OEM margins may moderate with a higher OE mix. Defence procurement adds stability despite easing geopolitical tensions

Related insights

The commercial aerospace sector remains well positioned for growth into 2026 despite tariff noise. The demand backdrop remains constructive: global air traffic is expected to grow at around 4% in 2026, with aircraft utilisation continuing to firm up and supporting higher engine flying hours. Supply-chain conditions are steadily improving, particularly in propulsion, enabling a clearer path for increased aircraft deliveries next year as engine availability normalises. Aftermarket revenues are expected to see solid growth, supported by a larger installed fleet, higher shop visit requirements and rising material throughput across major engine platforms. Tariff impacts are proving manageable, with manufacturers highlighting effective mitigation through pricing mechanisms in long-term agreements, diversified global sourcing and operational workarounds that limit direct exposure. Taken together, these dynamics position the sector for continued top-line and cash-flow growth in 2026, even as residual bottlenecks and macro uncertainty persist.

Commercial aerospace companies mostly delivered strong updates in 3Q25, with engine OEMs clearly outperforming airframe OEMs. For the engine makers, aftermarket strength remains the defining theme, with shop visits, spare parts demand and LTSA-driven revenue running ahead of expectations as material availability improves and the installed base expands. This has driven guidance upgrades across GE Aerospace, Safran, RTX, and Rolls-Royce. Airbus reiterated its 820-aircraft delivery target, supported by a clearer engine outlook which also enables the completion of gliders in 4Q25. Boeing generated positive free cash flow for the first time in years and received Federal Aviation Administration (FAA) approval to lift 737 output to 42 per month, but is not completely out of the woods after taking a USD4.9bn charge and delaying the 777X to 2027. Overall, most companies maintained or upgraded guidance, indicating tariff effects are manageable relative to upbeat demand and improving aftermarket and production cadence.

We remain optimistic about the aerospace sector into 2026 but still prefer the aircraft OEMs. Aftermarket activity is set to remain solid, supported by persistent reliability issues on new-generation narrowbody engines, ongoing GTF fleet management, an ageing fleet and favourable economics for older aircraft in a low jet fuel environment. However, margins for engine makers are likely to moderate as the mix shifts toward higher OE deliveries. In contrast, aircraft OEMs should see growth accelerate from rising build rates and improving engine availability, underpinned by stronger operating leverage as production ramps. Defence procurement is also expected to remain robust despite a de-escalation of geopolitical tensions, adding stability to the sector’s earnings base and reinforcing our relative preference for the OEMs.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.