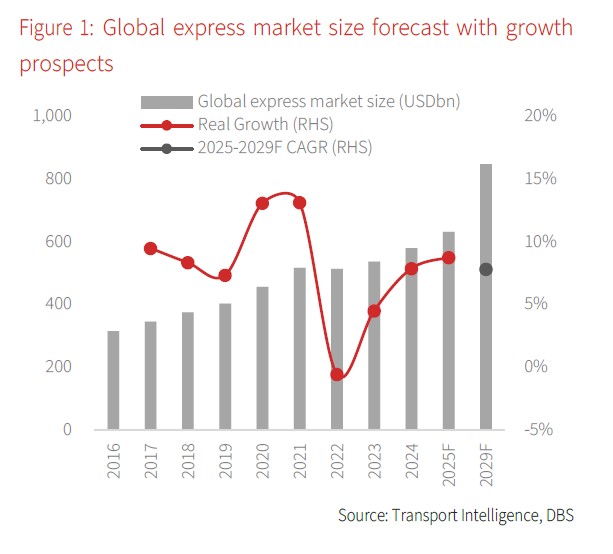

- The global express market is expected to deliver a robust CAGR of 7.9% over 2025-2029F, underpinned by thriving B2C demands

- Pricing strength and cost discipline supported strong results for US logistics giants; Chinese peers exhibited mixed performance amid regulatory reform

- Global logistics giants demonstrated pricing power and cost discipline to enhance profitability amid an evolving trade environment, while prioritising capital returns as a key focus

- Chinese peers are positioned for quality-led growth as regulators curb irrational competition, while accelerating overseas expansion to build global service capabilities

Sustained growth on e-commerce momentum. Despite the International Monetary Fund's (IMF) revised projection of a slowdown in global trade (in goods) growth to 2.0% in 2026F, the global express logistics sector is poised for robust expansion. The global express market is expected to deliver a 7.9% CAGR in 2025-2029F, following an elevated 8.8% y/y growth in 2025F. This resilience is underpinned by strong demand in the B2C segment, which is projected to grow at a substantial 10.8% CAGR, outpacing the sluggish 2.5% CAGR for the B2B segment.

China’s parcel volume growth is expected to moderate to c.10% y/y in 2026F as regulators curb irrational competition. In contrast, the US market is projected to grow at a 5% CAGR over 2025–2030F, supported by rising e-commerce penetration, which reached 22.0% in 2Q25 (vs 21.0% in 2Q23 and 21.8% in 2Q24).

Global leaders show pricing strength and cost discipline while Chinese players deliver mixed results. In the US, both UPS and FedEx posted stronger-than-expected results driven by a sharper focus on revenue quality and cost discipline. UPS reinstated its 4QFY25 guidance with confidence in execution, while FedEx has further upgraded its FY26 guidance, driven by its durable pricing power and structural cost actions.

In China, ZTO Express reported improvements in unit economics in 3QFY25, and remains well-positioned to ride the industry's shift towards quality-led growth. Meanwhile, J&T Global Express, with its extensive global network and efficient operations, has successfully captured the growing e-commerce demand. It delivered a robust full-year parcel volume growth of 67.8% y/y in Southeast Asia (SEA) and 43.6% y/y in new markets in 2025, compared to a more moderate 11.4% y/y in China. On the other hand, SF Holding and JD Logistics faced challenges, with upfront investments and strategic reforms weighing on their profitability.

Chinese logistics for growth; global peers for profitability and shareholder returns. China’s regulatory pivot since Jul 2025 towards quality-led growth and away from irrational competition should support improved pricing discipline and a gradual recovery in profitability for leading players. At the same time, Chinese players are accelerating overseas expansion pace to better serve robust cross-border e-commerce demand and capture market share despite trade frictions.

Global leaders such as UPS and FedEx continue to prioritise revenue quality and cost efficiency, focusing on higher-margin services and driving further productivity gains. Their strong commitment to shareholder returns should also support their share prices. FedEx has planned a 5% dividend increase in FY26 (its fifth consecutive hike) while UPS announced a USD1.0bn share buyback alongside USD5.5bn in dividends.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.