- Equities: US equities experienced a sharp decline over rising tensions in the Middle east; China equities rose on positive economic data

- Credit: US Treasury’s influence over the supply of short-term bills versus long-term bonds have quietly neutralised the increased duration risk that QT supplies, damping the effects of curve steepening

- FX: Amid EUR’s resilience, the DXY failed to gain traction despite constructive sentiment towards the USD

- Rates: UST yields receive a boost as NFP beat expectations; Recent data suggesting a more calibrated easing cycle amidst rising no-landing risk

- The Week Ahead: Keep a lookout for US Change in Initial Jobless Claims; Japan Industrial Production

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

US equities fell amid escalating tension in Middle East. On Thursday (4 Apr), the US equity markets experienced a sharp decline as concerns of potential escalation in the Israel-Hamas conflict sent oil price surging above USD90 per barrel. The S&P 500, Dow Jones, and NSADAQ notched weekly losses of -1.0%, -2.3% and -0.8% respectively. The upcoming US CPI data is likely to dominate markets sentiment this week as investors assess its implication on Fed rate cuts decision.

China equities, on the other hand, rose as data signalled signs of the economic recovery. The Caixin Manufacturing Index rose to 52.7 in March, marking its fifth consecutive expansion. Furthermore, the official NBS Manufacturing PMI also came in higher than expected (50.8 vs 49.1 consensus) and entered expansionary territory for the first time since Sep 2023. These robust data heighted expectations for China’s economic resurgence. The SHCOMP and CSI 300 both gained 0.9% for the week.

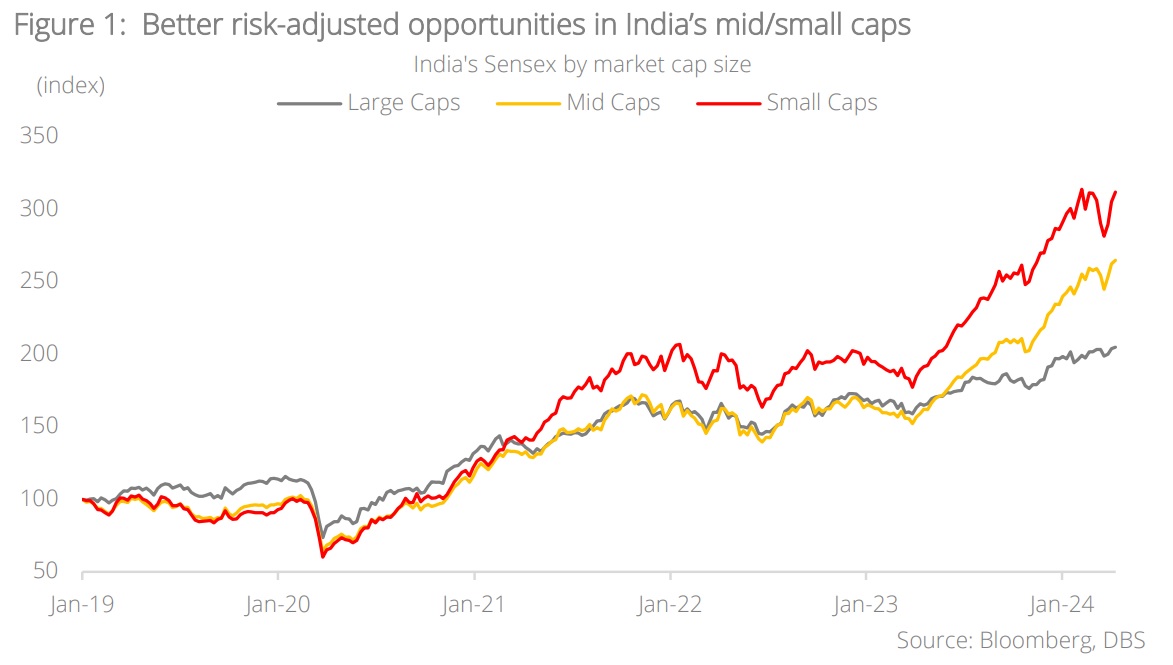

Topic in focus: India’s homegrown opportunities. India equities have been resilient thus far and can be expected to sustain its strong performance. To navigate the elevated valuations while capitalising on attractive growth prospects, we recommend exposure to India via mid/small cap mutual funds which can capture the opportunities brought about by the fifth largest economy in the world by nominal GDP, and yet with significant room to grow as it lags in per capita income. These funds are particularly appealing to domestic investors given ample liquidity in the economy and offer better returns on a risk adjusted basis. Recent regulatory cautions regarding such funds are expected to prompt enhanced risk management practices.

Key sectors contributing to the growth in the mid/small cap space include technology, consumer goods, and services. India’s financial sector, including banks and non-banking financial institutions, play a crucial role in supporting economic activities. We see bright spots in well-established financial institutions as well as fintech companies innovating in the sector. In this digital transformation era, companies involved in engineering and research and development (ER&D), as well as those benefitting from AI and digital tech spend should perform well. A rising middle class and increasing urbanisation trends in India contribute to the growth of the consumer goods and services sector.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024