Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Government to support economic revival. At the close of the National People’s Congress, the newly appointed Premier Li Qiang announced a GDP growth target of 5% for 2023; this came on the heels of a 3% growth recorded by the world’s second largest economy in 2022.

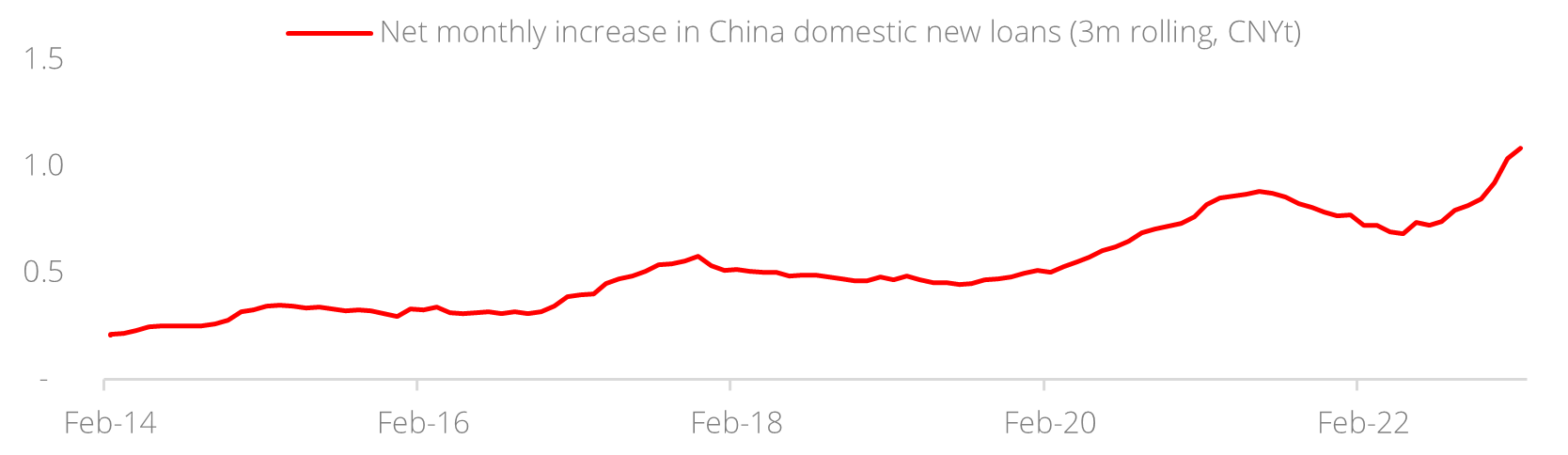

The government’s commitment to spur growth is evident from the sharp increase in new loans of CNY5.8t between December 2022 and February 2023, representing a 98% y/y increase.

Figure 1: Net monthly increase in domestic new loans

Source: Bloomberg, DBS

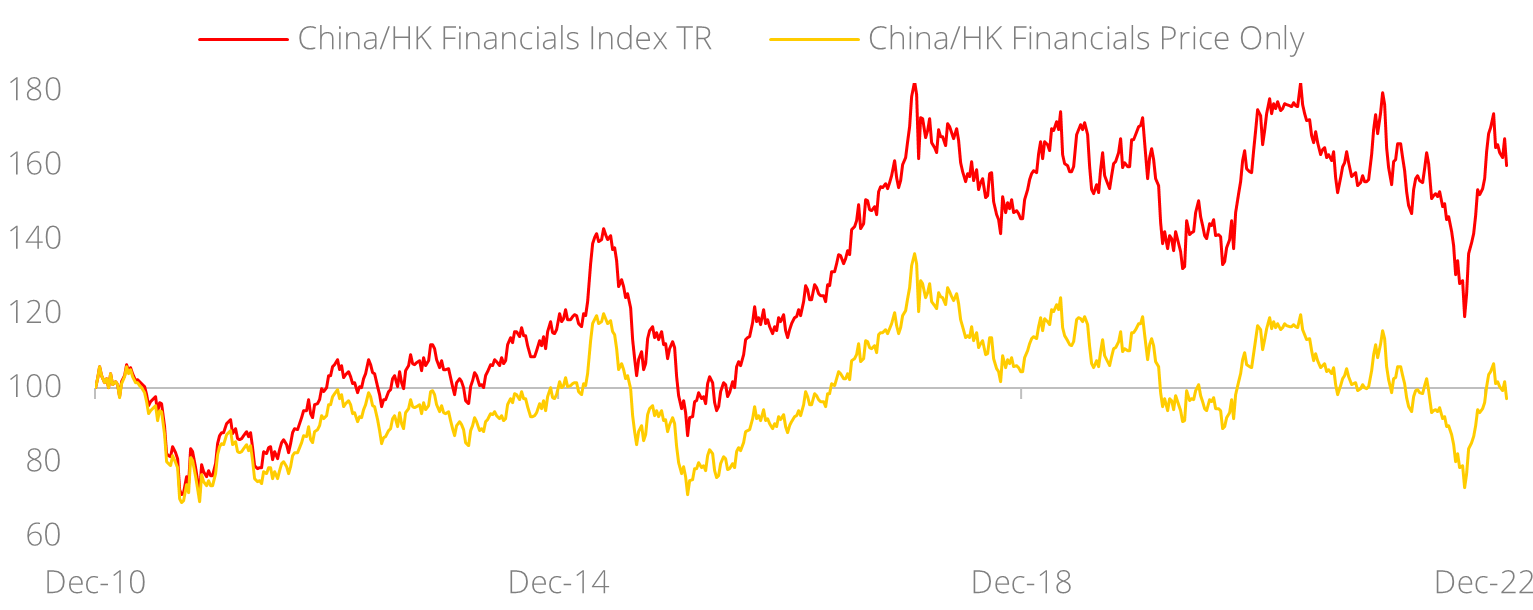

China financials as a sector plays an important role in the CIO Barbell strategy construct as it delivers attractive and sustainable dividend yields (Figure 2). The total return from investing in China financials has been resilient during last year’s market rout as it concluded the year flat (Figure 3) despite declines in global equities (-18%) and Asia ex-Japan equities (-21%).

Figure 2: Attractive and sustainable dividend yields

Source: Bloomberg, DBS

Figure 3: China financials total return in 2022

Source: Bloomberg, DBS

Unscathed by banking debacle in developed markets

We maintain our stance that China’s large State-owned Enterprise (SOE) banks are substantially insulated from external shocks currently faced by banks in the developed markets, owing to the former’s traditional business models.

The majority of China banks’ revenue and balance sheets are domestic centric, anchored by conventional deposits and loans. Notably, China SOE banks are known for their strong local branding and nationwide branch networks with access to cheap Current Account Savings Account (CASA) funding, and the discipline to stay away from exotic deposits and loans. As such, they are unscathed by the debacles affecting Western financial institutions.

Our constructive stance on China large financials rests on the following fundamentals:

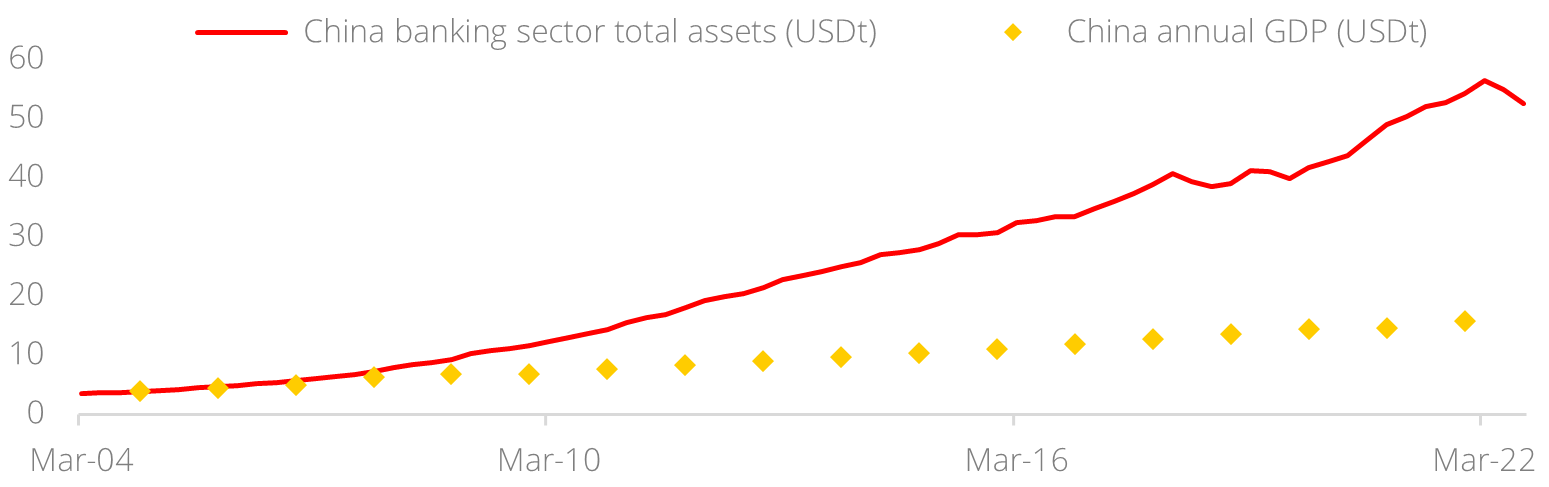

- Strengthening regulatory oversight. The government announced the establishment of a new financial regulatory agency—National Financial Regulatory Administration (NFRA)—to consolidate regulatory oversight of the world’s largest banking sector by asset value, bridging the gaps between multiple financial sector agencies which currently oversee different areas. As at 3Q22, China’s banking sector’s total assets stood at c.USD52t, an exceedingly important element in China’s economic ambitions (Figure 4).

Figure 4: A sector too important to fail

Source: Bloomberg, DBS

- Loan growth. The government has set a growth target for total social financing in 2023 to be in line with nominal GDP growth estimated at around 7%-8% where large commercial banks will play pivotal roles to supply the necessary funding. This bodes for a better outlook for loan growth and net interest income. As at February 2023, China’s total social financing had grown 9.9% y/y.

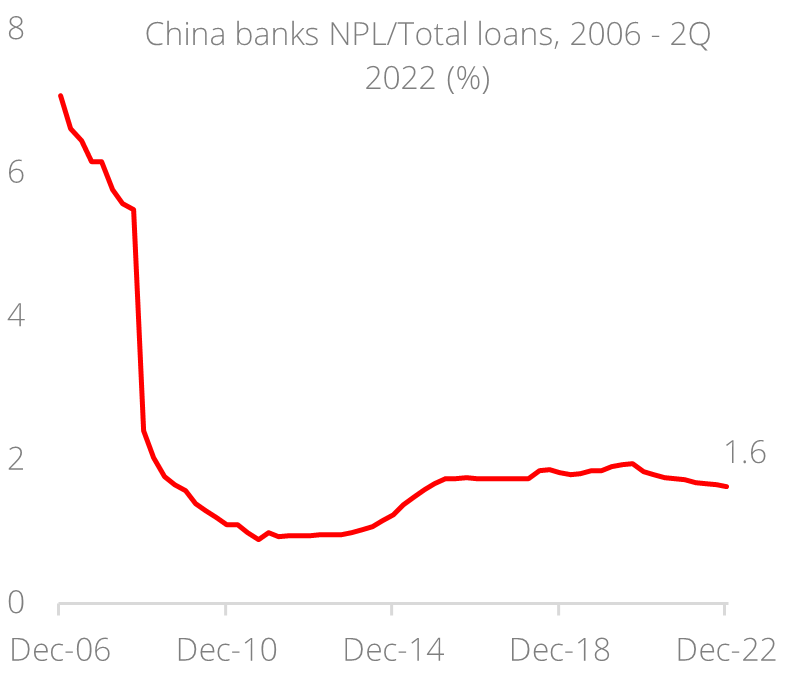

- Loan quality. Large state banks and the broad financial sector have their balance sheets predominantly anchored within China with minimal exposure to overseas assets and liabilities. The large banks have extended loans mainly to SOEs, government-linked projects, local large private sector enterprises, and consumer mortgages. These loans are usually of better quality and face low default risks even during past crises. The sector’s non-performing loan (NPL) ratio has stayed low at the range of 1.6%-1.7% over the past few years and is likely to remain (Figure 5).

Figure 5: Non-performing loans in check

Source: Bloomberg, DBS

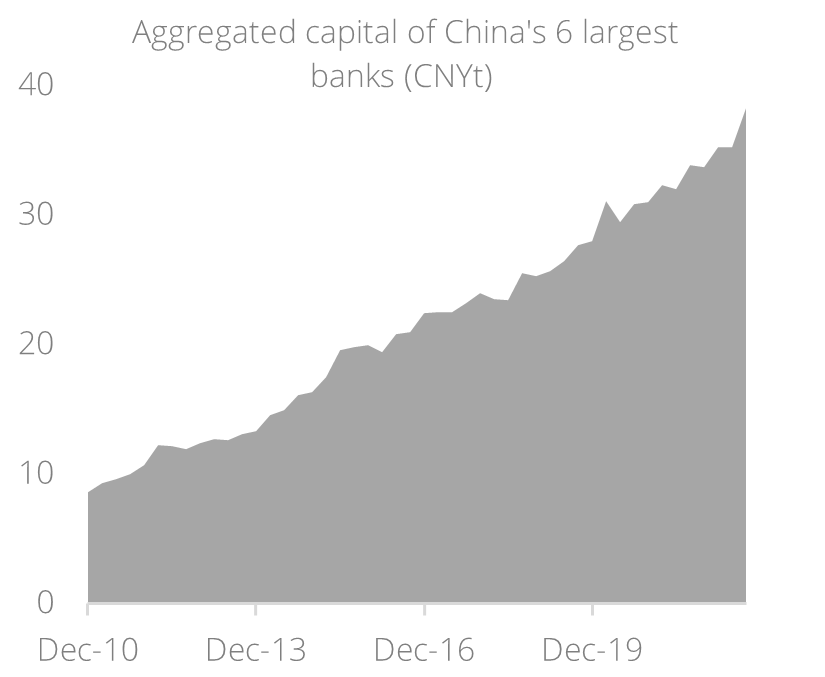

Figure 6: Strong balance sheet

Source: Bloomberg, DBS

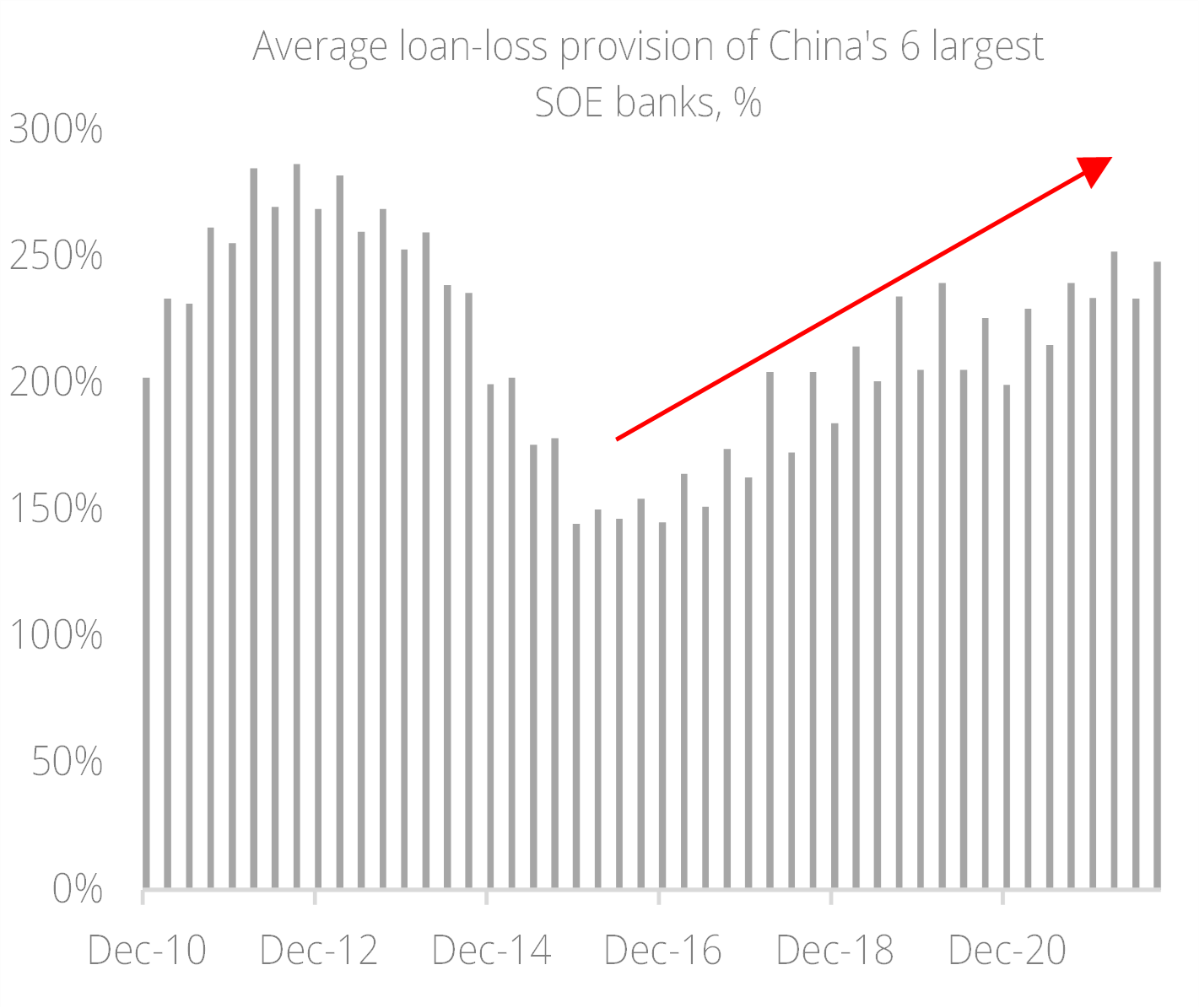

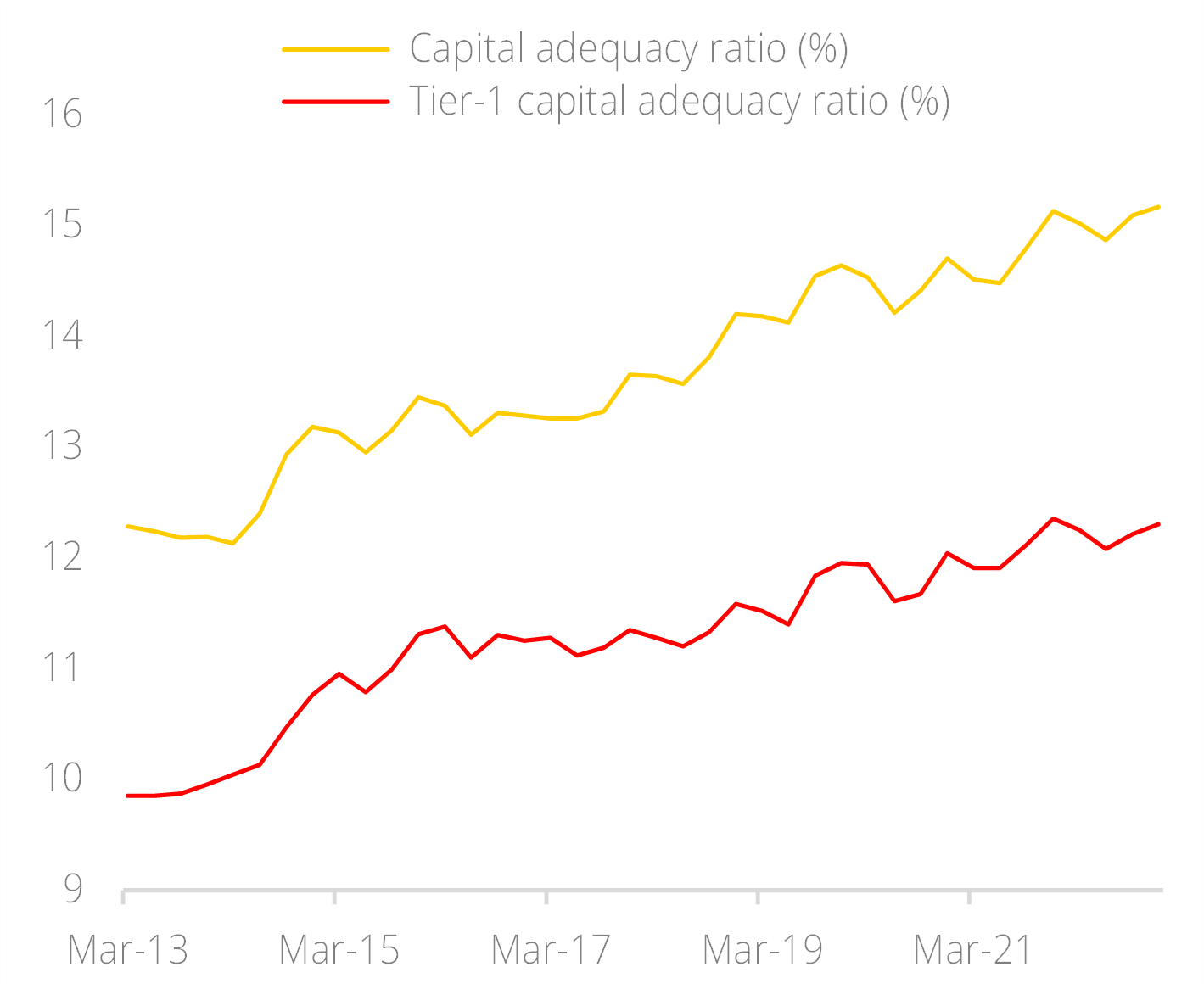

- Capital base. Between 2010 and 2022, the combined capital of China’s six largest banks had increased four-fold (Figure 6) and their loan loss provisions reached 250% (Figure 7). The banking sector’s capital adequacy ratio and tier-1 capital adequacy ratio improved further, registering 15.2% and 12.3% respectively as at 3Q 2022 (Figure 8). These figures reflect the sector’s resilience.

Figure 7: Buffered for loan losses

Source: Bloomberg, DBS

Figure 8: Well capitalised

Source: Bloomberg, DBS

- Yields. At the current price, China’s large SOE banks are rewarding investors with attractive and sustainable dividend yields of 7-8%. Over time, they have delivered appealing cumulative total returns to investors (Figure 9).

Figure 9: The power of dividends (2010 = 100)

Source: Bloomberg, DBS

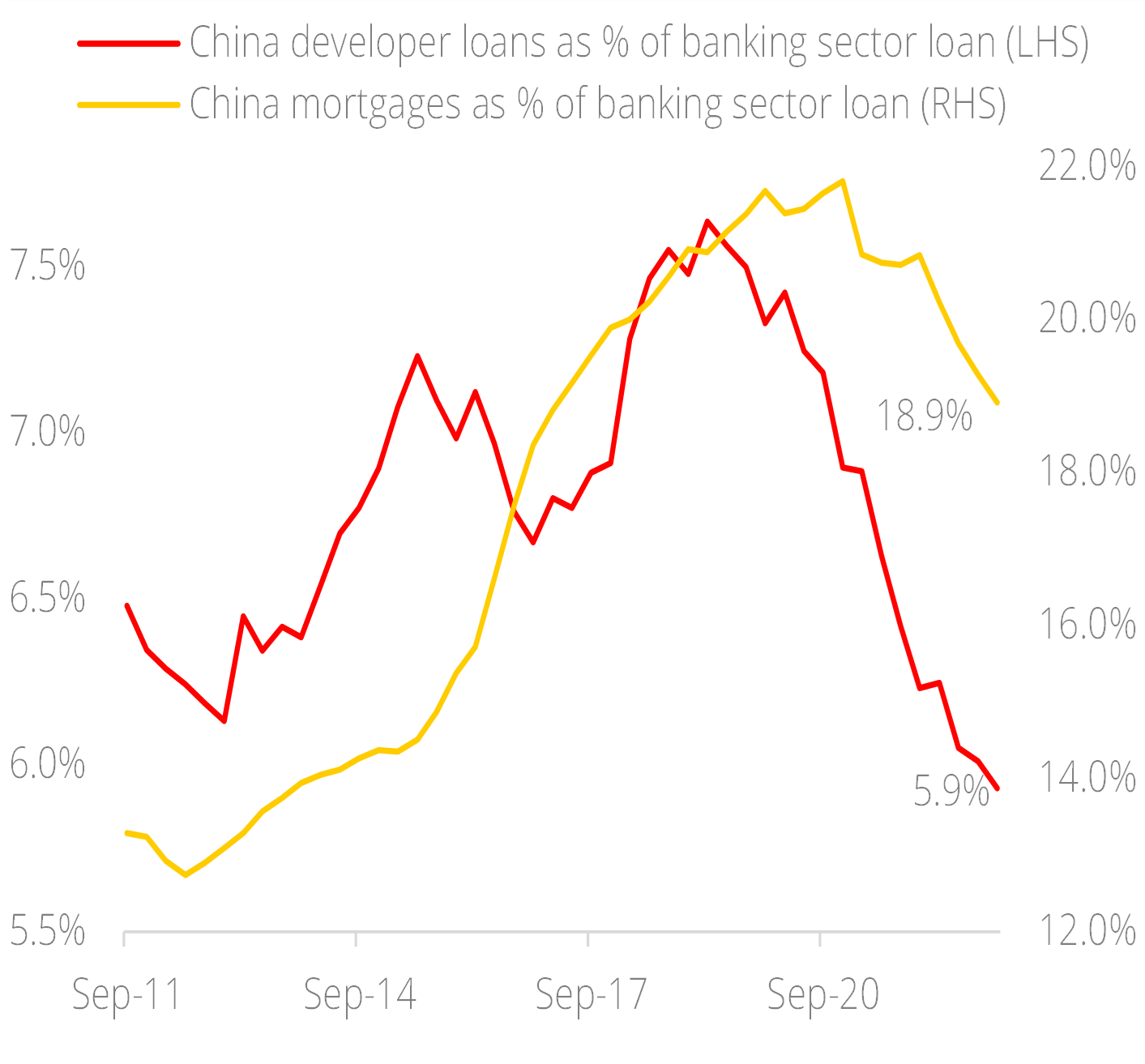

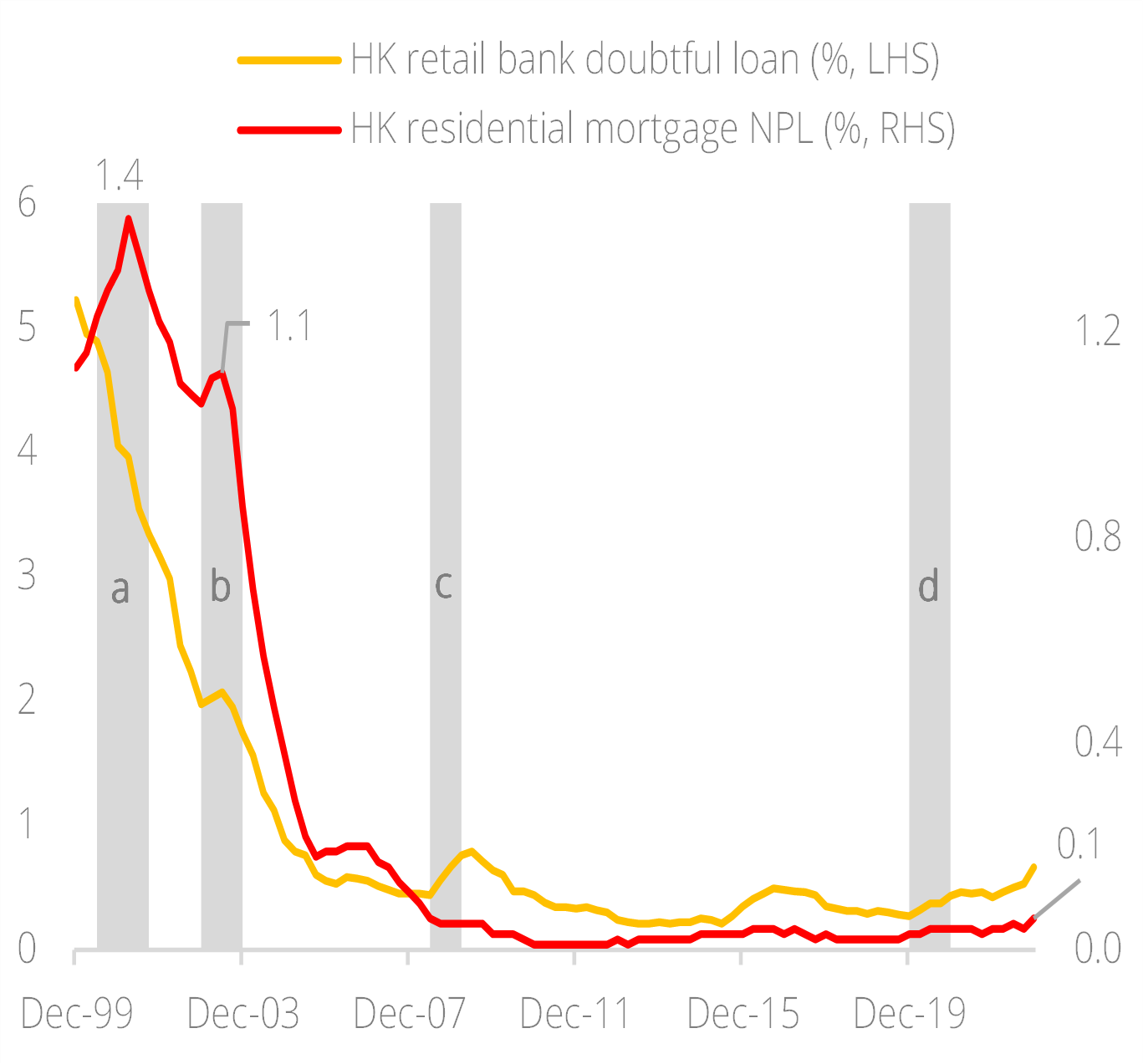

- Property loan exposure. China banks’ loan exposure to real estate developers declined to 5.9% at the end of 2022, a significant improvement from the peak of 7.6%. Exposure to mortgage loans have likewise declined to 18.9% from the peak of 21.8% (Figure 10). Using Hong Kong as a reference where residential mortgage NPL among commercial banks have remained low during past crises ((a) 2000 dot.com bubble, b) 2003 SARS pandemic, c) 2008 GFC, d) 2020 Covid pandemic (Figure 11)), we reckon the NPL of mortgages among China’s large banks should remain stable and low.

Figure 10: Exposure to property loans manageable and declining

Source: Bloomberg, DBS

Figure 11: Referencing Hong Kong banking sector as a guide for NPL outlook

Source: Bloomberg, DBS

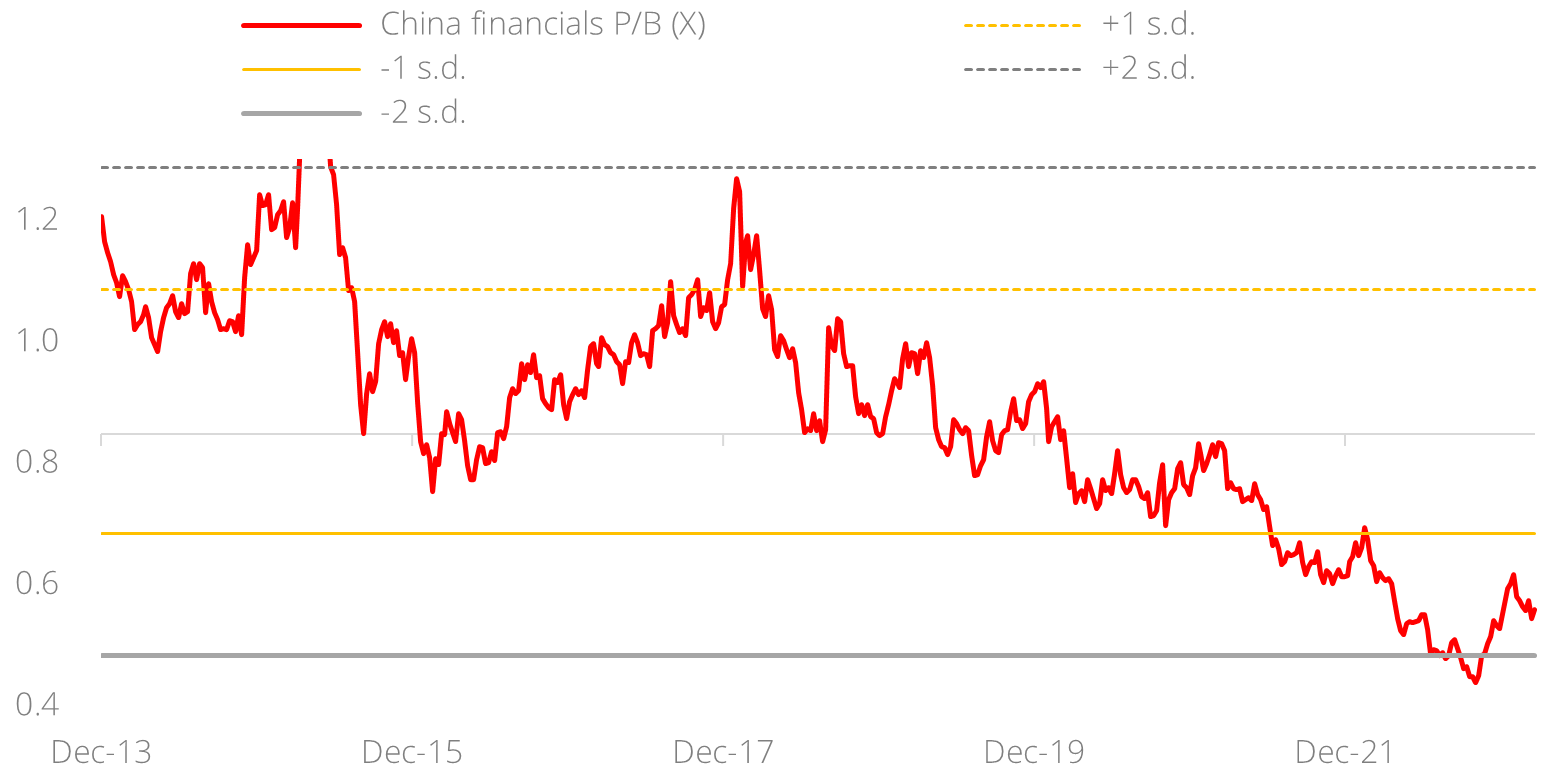

- Valuations. China financials trade at floor valuations. At a historical price-to-book ratio of 0.5x (Figure 12), the sector is valued at -1.5 standard deviation to historical mean. Similarly, the forward P/E ratios of 5x-6x against projected earnings growth of 11% over the next two years indicate that the market is pricing in a lot of pessimism which we believe is unjustified. These risk-reward metrics appear attractive by any standard.

Figure 12: Compelling valuations

Source: Bloomberg, DBS

Recommendations

China’s large SOE banks are well positioned as income generators in the CIO Barbell Strategy for their attractive and sustainable dividend yields of 7-8%. This is supported by the sector’s compelling valuations on the back of stable earnings growth of 5-6% over the next two to three years. As such, we continue to advocate China financials as part of a holistic portfolio strategy construct.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024