- Expectations of Fed rate cut at the September FOMC meeting set the stage for yield sensitive assets like REITs to return to prominence

- Impact of higher interest costs have peaked; REITs with lower hedge profiles to benefit ahead of others

- Investors to refocus on property fundamentals; suburban retail, data-centres, and logistics are well-placed to deliver steady growth

- Merger and acquisition activity could pick up, presenting upside surprise to REITs’ distributions

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

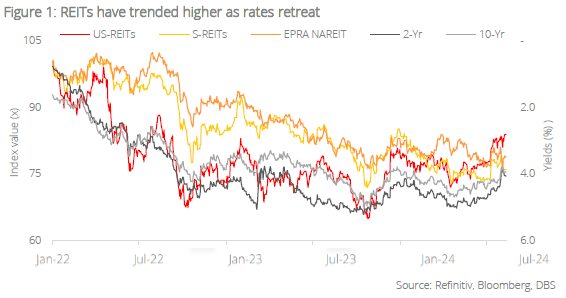

REITs shine as interest rates head lower. With inflation tapering off and other macro datapoints in the US showing signs of softening, the Fed has turned visibly dovish, signalling their readiness to cut interest rates at the Federal Open Market Committee (FOMC) meeting in September. With global interest rates now on a normalisation trend amid declining macro headwinds, we have seen a pick-up in performance for REITs in recent weeks. Given close inverse correlation between interest rates and REITs prices, we remain confident that REITs, especially those in Hong Kong and Singapore offering yields of 6-7% on average, will continue to see strong inflows from investors in the months ahead as they seek high yielding opportunities.

Interest costs peaked; lower-hedged REITs positioned to benefit. The impact of rising interest costs on Singapore REITs (S-REITs) appears to have peaked in the first half of 2024. Given recent declines in short-term interest rates across Asia and the expectation of further cuts in 2025, refinancing costs are likely to stabilise. Assuming a typical three-year loan rollover, the overall cost of borrowing could decrease, particularly for REITs with higher exposure to floating rates. Throughout the first half of 2024, REIT managers have been gradually unwinding hedges, positioning their portfolios to benefit from falling rates. Our sensitivity analysis indicates that for every 100 bps drop in interest rates, S-REITs could realise up to a 2.4% increase in earnings in 2025, a factor that is not yet reflected in current valuations.

Investors to refocus on property fundamentals; suburban retail, data centres, and logistics are well-placed to deliver steady growth. With declining macro headwinds, investors will likely refocus on underlying property fundamentals. Across Singapore and Hong Kong, we like suburban retail subsectors where growth is underpinned by resilient retail tenant sales amid limited new retail supply, driving the landlords’ ability to raise rents. In addition, secular trends underpinned by e-commerce, Generative Artificial Intelligence (Gen AI) will drive continued demand for data centres and logistics properties. We turn more cautious on hotels with expected softness in demand as most hoteliers have become more price sensitive, given the slower-than-expected pick-up in China demand.

Merger and acquisition activity could pick up, presenting upside surprise to REITs’ distributions. Lower interest rates will be a boost to the overall operating environment as it spurs more transaction activities. As the cost of capital turns more conducive for REITs to pursue accretive acquisitions, S-REITs will be back in a ‘virtuous cycle of growth’. This has not been priced in by investors and will present an upside surprise should it transpire eventually.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025