- Alcobev sales have generally grown on the back of inflation-led pricing uptick; but this tailwind is expected to wane in the coming quarters

- Sales volume remains under pressure amid soft consumer sentiments in various regions

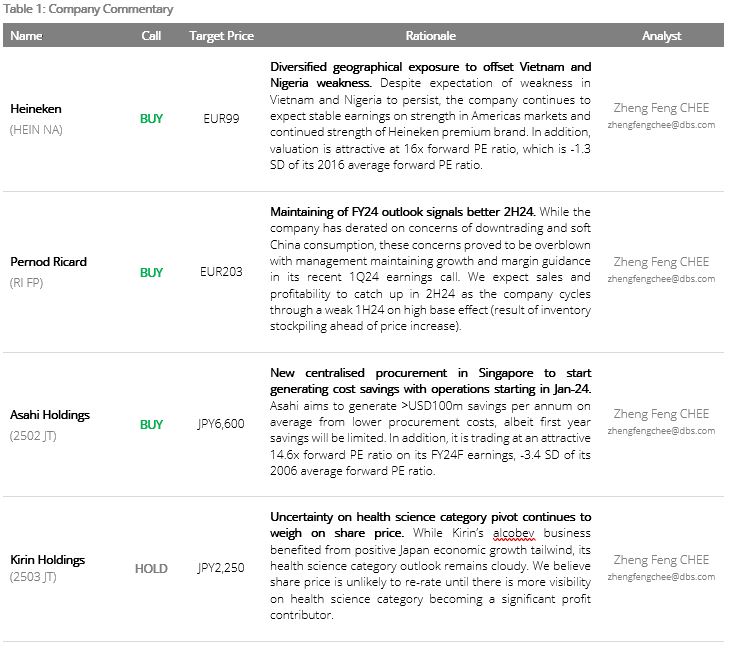

- Using 2006’s forward P/E as the baseline for “fair valuation”, companies trading at 1 standard deviation below this level offer attractive entry point for investors

- Companies with higher Americas and lower Asia Pacific (excluding Japan and India) exposure could see peer-leading earnings growth in the upcoming year

- Positive on select companies with attractive valuation and well-diversified brands portfolio and geographical mix

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Mixed 3Q23 results; but overall guidance of stable to low growth maintained. Global alcoholic beverage (alcobev) companies’ 3Q revenue generally improved by low single digits, as inflation-led pricing uptick helped to mitigate lower sales volume (which came on the back of soft consumer sentiments, particularly in Africa and Vietnam).

While volumes have picked up in China, it was on the back of reopening led on-trade recovery. Nonetheless, volume bright spots in Americas and India markets remain.

Overall, underpinned by inflation-led pricing uptick, companies are still guiding for stable to low single digit growth for FY23F. But we expect this pricing tailwind to wane over time.

Room for further downside ahead; major alcobev players trading at premium despite higher risk-free rate. Global alcobev companies currently trade at 20.6x forward P/E. This represents a premium compared to the 18.2x forward P/E seen in 2006 even though the prevailing risk-free rate was lower back then. Potential valuation de-rating is on the cards.

That said, select companies with established brands and management track records have already derated beyond 2006’s level as a result of company-specific headwinds. This presents attractive stock picking opportunities.

Using 2006’s average forward P/E as the baseline for “fair valuation” under a higher-for-longer interest rate environment, we believe valuations that are 1 standard deviation below this level will offer attractive entry point for investors.

Preference for players with well-diversified brand portfolios and geographical mix. Based on companies’ guidance, consumers from the US, Latin America, and Japan are expected to stay resilient while consumption in Africa and China will be more conservative in the near term.

Given uneven macro recovery, we believe companies that are highly diversified geographically and hold a good brand portfolio mix will report stable/growing earnings. In particular, we believe those with higher Americas and lower Asia Pacific (excluding Japan and India) exposure could see peer-leading earnings growth in the upcoming year.

Figure 1: Global alcobev players’ valuation

Source: Refinitiv, DBS

(Index constituents are 13 largest alcobev companies with >USD1b market cap in 2006 and global sales presence)

Table 1: Company Commentary

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024