- Oil prices expected to remain choppy in near term with firm downside support around USD85/bbl

- Escalation in the Middle East conflict poses severe risks to the oil market if it comes to fruition, and is not priced in fully yet

- Sanctions against Iran or disruption of trade routes along the Persian Gulf could see prices spike beyond USD100/bbl, but such scenarios are unlikely at the moment

- Despite risks of demand moderation in 2024 from a global economic slowdown and continued voluntary supply cuts by OPEC+ members, possible end of rate hikes cycle and weakening USD are bullish factors to watch out for

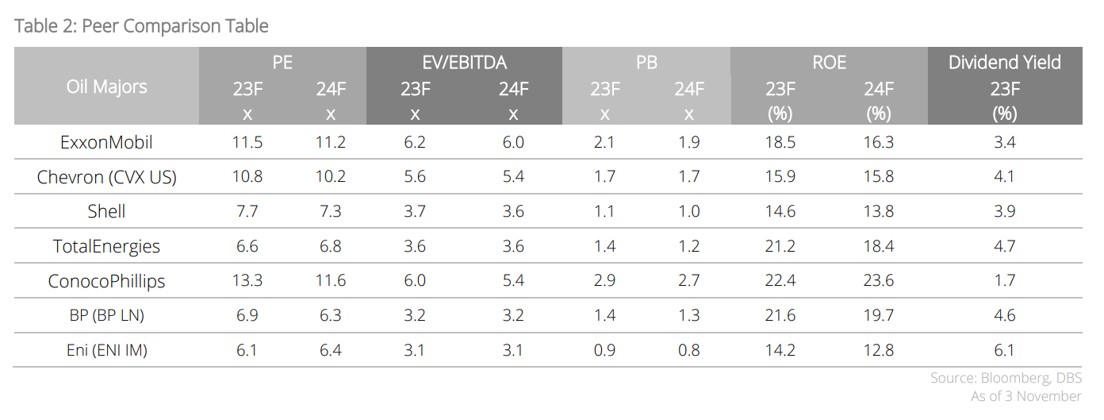

- Oil remains an important global commodity in the context of energy demand and security; oil majors are an important avenue for investors to express this positive outlook on the sector

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Geopolitical risk returns to the oil market. Following the eruption of armed conflict between Israel and Hamas forces in the Gaza strip, oil prices have been volatile, given the delicate position of the conflict close to the oil trading routes in the Middle East theatre. While the conflict has so far not snowballed into a bigger regional issue, the chances of that happening are not entirely zero.

In the near term, we believe oil prices will remain choppy, with firm downside support around USD85/bbl, given the geopolitical risk premium is unlikely to fade for a while. Supply side constraints continue to be a big factor, with both Saudi and Russia remaining committed to their supply cuts. Bullish factors for oil could also emerge from the possibility of a less hawkish stance from the Fed hereon and a weaker US dollar environment.

Upside scenarios possible for oil. As the conflict situation continues to evolve but without widespread escalation a month into hostilities, we keep our base case oil price forecasts (4Q23: USD90/bbl average for Brent, 2024: USD80-85/bbl average for Brent) unchanged, but we concede upside scenarios are possible. Iranian backed players in the region such as Hezbollah in Lebanon could get involved in the coming days, and if the US is able to take a tougher line with implementing sanctions under the Iran nuclear deal, we think oil prices could test the USD100/bbl level, unless there is Saudi intervention in terms of rolling back some of its voluntary production cuts.

In the worst-case scenario of trade routes in the Persian Gulf getting impacted owing to the intensification of a proxy war in the Middle East, we believe oil prices could spike towards USD130/bbl or higher, given that the Strait of Hormuz in the Persian Gulf is a key choke point for oil trade, but it could be too early for these doomsday scenarios in our view.

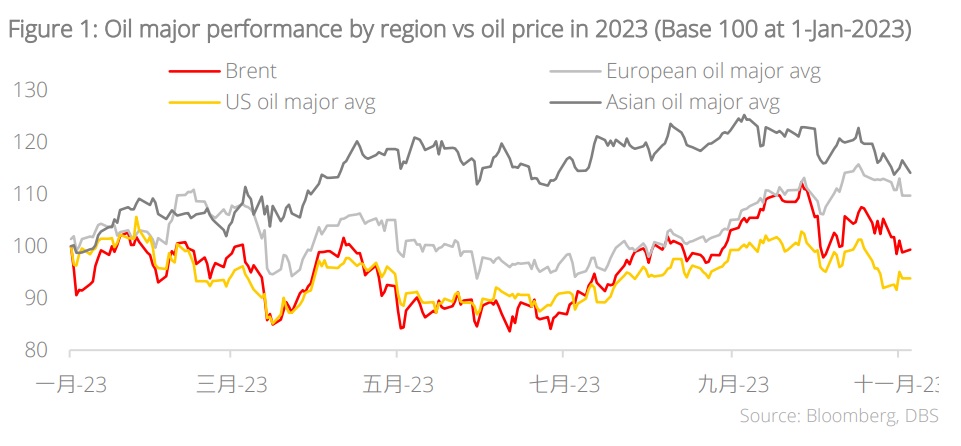

3Q performance for oil majors mostly stable, 4Q numbers could look better. After taking a breather for much of 1H23, share prices of oil majors have rallied in 2H23 after the combination of supply cuts from Saudi/ Russia and seasonally higher demand saw oil prices benefitting. The Israel-Hamas conflict led to a further spike in performance before some profit taking in recent weeks. 3Q23 results for most of the oil majors have thrown up no big surprises, and oil majors, especially in the US, remain committed to the hydrocarbon business with recent big M&A deals.

Even European oil majors – more advanced in the energy transition roadmap – have taken a step back to review their strategy and ensure their investments in Oil & Gas and cleaner energy sources are well matched, given that energy demand and energy security have come into spotlight in an increasingly fissured world. With average Oil & Gas prices likely higher in 4Q, as well as potentially better Oil & Gas trading and optimisation results given increase in volatility, performance and shareholder returns could surprise on the upside, providing further catalysts.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024