- The Israel-Hamas conflict provides a short-term boost for gold; possible further upside should regional instability ensue

- Inverse relationship between real rates and gold being challenged; gold has been displaying downside resilience to rise in real rates in recent months

- Debt sustainability issues in the US spell limited room for further substantial rate hikes thus limiting downside for gold

- Healthy gold demand in China and continued central bank buying in August add to fundamental tailwinds for the precious metal

- Continue to advocate for holdings in gold as a portfolio risk diversifier and black swan hedge

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Short-term boost from conflict in the Middle East. It is almost a foregone conclusion that gold benefits during tumultuous times given its status as a haven asset. Unsurprisingly, the recent escalation of Israel-Hamas tensions into a full-blown war boosted gold significantly, lifting spot prices almost 5% since 7 October (the inception of the latest flare-up). What remains uncertain at this point is how much more and how much longer gold prices will continue to rally from here. To a large extent, this would depend on how the conflict plays out – if it is contained and resolved within the next one to three months, then it is likely that the bulk of the rally is behind us.

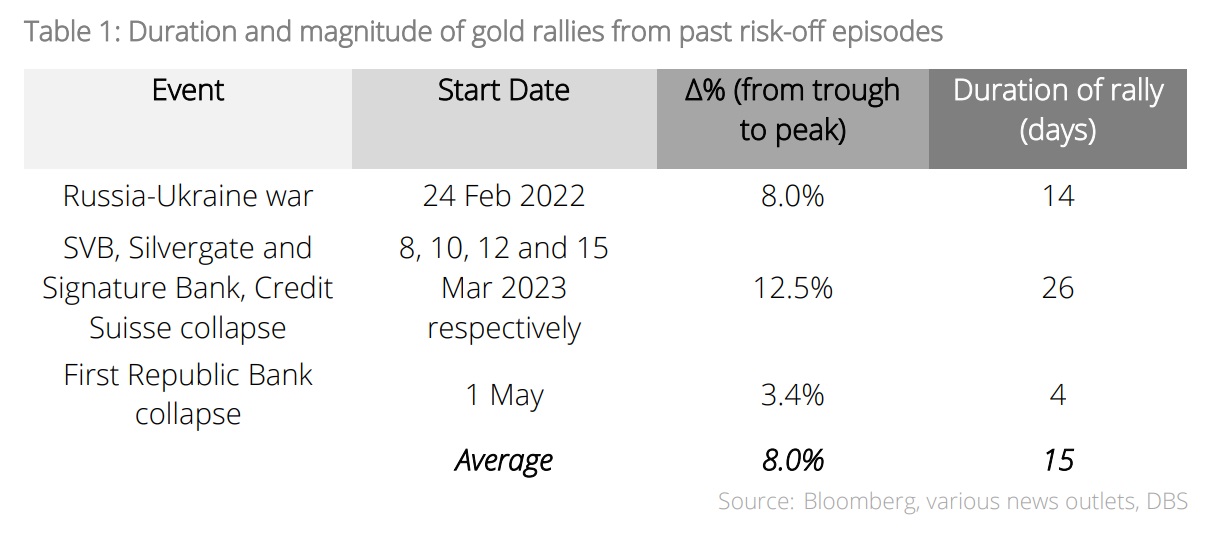

However, if the conflict spreads and becomes a destabilising force regionally, gold may yet have legs to run. Given the efforts by the US and its allies to contain the conflict, which include back-channel talks with Iran to warn against escalation, as well as the maintenance of a safe corridor open between Israel and north Gaza, our base case is that of a ring-fenced conflict rather than a regional crisis. On a more quantitative front, we analysed past risk-off incidents to see their effects on gold price and found that, such episodes resulted in a gold rally that lasted an average of 15 days (trough to peak) and resulted in an average increase in price of c.8.0%.

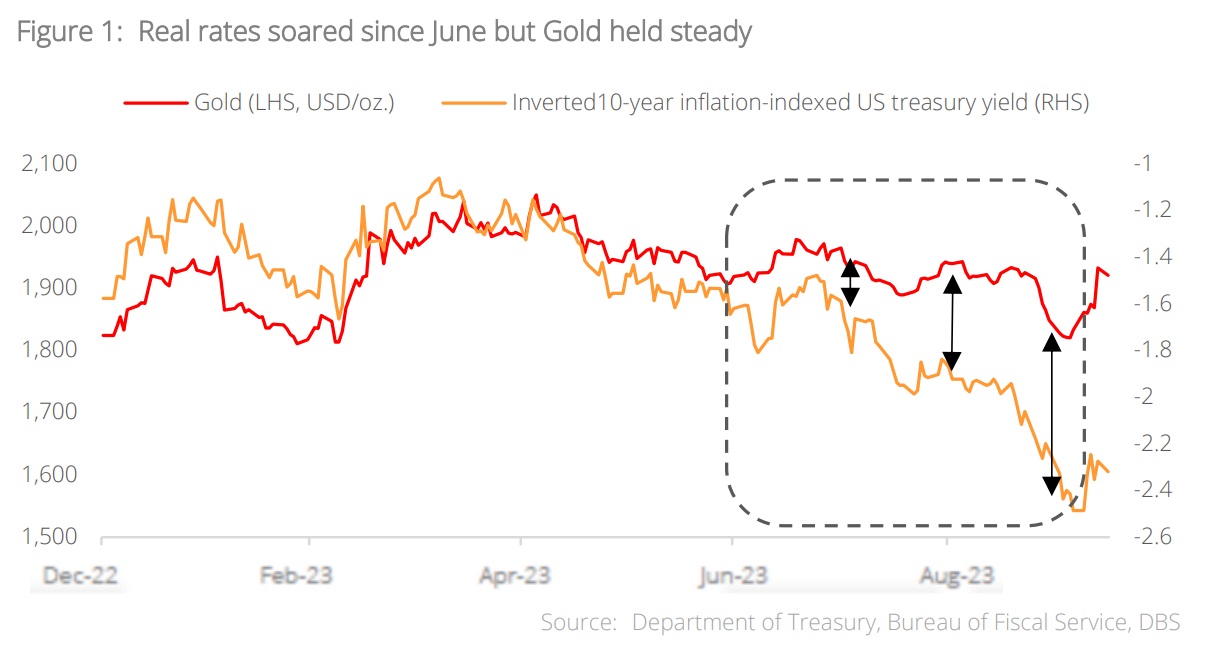

Increasing resilience to real rate rises. Since the start of the Fed’s rate hiking cycle in March last year, interest rates and the dollar have been the primary headwind for gold. This makes sense as treasury yields represent the (risk-free) opportunity cost of holding non-interest-bearing gold. However, this relationship has been somewhat challenged in recent times; the inverse directionality between real rates and gold price remains, but the downside sensitivity of gold price (in response to a rise in rates) has diminished to some extent.

From 1 June to 16 October, the 10Y inflation-indexed US Treasury (GTII10) yield, which is seen as a proxy for real rates, increased 58.8%, while gold receded just 1.5%. Even if we disregard the supportive effect of the Israel-Hamas conflict on gold, the point on reduced downside sensitivity remains valid – between 1 June to 6 October (just before tensions escalated in the Middle East), the GTII10 yield increased 73.6%, while gold fell 7.3%. There are many reasons behind this phenomenon, but a key explanation is that markets are predicting a peak in rates in the near future and positioning themselves for it.

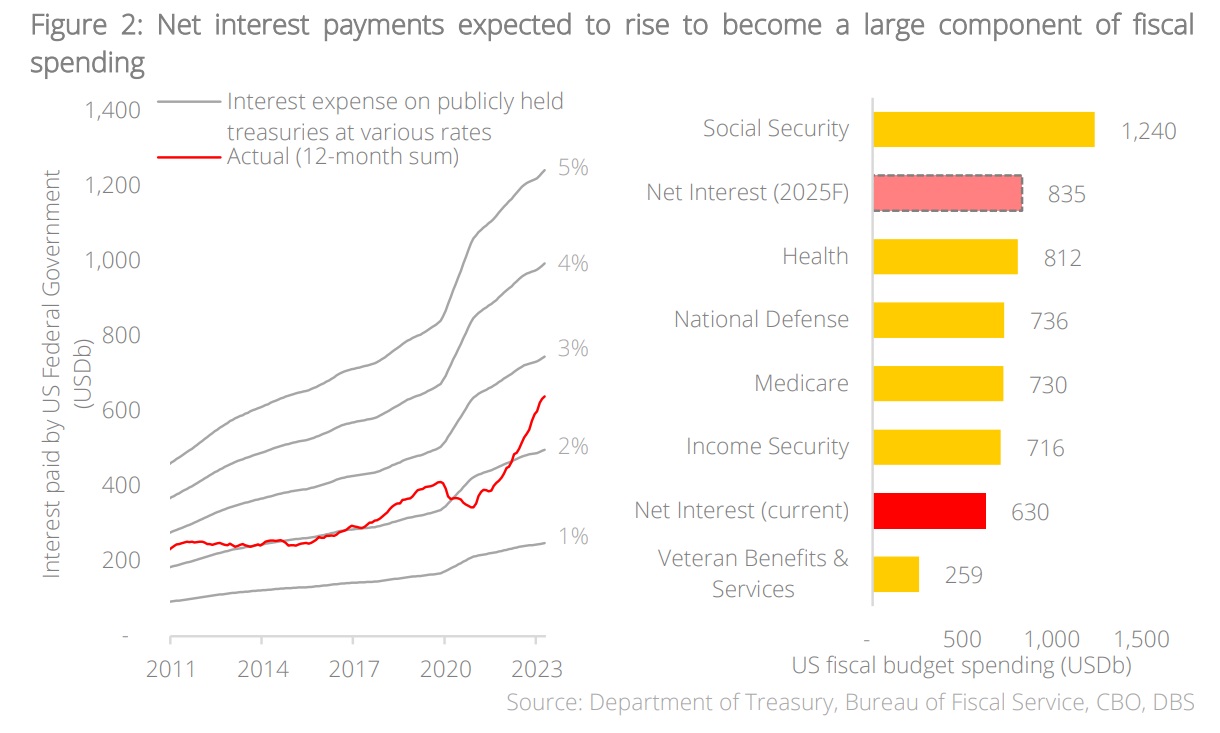

Rates remain a risk but inflection point could be near. With US economic growth staying resilient, labour markets continuing to be tight, and inflation remaining sticky, the Fed is likely to keep the doors open for another hike in November. However, in the larger scheme of things, it appears that the US may soon be at an inflection point where the efficacy of high rates in cooling the economy and bringing about price stability is outweighed by the negative effects of US deficits and indebtedness.

To illustrate how much US indebtedness has ballooned, gross interest payments on US debt have risen c.50% to c.USD970b within a year of the Fed’s first 25 bps hike in in 2022. Net interest payments are projected by the Congressional Budget Office (CBO) to reach USD835b by 2025 (the deadline for the debt ceiling suspension), which ceteris paribus, would make this non-productive area of spending a larger component than other mandatory categories such as National Defense and Medicare.

All this to say that the US will not be able to indiscriminately hike rates much further without running into massive fiscal deficits. We cover in greater detail the implications of higher rates on US interest payments in ‘Credit: How Policy Rates Affects Deficits’ (published on 29 September 2023). The inference for gold is that further rate-driven downside, while possible, is likely to be limited.

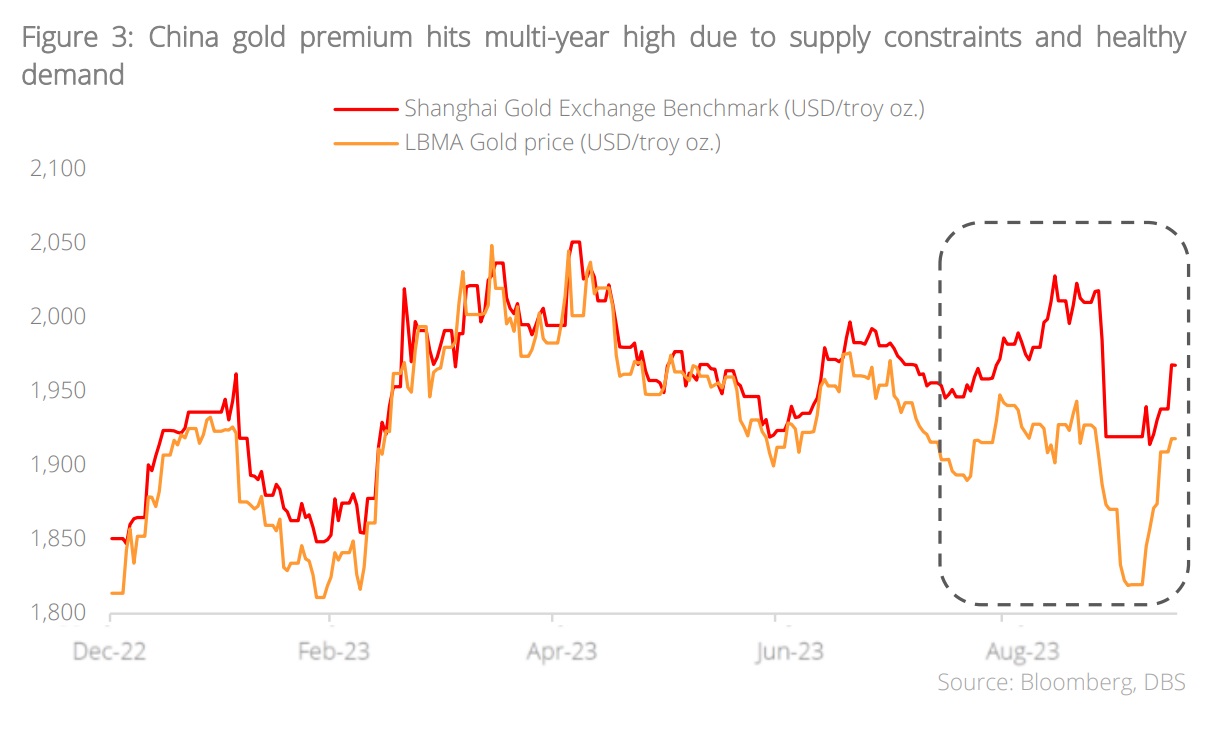

Shanghai Gold Exchange price suggests upside in China market. Another note-worthy development is that Japanese and Chinese investors have been pouring into gold recently, propelling the precious metal to a record high against the JPY. Concurrently, the gold premium in China (as measured by the difference between the Shanghai Gold Exchange price less the COMEX Gold price) has spiked significantly. This growing premium is in large part a reflection of the import curbs that the Chinese government has put on gold recently in a bid to defend the RMB against the backdrop of recent monetary loosening (the People’s Bank of China (PBOC) resumed rate cuts this May for the first time since August 2022). Such elevated gold premiums point at a relatively healthy demand within China.

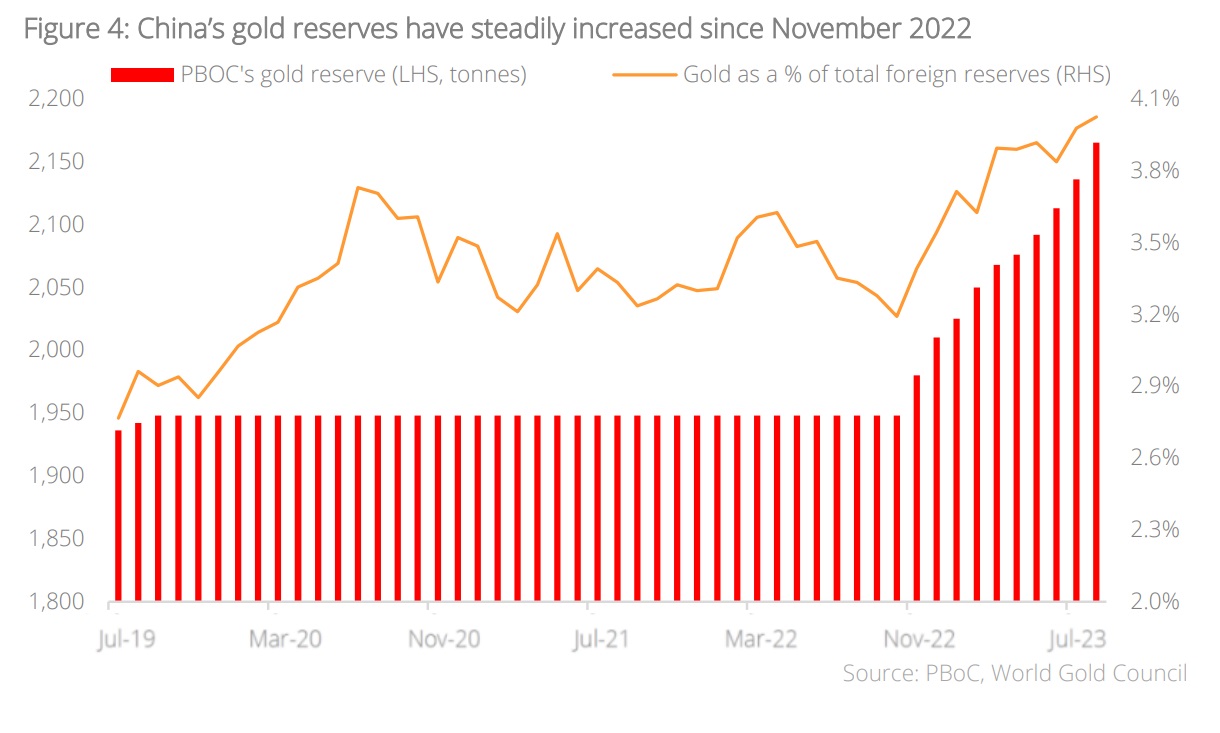

Central bank net buying resumed in August. Additional tailwinds for gold can be found in central banking buying, which turned from net negative in April and May, to net positive in June, July, and August. The largest buyers remained the usual suspects with China, Poland, Turkey, Qatar, Singapore, and Czech Republic rounding out the buyer group for July. In particular, the PBOC has been extremely active in adding to its gold reserves, with its latest purchase of 29 tonnes in August stretching its buying spree to 10 consecutive months and a total purchase amount of 217 tonnes since last November.

We believe this continued strength in central banking buying is part of a wider geopolitical trend that involves countries wanting to diversify their foreign exchange reserves and increase their holdings in neutral hard assets. This long-term trend should prove supportive of gold prices over the long run.

Geopolitical risk, policy rate dynamics and central bank buying provide tailwinds for gold. Higher-for-longer rates remain an immediate concern for gold, however we believe rate-driven downside should be limited as debt sustainability issues will force the Fed to think twice before hiking rates further. Gold has also been displaying a growing downside resilience to rising real rates recently. In the shorter term, the conflict in the Middle east should provide some support for gold around the USD1,900/oz. level, whilst in the longer term, central bank buying on the back of de-dollarisation should prove supportive for the previous metal. We continue to advocate for investors to have holdings in gold as a portfolio risk diversifier and blackswan hedge.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024