- Trade tariff disruption surfacing, with global OEMs expecting earnings hits

- US tariff uncertainty an overhang; global automakers with exposure to the US market could be hit

- Long-term shift to US manufacturing slow; global automakers face complex strategic adjustment

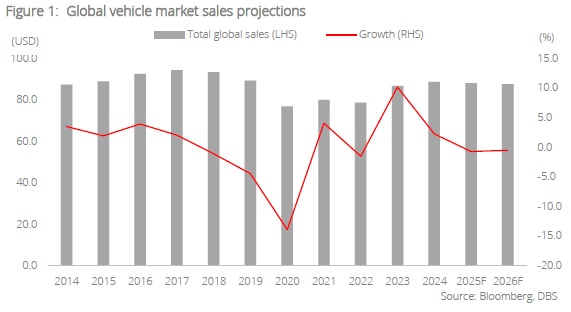

- Global vehicle sales expected to contract by 1% in both 2025-2026; remain cautious on the sector

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Global automotive value chain faces disruption; production outlook downgraded. The global automotive industry is beginning to feel the strain from the recently announced US trade tariffs, with several global automakers anticipating demand to soften ahead amid potential negative impacts on their earnings during the recent results briefings, including Ford (by USD1.5bn) and General Motors (of USD4-5bn). In response, S&P Global Mobility has revised its global vehicle production outlook, now projecting 7%/5% volume declines in Europe and North America, respectively.

This is already reflected in the data with new car registrations in the EU falling 1.2% y/y (4M25), attributable to the ongoing unpredictable global economic environment. In contrast, the US auto market remained resilient since the tariff announcements in March with volume shipment up 3.2% y/y in April as consumers rushed to buy before higher prices hit the market. Underpinned by the strong demand, average vehicle transaction price rose c.1.7% m/m in Apr 2025.

US trade tariffs remain uncertain amid legal reversal. Uncertainty over US trade tariffs continue to cloud the outlook for the global automotive sector. The court of appeal has paused the court of international trade’s earlier decision to block the “Liberation Day” tariffs, including the 25% tariffs on imported cars and parts. The US tariffs on automobiles from Canada, Mexico, and other nations have sparked concerns about supply chain disruptions and rising consumer costs. The latest development implies that global automakers – European and Japanese automakers such as Volkswagen, Mercedes Benz, Subaru, and Honda, which have significant exposure to the US auto market, 5-30% – will continue to face trade uncertainty. Approximately 46% of the 16mn vehicles sold in the US in 2024 were imported.

Supply chain realignment will be long and costly process. The global automotive supply chain is highly integrated, and any shift could face significant strain, especially on global automakers in relocating suppliers. While punitive tariffs may eventually incentivise greater investment in US manufacturing, the path to meaningful reconfiguration will likely span several years given the entrenched global production networks. In the interim, automakers must recalibrate their pricing, production, and capital allocation strategies to preserve market share in the US while navigating near-term policy uncertainty. Hence, we estimate global vehicle industry sales to contract by around 1% each in 2025-2026.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025