- Three key themes will dominate 3Q25: pragmatic de-escalation of tariff tensions, divergent equity performance, and fiscal headwinds which are negative for government bonds and the dollar but positive for gold.

- Gold's traditional inverse relationship with bond yields has broken down since "Liberation Day", reflecting new dynamics around fiscal sustainability and de-dollarisation.

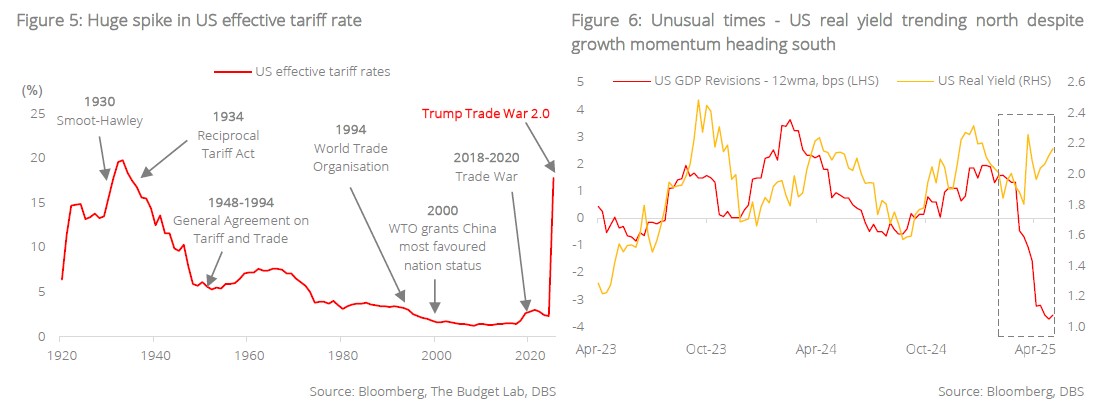

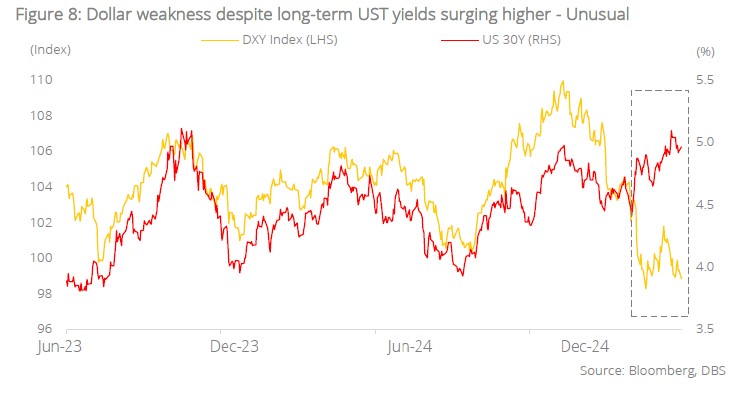

- Despite tariff tension clouding the macroeconomic outlook, long-term Treasury yields have broken out decisively with the 30Y yield breaching the 5% mark.

- Dollar weakness of -9.7% YTD despite surging Treasury yields reflects growing reservations about the greenback's reserve currency status.

- US fiscal profligacy and policy ambiguity are increasing risk premiums across financial assets. While pragmatism will likely underpin tariff de-escalation, expect significant divergence in equity performance with technology and services outperforming.

lot has happened in Trump’s first 100 days. From aggressive cost cuts at the Department of Government Efficiency (DOGE) to the unleashing of a global tariff war, his shock and awe approach has remade America with far-reaching consequences. Rhetoric from the Trump administration suggests policy ambiguity will be an ongoing feature for the next four years, and this means rising risk premium for US financial assets and, certainly, a greater need for agility in investors’ portfolio positioning.

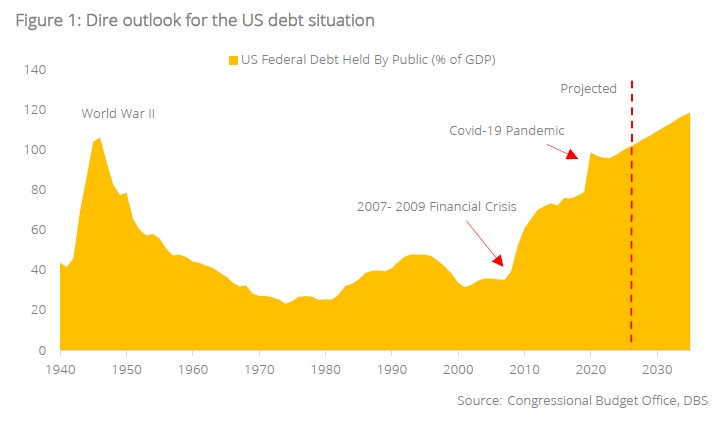

The recent passage of Trump’s expansive tax reform through congress added another layer of complexity for financial markets as investors begin to question the sustainability of the US’ enormous debt load. Based on projections by the CBO, the US budget deficit is expected to hit USD1.9tn this year, and by 2035, federal debt will constitute 118% of GDP. These dire projections tie in with Moody’s downgrade of the US credit rating to Aa1 – a symbolic move which heralds a new era where US Treasuries are no longer “risk-free”.

Despite tariff tension clouding the macroeconomic outlook, long-term Treasury yields have broken out decisively with the 30Y yield breaching the 5% mark. The unusual occurrence marks rising unease over US fiscal sustainability and the additional risk premium required for investors to hold long-duration assets. The surge in Treasury yields coincided with similar moves for JGBs, with the 30Y yield hitting 3%.

But while the moves were similar, there is one crucial difference. In Japan, public debt is financed predominantly by domestic savings. In the case of the US, public debt is funded heavily by foreign capital and, today, foreign investors account for 33% of Treasury bonds and 18% of US equities (as of Jun 2024). Such heavy reliance on foreign funding can turn precarious as Trump continues to pursue his “America First” agenda.

Uncle Sam wants your money. The US’ failure to meet its obligations through taxation and cost cuts only reinforces the view that Trump’s so-called beautiful tariff war is not only about reshaping the world order through strategic containment of China and “Making America Great Again” by bringing manufacturing jobs home; it is also about raising revenue to address America’s insolvency issue which underpins the ideological rationale of implementing a “universal tariff” on both friends and foes alike.

If this train of thought runs true, then one can only conclude that Trump’s tariffs are here to stay with substantial impact on global inflation and growth outlook. According to the Tax Foundation, universal tariffs of 10%-15% will reduce GDP growth by 0.4%- 0.6% as economic output contracts on the back of higher import costs and supply chain disruption. Based on a separate study by the Budget Lab at Yale, the tariffs are also expected to push consumer prices higher by 1.7% as businesses pass on the higher input costs to end-consumers.

A solution for a bygone era. Unlike the 18th and 19th centuries, when tariffs functioned as an important source of government revenue, the situation today is vastly different given the gargantuan size of the US fiscal deficit. Even if one assumes an aggressive 20% universal tariff, the Tax Foundation expects only an additional “conventional” revenue of USD297.1bn for 2025. Should one factor in the “dynamic effects” of tariffs coupled with potential foreign retaliation, the additional revenue will shrink further to USD185.2bn – a sum barely sufficient to offset the interest payments for US debt obligations.

Trump’s so-called beautiful tariff war is therefore no panacea for US fiscal profligacy which will only get worse as the administration pushes ahead with tax cuts in the “One Big Beautiful Bill”. Concerns over the government’s ability to fund its deficit have not only pushed long-term yields higher, but also sent the dollar lower (with DXY index poised to hit 92.5 by the end of 2026). The dynamics driving equities were, however, different as markets rebounded close to re-“Liberation Day”, levels riding on the positives of tariff de-escalation and tax cuts.

As we approach the second half, we believe that the following topics will dominate the narrative and determine the trajectory of markets:

- Pragmatism and the de-escalation of tariff tension

- Divergence and polarisation in equity performance

- Fiscal headwinds negative for government bonds and the dollar, positive for gold

Tariffs: De-escalation, but Not Elimination

“When the facts change, I change my mind”. The words of John Maynard Keynes couldn’t be more timely in today’s geopolitical landscape. Abrupt US-China de-escalation has taken markets by surprise and the decision is underpinned no less by pragmatism. A tariff of 145% is essentially a trade embargo that will hurt both parties. Above all, the acute surge in bond yields is another crucial factor that has taken the Trump administration by surprise and is causing a re-think in its strategic agenda.

US Debt-to-GDP currently stands at 124% and USD7.8tn of outstanding debt requires refinancing this year, followed by USD3.7tn in 2026. The blended average interest cost currently stands at 3.35% and this is markedly lower than prevailing 2Y, 10Y, and 30Y bond yields. Today, interest payment accounts for c.11.9% of US total expenditure, and given the dire US fiscal situation, the country can ill-afford to incur additional interest expense especially at a time when it is extending previous tax cuts.

China is not doing much better either. Manufacturing activities are starting to moderate while the government’s efforts in boosting domestic consumption has remained futile in the land of savers. In the US, inflation is poised to surge as both Chinese exporters and US importers have showed little appetite to “eat the tariffs” as Trump has suggested, and this could only mean one thing: Higher prices for US consumers.

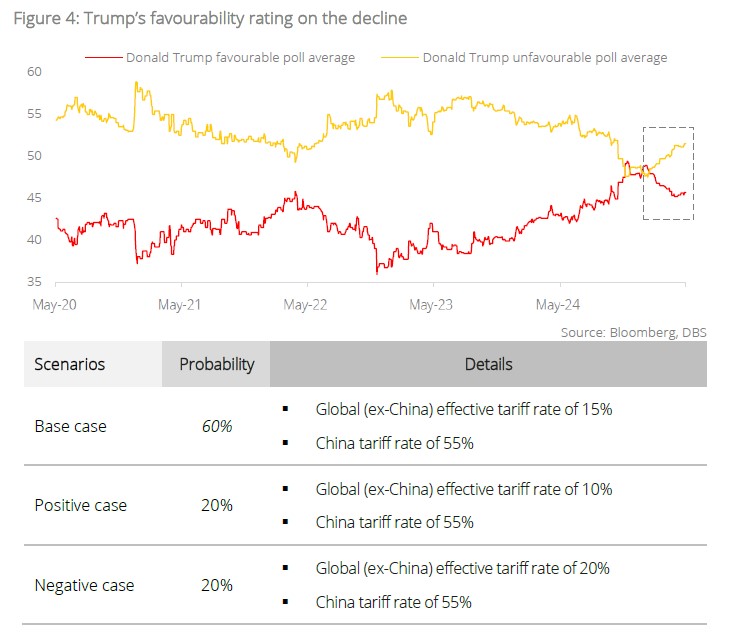

Pragmatism rules. Slower growth and rising inflationary pressure will be a disaster for Trump at a time when he is facing waning poll numbers at home. The surprising embrace of policies belonging to the progressive left (such as tax increase for top earners) underlines Trump’s effort in revving his popularity before the 2026 midterms and to reframe the Republicans as a party for the working class. This probably explains the eagerness to taper trade tension with China, avoiding the economic fallout of a full-blown trade war.

What happens after 90 days? Using the first Trump presidency as a guide, our base-case scenario is further de-escalation with China, agreeing to make substantial purchases and potentially striking a fentanyl deal with the US. Should this transpire, the tail risks for markets will be reduced significantly with low likelihood of a recession. While uncertainties remain, we believe investors will see the glass as “half full” and focus on the positives of trade de- escalation.

Following the mid-June trade talks in London, President Trump has announced US tariffs on China would be set at 55% while Chinese tariffs on US goods would remain at 10%. Such substantial de-escalation will put a floor to equity markets as investors await corporate guidance on how the 10% universal tariff and 55% China tariff will impact corporate earnings in the coming quarters. But given that equity markets have already rebounded back to pre-“Liberation Day” levels (as a result of light positioning), much of the upside is captured in current prices. For markets to grind higher from here, corporate earnings need to strengthen further as valuations are looking stretched by historical standards.

Equities: Divergence and Polarisation

Our assumption of further de-escalation in the tariff war means that the probability of a recession has diminished sharply and this is comforting news for global equities. But avoiding the worst-case scenario does not mean that no damage is done. The uncertainties and chaos brought on by the Trump administration has dampened business confidence and the lack of visibility means that CEOs will hold off corporate capex until the fog clears. The same applies to consumers. Big-ticket purchases will be postponed until further clarity emerges on how the universal tariffs will impact the future cost of living.

Under such conditions, we expect earnings downgrades to take place across sectors, particularly amongst global cyclicals. Based on consensus forecasts, the street is still expecting 11% EPS growth for S&P 500 this year, a level which does not reflect prevailing macro uncertainties. US industries that are most exposed to tariff tensions with China (such as automobiles and agriculture) will encounter the sharpest downward earnings revisions.

This is unfortunately coming at a time when longer-term bond yields are edging higher as US fiscal concerns have compelled investors to start questioning US Treasuries’ “risk-free” status. Under normal circumstances, rising bond yields reflect economic strength. But not this time round, as US real yield is trending north just as GDP momentum is heading south.

But despite these headwinds, why are we Neutral and not outright bearish on equities? There are three mitigating factors at play:

- The “shock and awe” antics aside, it is also evident that the Trump administration’s policy approach is overlaid with pragmatism. This is evident from its abrupt U-turn when bond yields were spiralling higher at the peak of the tariff war. With the mid-term on the horizon in 2026, we believe that tariff tensions with China will eventually be resolved, and the avoidance of a recession warrants a Neutral call for equities.

- AI investments remain a significant tailwind for both economic growth and financial markets. Alphabet, Microsoft, and Amazon, for instance, will be investing a combined USD250bn in 2025 on AI-related infrastructure while on the sovereign front, the Middle East is pumping in c.USD100bn in AI-driven investments over this decade.

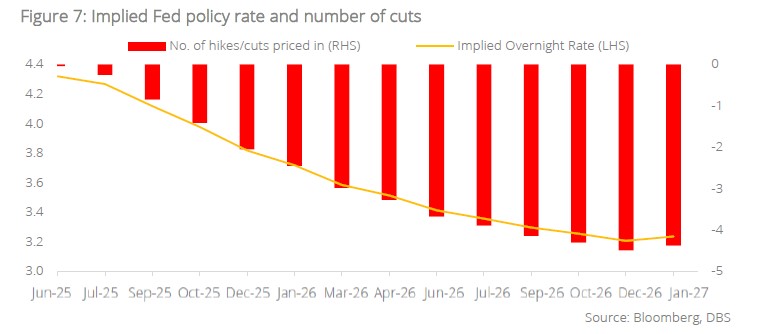

- Tariffs are inflationary and this dampens the Fed’s enthusiasm for cutting rates as the central bank monitors hard data releases to assess the impact on consumer prices. But consensus forecasts suggest that the Fed will nonetheless commence its rate cutting cycle in 4Q as growth starts to moderate and this is a tailwind for equity markets.

In such an environment, we see divergence in performance across the equity space. Industries focusing on services will be more resilient relative to those focusing on goods. Within the US technology sector, a clear case in point is the divergence in performance between Microsoft (MSFT US) and Apple (AAPL US). Microsoft’s focus on cloud services is less directly impacted by tariffs, unlike Apple’s consumer tech business where headwinds are on the rise with Trump insisting that iPhones sold in the US must be manufactured domestically.

Conviction Calls – Bullish Gold; Bearish Dollar

Historically, given the non-yielding nature of gold, the precious metal possesses an inverse relationship with bond yields. Indeed, gold and the 30Y nominal yield exhibited a correlation of -0.22 during 2004- 2024. But this inverse relationship has clearly broken down since Trump’s “Liberation Day”, as concerns about tariffs, coupled with US fiscal sustainability and de-dollarisation, have taken centre stage.

Data from the World Gold Council shows central banks’ demand for gold has been on the rise, hitting 1,045 tonnes in 2024 (121% higher than the long- term average for 2010-2021). The latest projection from the CBO on US’ long-term debt outlook suggests that this trend will persist as central banks incrementally diversify and reduce their exposure to US financial assets in the face of geopolitical and fiscal sustainability concerns.

An offshoot of US fiscal profligacy is dollar weakness. The greenback has weakened 9.7% despite long term US Treasury yields surging higher this year. This is an unusual occurrence which suggests rising reservations about the greenback as the anchor reserve currency of the world. The dollar weakness, meanwhile, also ties in with Trump’s Mar-a-Lago strategy, as a strong dollar was often blamed for the US’ loss of export competitiveness and the hollowing out of its industrial base.

We expect dollar weakness to persist with the US Dollar Index (DXY) hitting 97.8 by 4Q25.

3Q25 Asset Allocation – Defensive Shift

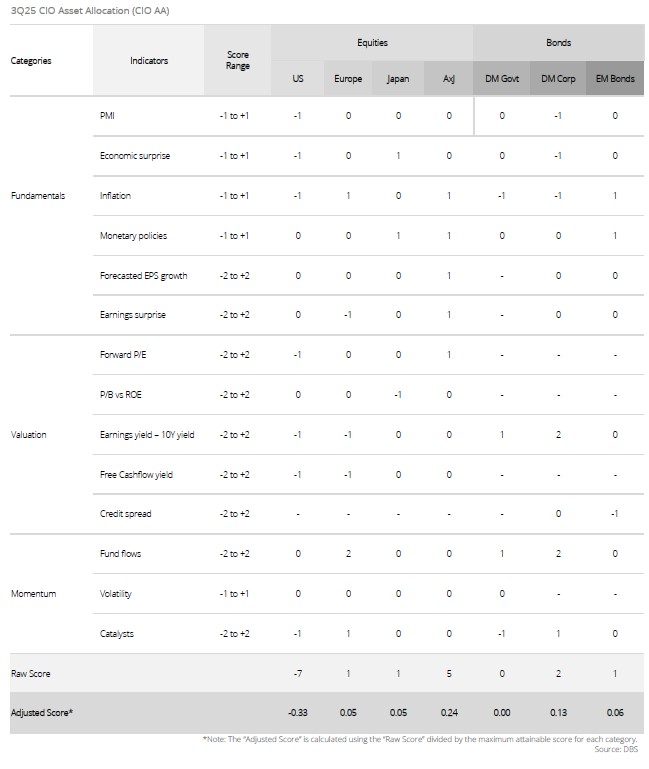

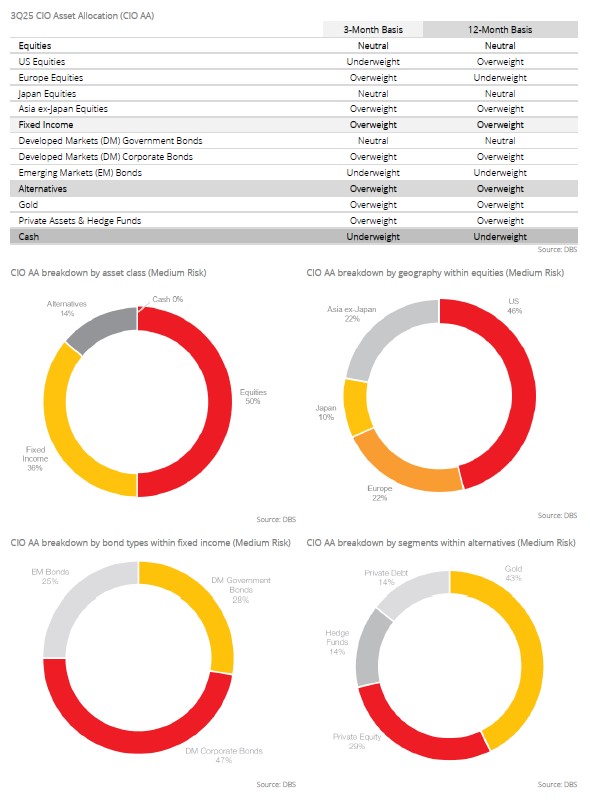

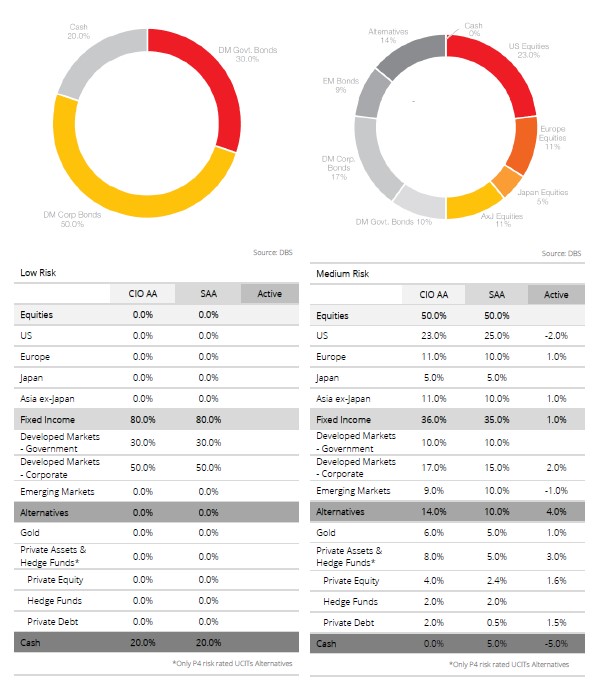

Cross Assets – Bonds remain in play. The latest scoring on our CAA framework suggests a preference for bonds over equities in the VUCA era.

Fundamentals: US manufacturing momentum has moderated since the start of the year, while economic surprise is not looking too upbeat either as the strain of trade war uncertainties gradually erodes business confidence and deters corporate capex. A slowdown in growth momentum, however, is paradoxically met with upward inflation risks amid potential supply chains disruptions, labour market tightness, and rising money supply growth. Companies are already reporting sharp increases in input costs and the situation will get worse should China/Europe fail to cut a trade deal with the US.

On corporate earnings, US earnings forecast has been revised down but the change is marginal and this suggests analysts’ assumption of further de- escalation in trade tension. A similar downtrend in earnings revision is evident in Europe and Japan, and the only market that managed to buck the trend is Asia ex-Japan. For FY2025, the region is expected to register earnings growth of 12.4% (vs 6.6% for DMs).

Valuation: The gap between US earnings yield and the UST 10Y yield has deteriorated to -0.4% (as of 30 May) and this reinforces our cautious stance on equities relative to bonds.

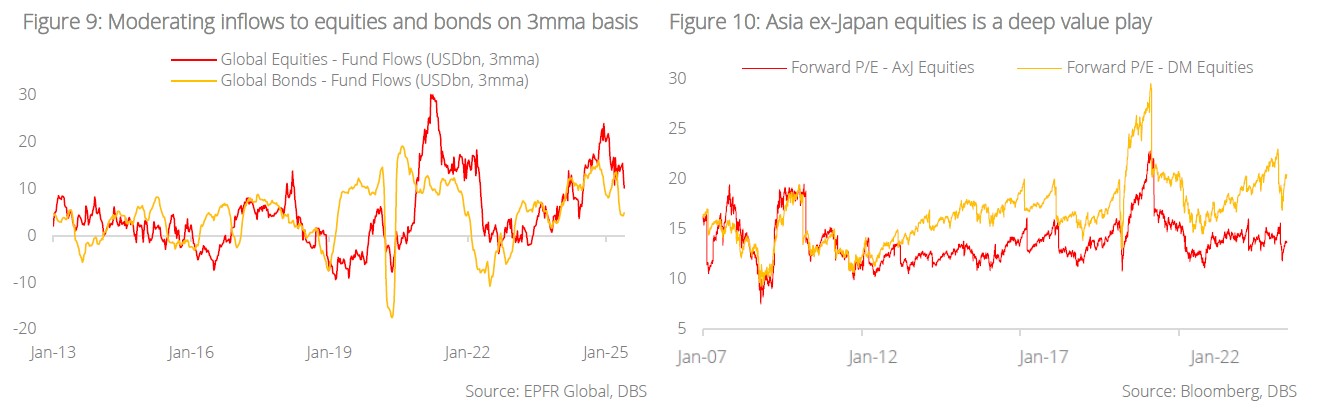

Momentum: While bond funds continue to register inflows, the momentum for equity funds appeared to have waned as the latter registered outflows of USD213.6bn in the past two weeks (as of 28 May), compared to inflows of USD44.3bn for bonds. This reflects a broad-based shift to defensive positioning as concerns on tariff uncertainties took hold. Expect this trend to persist as the deadline for trade negotiations between the US and China/Europe looms.

Equities: Maintain conviction call on US Technology; Nvidia’s strong guidance reinforces resilience of AI theme. Given prevailing tariff uncertainties, making country allocation calls in 3Q25 will be a challenge as things could swing either way, much depends on whether the country/ region can cut a deal with the Trump administration by July. Judging from recent market movements, a “favourable” trade deal will mean an indiscriminate rally in risk assets while a re-escalation will lead to the resumption of market sell-offs – binary outcomes.

We maintain our base-case assumption of pragmatism to prevail in the negotiations, with both China and Europe reaching respective trade deals with the US. And should trade relationships return to pre-“Liberation Day” normalcy, we expect the previous dynamics driving equity markets to take hold. Within DMs, we maintain a slight Underweight on US equities and our cautious stance is premised on:

- Consensus earnings forecast for US remains overly optimistic at 11% despite recent downward revisions (vs 7% for DMs). We expect more progressive earnings cuts in the coming months as the impact of tariff uncertainties (and consequentially, a decline in business confidence) is factored into the business outlook.

- Dollar weakness, coupled with the prevalence of policy uncertainties (tariffs and Section 899) will compel portfolio allocators to lighten their exposure to US financial assets and diversify to other DMs.

But the above headwinds, however, are mitigated by the continuation of strong momentum in the technology space (notably, the AI segment). As evidenced by Nvidia’s results, the growth trajectory for AI remains robust and this augers well for the outlook of the entire US tech ecosystem. We expect weakness in US non-tech sectors to be partially offset by resilience in the tech space.

Maintain Overweight on Europe. Prevailing concerns on US fiscal sustainability and policy uncertainties provide tailwinds for Europe equities as global portfolio allocators reduce their US exposure. Above all, resurgent fiscal impulse in Europe will drive macro growth momentum for the region in the coming years as European countries start to increase their defence spending. Earnings expectations in Europe remain low and this provides room for upside surprises.

Trading at a 33% discount to DMs, Asia ex-Japan is a deep value play. The region’s valuation merits provide a margin of safety for investors particularly when the economic cycle is starting to turn. China remains massively under-owned by institutional investors and the resurgent domestic tech industry (in the wake of DeepSeek) provides ample opportunities for stock pickers. Stay Overweight.

Bonds: Fiscal sustainability and inflation concerns to drive long-term yields higher; maintain duration barbell approach. While tariff tension remains, the market’s attention has since shifted to fiscal sustainability as long-term yields drifted higher on growing demand-supply imbalances. Besides, the recent spikes in long-duration Treasuries and JGB yields also reflect sticky inflation that are not likely to subside anytime soon in the face of tariff uncertainties, labour market tightness, and money supply growth. Backward looking data may present a picture of calm on the inflation outlook but we advise against complacency and this underpins our downgrade of DM government bonds to 3-month and 12-month Neutral. Higher long-term yields and further curve steepening are on the cards in the medium term.

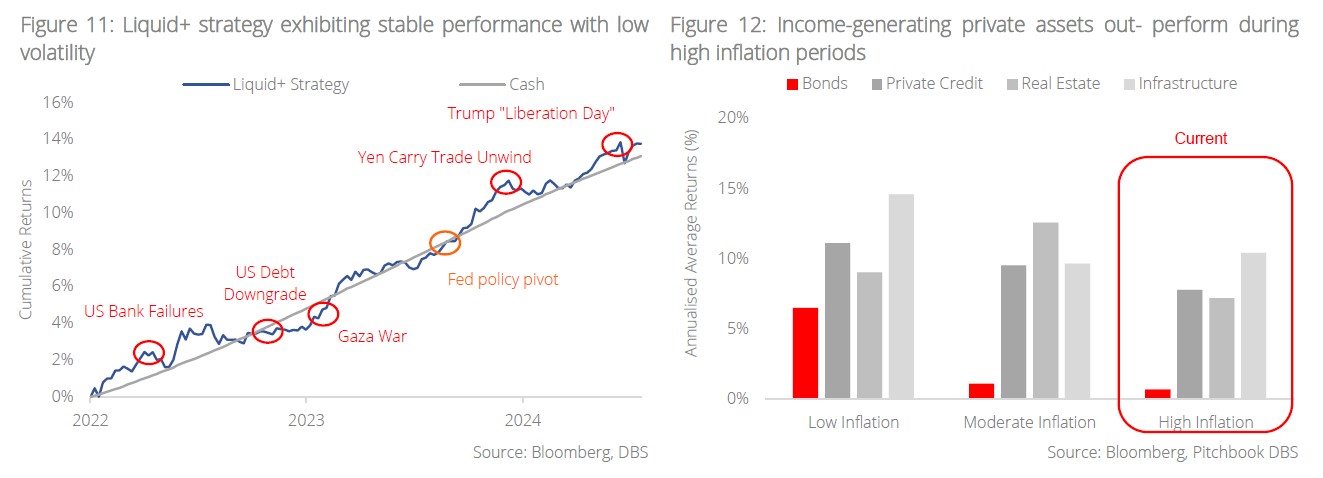

In the credit space, we advise investors to stay with quality in the A/BBB bucket and adopt a duration barbell approach with exposure to the 2-3Y and 7-10Y IG credit. Our 2-3Y Liquid+ strategy has exhibited stable performance with low volatility despite significant market risks in recent years and it is well-positioned to navigate stagflationary conditions should the latter transpire. We are, however, less convinced on the HY segment given higher risks of spreads widening and we advise investors to stay in quality in the BB bucket.

Alternatives: Overweight gold with target price of USD3,765/oz. by 4Q25; seek opportunities in income generating private assets. of central banks and investors’ demand in the face of these headwinds are key to driving up the price of gold given the precious metal’s appeal as an effective diversifier. We expect gold to hit USD3,765/oz. by 4Q25 and this connotes another c.14% upside from current level (as of 30 May). Maintain Overweight.

In private assets, our strategist opines that a portfolio of open-ended semi-liquid and hedge funds will gain traction among investors looking to increase exposure to alternatives. The ability to calibrate a portfolio’s liquidity profile allows investors to navigate market volatility in the VUCA era. With tariff uncertainties posing downside risks to inflation, it makes sense for portfolios to gain sufficient exposure to higher yielders, for instance. Our analysis suggests that income generating private assets like private credit, infrastructure, and real estate displayed greater resilience over bonds during inflationary periods.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.