- Japan’s ongoing domestic transformation, driven by corporate governance reforms, should support market strength in 2H25, alongside gradual policy shifts by the BOJ

- A supplementary budget is likely to be introduced in 2H25 to offset the negative impact from US tariffs and bolster domestic consumption

- Market sentiment will remain highly sensitive to trade negotiations with the US and Upper House election result

- We favour sectors that are domestic-focused, less reliant on exports, and have resilient earnings amid a strengthening yen and higher interest rates

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

After an unsettling April, Japan equities have recovered to pre-“Liberation Day” levels and are expected to regain its upward momentum as concerns over tariff escalation ease. Key domestic drivers, including corporate reform, BOJ interest rate normalisation, and reflation policy measures remain intact. Recent tariff sagas, however, create ambiguity around BOJ policies as global growth remains uncertain. The latest GDP growth also suggests that Japan’s growth continues to stagnate below potential growth. Our conviction call lies in corporate restructuring, which is gaining traction beyond expectations.

Corporate restructuring in Japan gaining momentum

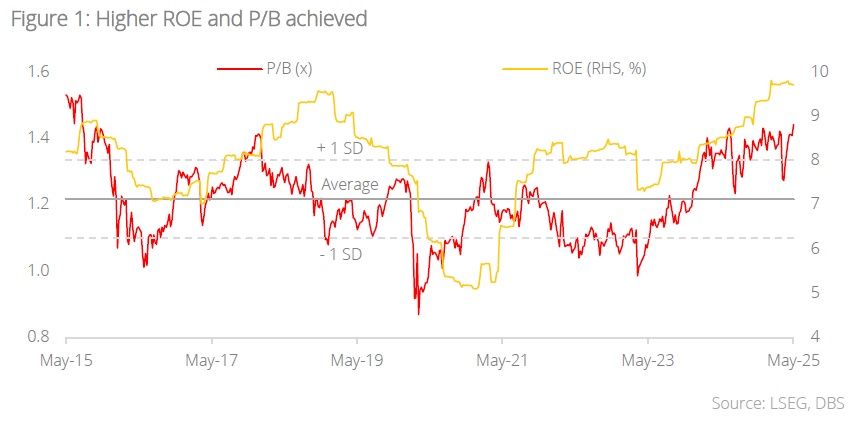

Japan’s corporate landscape is undergoing a fundamental shift with management capabilities and reforms taking centre-stage from a bottom-up perspective. This transformation is evident across both private and public markets, signalling a broader effort to unlock value and enhance corporate governance. Two years into this reform-driven shift, we are seeing tangible results that are reflected in corporate re-ratings and strong TOPIX gains. Japan’s domestic transformation is no longer just a narrative; it is actively reshaping its financial markets and corporate culture.

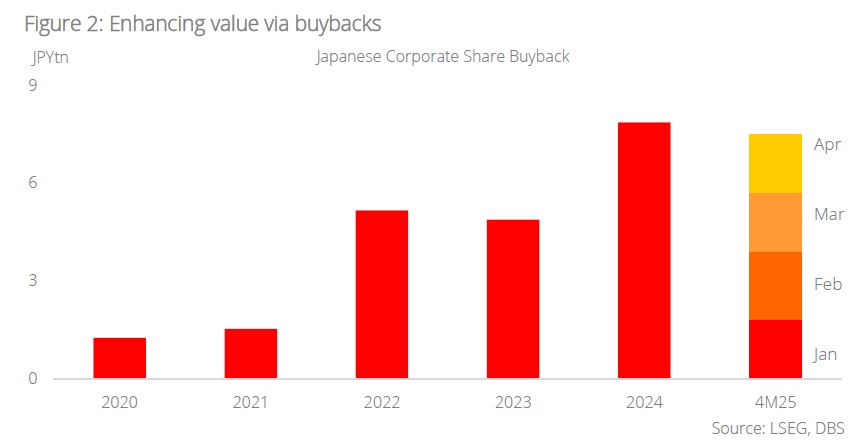

In the public markets, Japanese corporations have emerged as the largest equity buyers, repurchasing JPY7.9tn (USD50bn) worth of domestic stocks in 2024 – a record amount. This surge in buybacks comes as the Tokyo Stock Exchange pressures listed firms to enhance shareholder value and improve capital efficiency. Buybacks continue into this year with the first five months of 2025 exceeding 2024 full-year numbers.

Market sensitivity to trade and political news

Market sentiment remains highly responsive to developments in both trade negotiations and domestic politics, reflecting an environment of elevated uncertainty. We expect this pattern to continue in the near term, particularly around key dates such as election results or major US-Japan trade announcements. Investors should be prepared for short-term volatility with high-beta sectors and cyclicals as the most exposed out of the lot. Conversely, companies with strong balance sheets, high domestic exposure or active shareholder return programs may outperform during periods of uncertainty.

Below, we outline the key dynamics investors should monitor closely, along with our views on likely outcomes and their expected impact.

Political developments: Upper House election

Japan’s Upper House election in July will serve as a referendum on the ruling Liberal Democratic Party (LDP)’s mandate. The outcome has the potential to shape the trajectory of trade policy, fiscal stimulus efforts, and structural reforms. A strong showing by the LDP-led coalition would support continued policy continuity and enable smoother negotiations with the US. Conversely, a weakened position could delay trade agreements and heighten political uncertainty. The election outcome will also influence the timing and scope of fiscal initiatives, including potential supplementary budgets or tax reforms.

Japan-US tariff negotiations

Ongoing trade discussions between Japan and the US will be a central focus in the coming months. Negotiations are aimed at reducing reciprocal tariffs, particularly in the automotive, energy, and agricultural sectors. We expect partial progress by the end of the truce period with average tariffs declining from approximately 24% towards 10%. While concessions on autos and energy are likely, agriculture remains politically sensitive due to domestic opposition, especially from rural constituencies ahead of the Upper House election. A successful outcome could reduce uncertainty and improve investor sentiment, especially for export-oriented manufacturers. However, the absence of a comprehensive deal could prolong sector-specific volatility.

Fiscal policy response and stimulus measures

In response to the tariff environment and potential electoral uncertainty, Japan is likely to introduce a supplementary budget which is modestly larger than recent years in the second half of 2025. This is aimed at offsetting the economic drag from US tariffs and supporting domestic consumption. While proposals to temporarily cut the consumption tax to 5% are gaining political traction, such a move remains contentious amid rising Japanese Government Bonds (JGB) yields and mounting concerns over fiscal sustainability. Should the LDP suffer electoral setbacks, debates over tax cuts and the pacing of fiscal consolidation would likely intensify.

Monetary policy and BOJ normalisation

The BOJ’s next policy meetings in June and July are likely to stand pat on interest rate normalisation and may temporarily intervene – particularly through purchases of super long-term JGBs – if yields in the 30- to 40-year segment rise sharply. A more decisive policy shift could benefit financials, while rapid changes may introduce market instability.

JGB yield curve and long-term interest rates

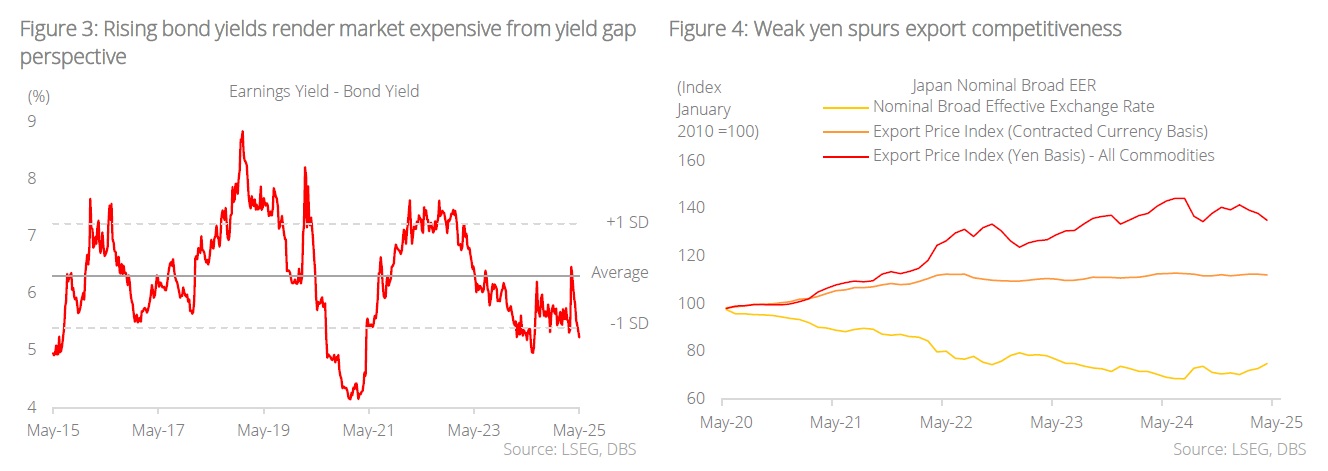

For the first time in over a decade, Japan’s yield curve is displaying a meaningful steepness, driven by rising long-term JGB yields. This development reflects both the BOJ’s policy shift and improving inflation dynamics. While steeper curves enhance bank profitability and may encourage a return of domestic institutional capital to the JGB market, they also raise concerns about fiscal sustainability – particularly for long-duration public debt. We expect the BOJ to proceed cautiously with quantitative tightening continuing, though it would be balanced by tactical long-end purchases if market conditions warrant intervention.

the JPY’s excessive weakness, Japan is unlikely to intervene if the JPY appreciates.

Should USD/JPY continue to trend lower, the pressure on corporate earnings – particularly in the automotive and technology sectors – could intensify.

Implications and strategy for Japan equities

Despite being surrounded by macro uncertainties, Japan’s ongoing domestic transformation, driven by corporate governance reforms, is expected to sustain market strength into the second half, alongside economic policy shifts (e.g. BOJ policy shifts) and structural improvements (e.g. TSE corporate governance policies). This period will further underscore the resilience of Japanese companies as management teams continue to execute reforms and adapt to evolving economic conditions, reinforcing a strong bottom-up growth story. Corporate restructuring beneficiaries are likely to be prevalent in big caps with non-core businesses and cross-holding structures (where value can be unlocked) and small mid-cap companies which could be subject to delisting if they fail to meet continued listing criteria.

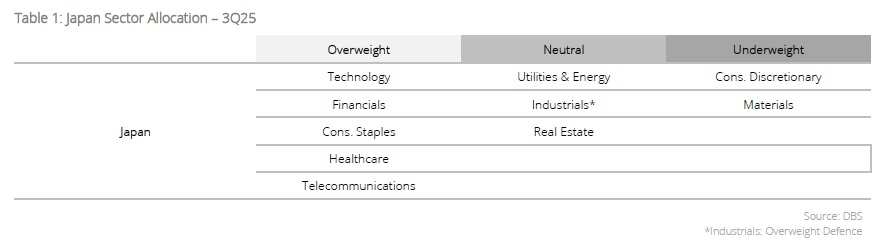

Japan Sector Allocation - 3Q25

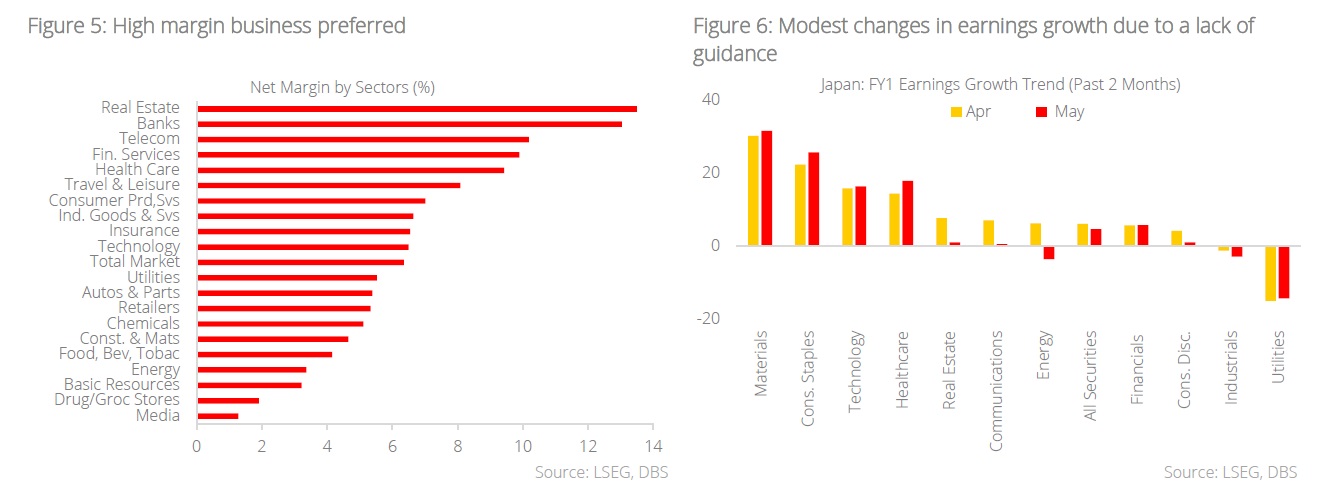

Our preference for sectors is analysed around earnings resilience amid a strengthening yen, higher US tariffs, and higher interest rates. High margin businesses should provide more cushion for rising costs.

The best positioned sectors are those that are domestic-focused, less reliant on exports, and capable of passing costs onto customers. Investors should favour these areas for stability and growth potential in uncertain external environments.

Most positive sectors under this environment:

- Consumer staples retailing such as drugstores and supermarkets with strong domestic demand, margin improvement potential, and market share gains

- Pharmaceuticals and medical devices where demand is inelastic and are, thus, less affected by tariffs or currency fluctuations

- Banks and insurance benefit from rising interest rates and steady profit growth; banks are undervalued, while insurance is less exposed to trade risks

- Rising demand for electricity and gas is driven by domestic consumption and infrastructure projects such as data centres and semiconductor plants

- Domestic-focused technology and services such as software and IT services where domestic market is strongly driven by digital transformation and margins improvement via offshoring; internet and digital media companies where growth is driven by local user engagement, advertising, and digital services—these activities are less impacted by tariffs or currency

- Industrial sectors such as the defence and aerospace industry benefit from government contracts and are less vulnerable to trade and currency fluctuations

Conversely, the worst positioned sectors in such an environment are primarily those with significant export exposure, high capital expenditure needs, low margins, and are highly sensitive to cost increases and currency fluctuations with reliance on international trade and supply chains. Their margins and growth prospects are at risk from (i) tariffs which increase costs and disrupt supply chains, (ii) strong yen which erodes competitiveness and reduces foreign earnings, and (iii) rising interest rates which raise financing costs and potentially slow investment and demand.

These include:

- Export-dependent manufacturing and capital goods such as machinery, plant engineering, and shipbuilding. They are sensitive to tariffs and yen appreciation which increase costs and reduce international competitiveness. Higher interest rates can raise financing costs for large projects and investments

- Steel and metals which are export-oriented sectors heavily impacted by yen strength and tariffs which can erode margins

- Semiconductor equipment and electronics exporters have strong fundamentals, though there are sector risks which include export restrictions (e.g. China) and potential demand slowdown from tariffs and geopolitical tensions. Yen appreciation could also pressure international competitiveness

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025