- With the world seemingly at the precipice of an economic slowdown, distressed debt funds are readying their arsenal for a slew of opportunities

- Distressed debt investing involves scouring the market for undervalued debt of companies with a high likelihood of default

- Elevated interest rates, tightened lending standards, and rising refinancing risks suggest defaults could be more prevalent especially among weaker borrowers

- A resulting surge in supply of steeply discounted non-performing debt would mean more opportunities from which distressed debt funds can extract value

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Investors in distressed debt do not follow the conventional market psyche. While most investors relish in an environment of optimism, distressed debt funds operate under a different framework. Episodes of strong growth usually mark exit points, while recessions are fertile ground to scavenge for funding gaps that have the potential for huge upside. With the world seemingly at the precipice of an economic slowdown, distressed debt funds are readying their arsenal for what they consider could be a slew of opportunities ahead

What is distressed investing? Distressed investing strategies involve scouring the market to snap up undervalued debt of bankrupt companies, or those with a high likelihood of default. Distressed debt funds review companies’ capital structure for opportunities and purchase underpriced securities with as deep a discount as possible. They then work with other creditors and enhance the securities’ value (e.g., by negotiating bankruptcies to maximise recovery, taking control of an insolvent yet fundamentally sound business, selling assets of the insolvent business, etc.)

A return of distressed opportunities. The pre-pandemic past decade of cheap funding and relatively low default rates resulted in a dearth of opportunities for distressed debt funds. This is set to change, however, as funding pressures and falling asset prices persist. Although the US economy is displaying remarkable resilience despite undergoing one of the most aggressive monetary tightening cycles in recent history, aggregate data overlooks cracks under the surface. Although households and investment grade corporates could be equipped to weather a challenging macro environment, divergence by credit quality is increasing. Elevated interest rates and slowing growth are already weighing heavily on the weakest borrowers – highly-leveraged companies with floating rate capital structures.

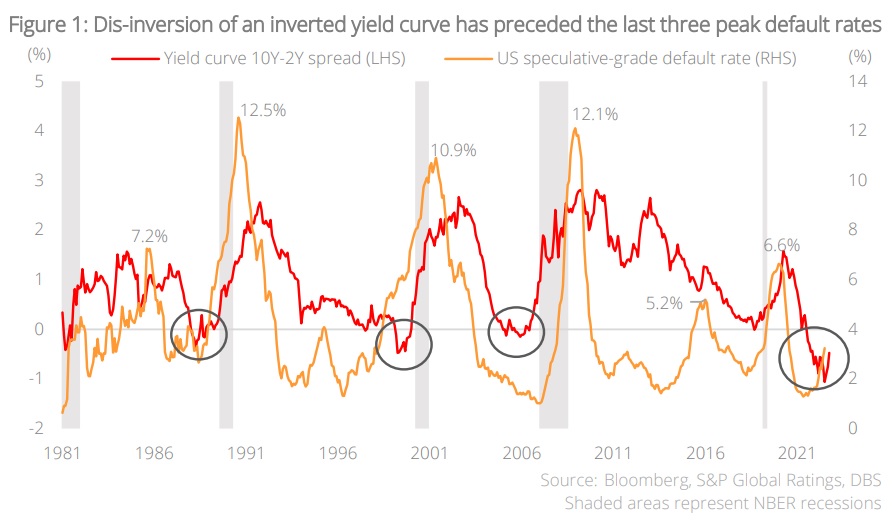

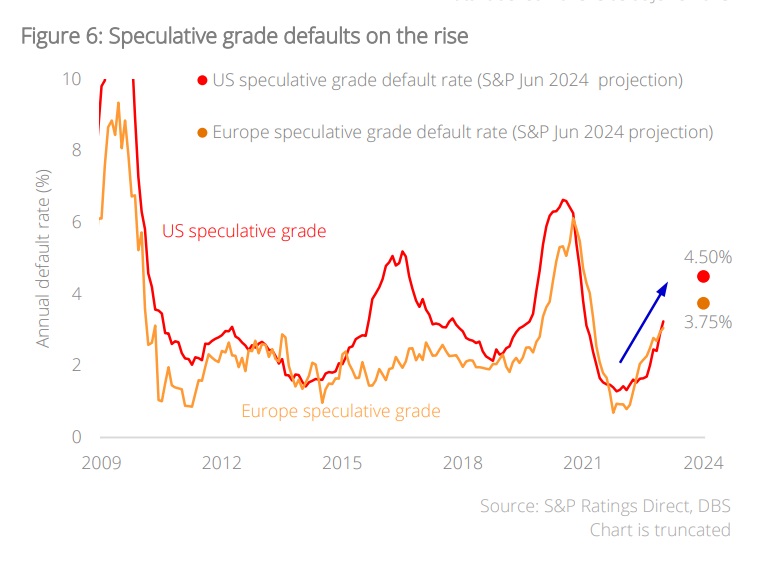

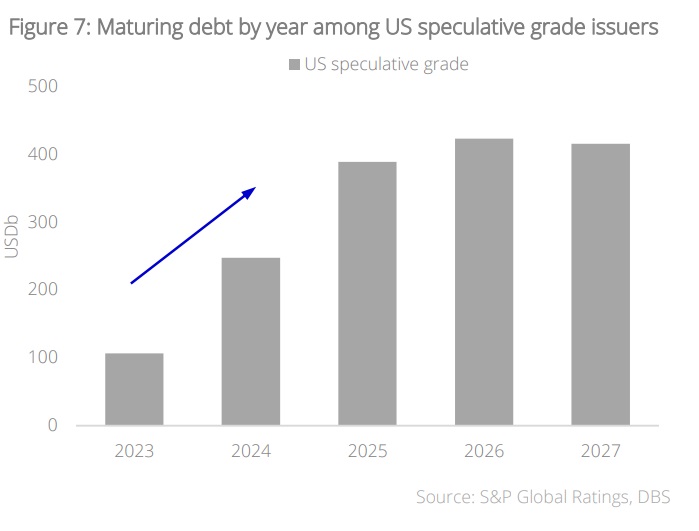

Conditions leading to a rise in distressed opportunities are materialising. For one, recent movements in the treasury yield curve have been sending ominous signals – inversion of the yield curve has historically been a reliable precursor to a US recession, having preceded the past seven recessions by approximately 10 months on average. Furthermore, examining a shorter available history of default data, dis-inversion of an inverted yield curve had foreshadowed the last three peak default cycles in which default rates amongst speculative-grade borrowers reached at least 10% a year. If history is any guide, recent dis-inversion of the deeply inverted yield curve could foreshadow a surge in defaults. The average lead time of inversions across all three prior peaks default cycles was c.34 months, which would place the default rate at c.10% by the second half of 2025, coinciding with a period which sees a spike in speculative grade maturities.

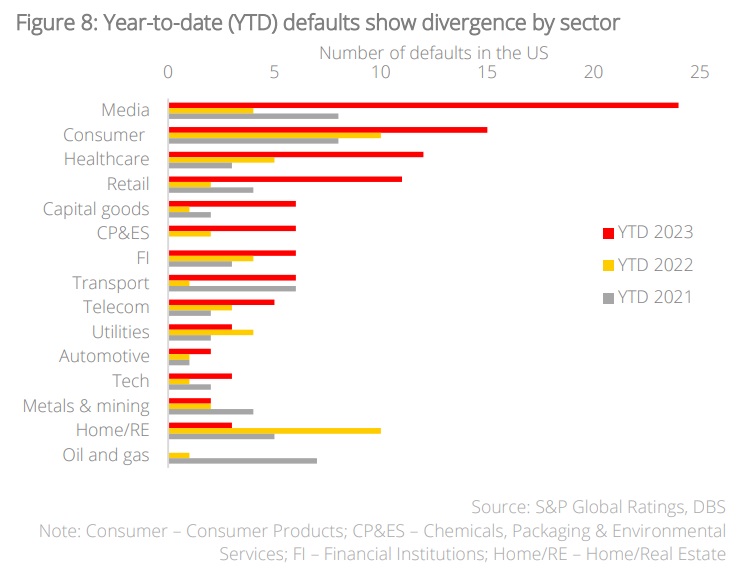

Furthermore, leading indicators of escalating credit stress are apparent, promising an environment with more distressed opportunities, with ratings agency S&P projecting loan defaults to become increasing prevalent in the months to come as companies struggle with elevated rates and refinancing their existing borrowings:

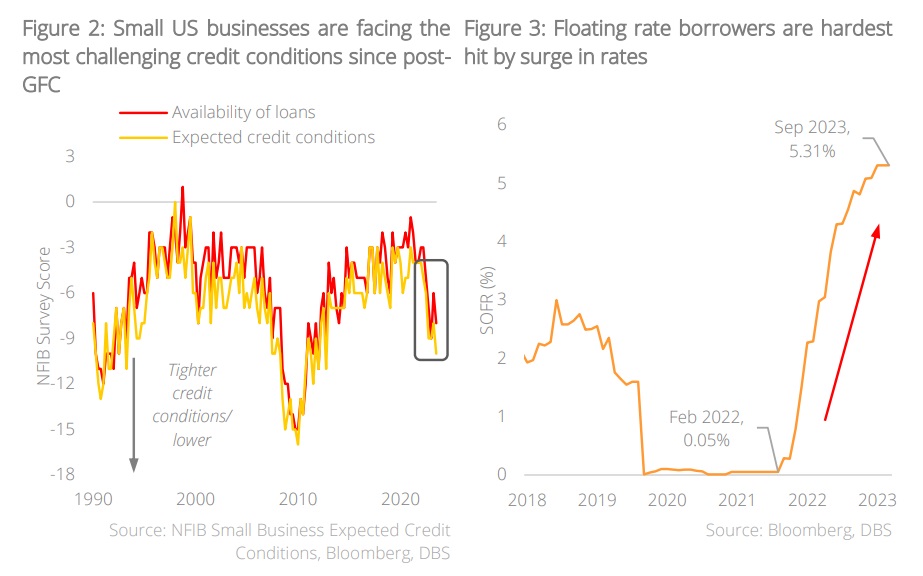

- High interest rates pose a significant challenge, especially for riskier debt – overnight reference rates surged from just 0.05% in February 2022 to more than 5% today. With rates likely to remain higher-for-longer, this adds a significant interest burden for floating-rate borrowers, which already have the weakest credit profiles.

- Banks have begun to curtail lending, especially to riskier borrowers – risk free rates of c.5% offered on default-free government risk present a high hurdle for banks to part with capital. Data from the Fed already shows considerable tightening in bank lending.

- Rising refinancing risks given looming maturity wall by 2024 – nearly USD250b of US speculative-grade borrowers have debt maturing in 2024. These borrowers will face dual headwinds of unwilling lenders and elevated rates. With banks stepping back from lending, this opens a gap for alternative lenders, including distressed debt funds to step in.

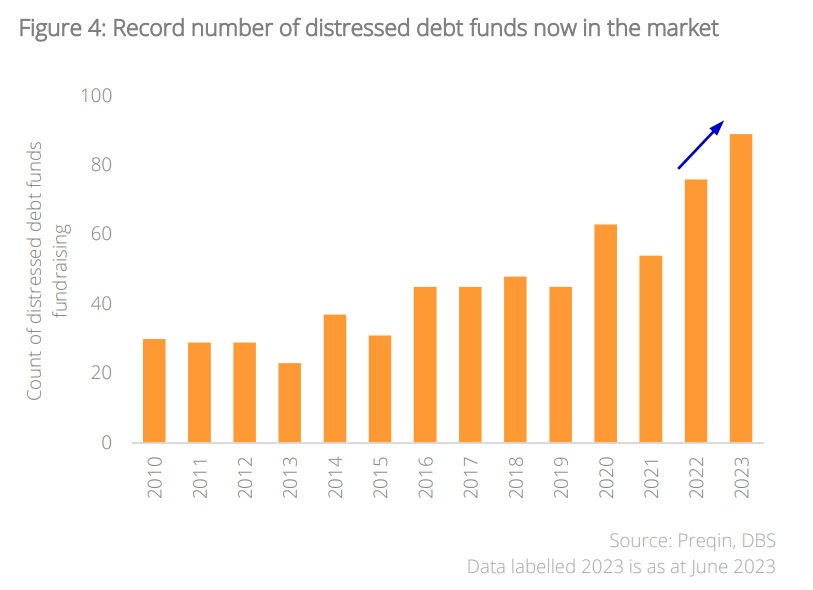

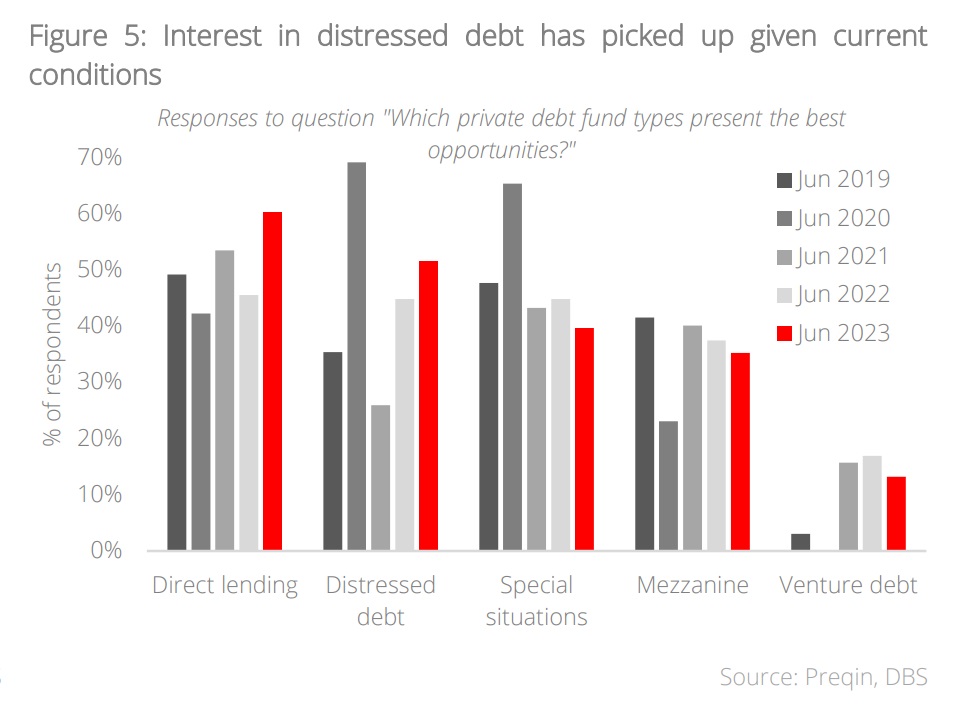

Making the most of a stressful situation. Although the current environment threatens to bring difficulties for businesses that are heavily reliant on borrowings, this would mean a surge in supply of heavily discounted, non-performing debt. Anticipating a fertile hunting ground, distressed managers expect compelling deal flow and have begun preparing to capture such opportunities by gathering dry powder. Accordingly, data provider Preqin notes a record number of distressed debt managers now raising funds – more than 80 distressed funds are raising funds (as at June 2023), a figure higher than at any point in the last decade. Similarly, more investors are also becoming convicted of opportunities in distressed debt, with 49% of respondents in Preqin’s Investors Survey expecting this strategy to be the best performing private credit strategy over the next few months.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024