- AxJ equities trading at steep valuation discount as headwinds were largely priced in; expect a turnaround in sentiments

- While China equities have underperformed, keep an eye on them as pro-growth measures are anticipated to restore growth in GDP, lifting sentiments

- ASEAN markets will depend on the dollar outlook, with USD weakness boosting their performance

- Bright spots in the region are Indonesian banks and telcos; Thailand’s tourism and industrial property; Singapore’s REITs and banks; Malaysia’s construction sector

- Focus on India given its remarkable economic resilience and strong earnings outlook

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

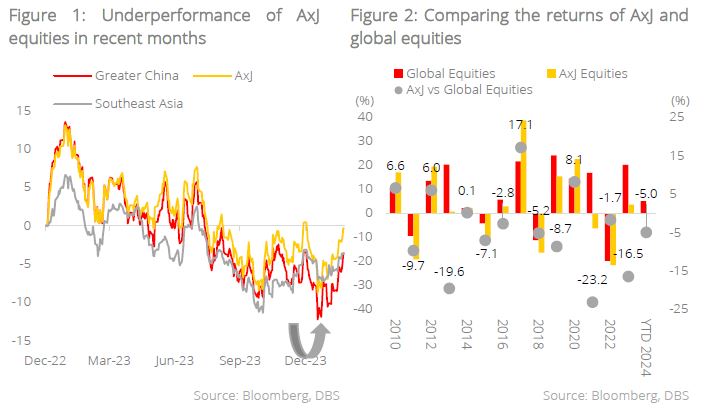

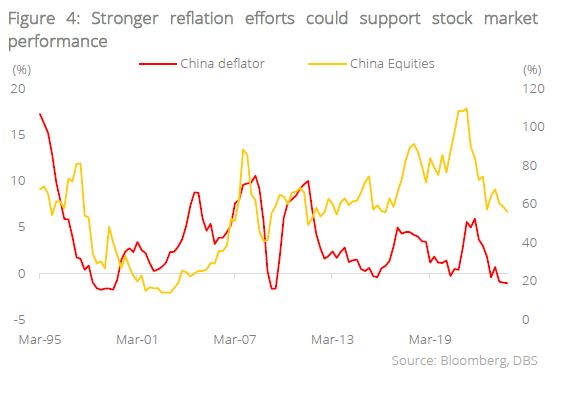

Contrary to our expectations, AxJ equities started 2024 weak, as deflation, slowing consumption, excess supply of properties, and low allocations by global investors persisted.

China – Underperformance in the past decade. 2012, 2017, and 2020 saw China’s outperformance buoy the overall returns of AxJ equities. Apart from that, AxJ has underperformed global equities in most years over the past decade. Between 2021 and 2023, the region recorded three consecutive years of underperformance relative to global peers due to ongoing headwinds. These include concerns over China’s economic recovery amid modest policy measures, persistently high US interest rates, supply chain disruptions, and ongoing tensions between the US and China.

The last time MSCI China declined for three consecutive years (2000-2002), it subsequently rebounded strongly by over 80%. The current sharp discount, extremely low valuation, and light positioning among investors set the stage for a rebound when increasing Chinese government policy support finally turns the economy around. The region’s underperformance is anticipated to reverse then.

SEA – Effects of fiscal stimulus. Southeast Asia (SEA) nations are expected to introduce fiscal stimulus in 2024, reversing the post-Covid fiscal austerity. Notably, according to historical data, government-driven supportive measures profoundly benefited corporate earnings over the mid-to-long term. When implementing fiscal stimulus, however, SEA nations will need to juggle between reigniting growth, keeping a lid on inflation, and managing level of debts.

Since the pandemic began, SEA saw an unprecedented surge in public debt as the region initiated a series of fiscal stimulus to stabilise their domestic economy. Aggravating the situation, as interest rates rose over the past two years, these nations’ financial burdens, in terms of debt repayment, grew heavier. With rates projected to ease from current levels, these governments will likely breathe a sigh of relief and will be able to channel their funds to more productive expenditure.

China

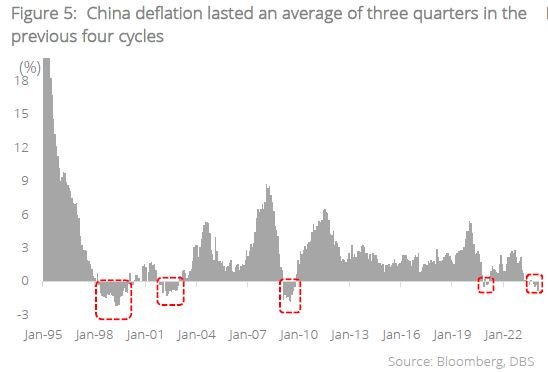

Pro-growth measures to combat deflationary pressures. China’s deflationary pressures have held its market back, with the GDP deflator remaining in negative territory for three quarters in a row, the longest since 1999. This was mainly due to food and energy price weakness, along with sluggish aggregate demand during this post-Covid period. Deflation has not only weighed on corporate earnings, but also resulted in de-rating in the equity markets through rising real interest rates.

It is, however, not unprecedented to witness deflation in China. These instances occurred during the Asian Financial Crisis (1997-1998), China equity selloff (mid-2015), Global Financial Crisis (2008-2009), and Covid-19 (2020).

Historically, deflation persisted for an average length of three quarters, with the longest period lasting seven quarters. In previous occasions of deflation, China’s growth eventually turned around as reflation efforts succeeded. The recent deceleration in price highlights the need for additional support from the government to revitalise the economy and restore consumer confidence. China’s market performance has a close correlation with the deflator data. Hence, the GDP deflator acts as a leading indicator to determine when the market bottoms.

The implementation of pro-growth measures is anticipated to restore growth in the GDP deflator, which would help lift sentiment. With the market’s low base last year, coupled with gradual domestic consumption recovery, we expect price indices to gradually climb out of deflation.

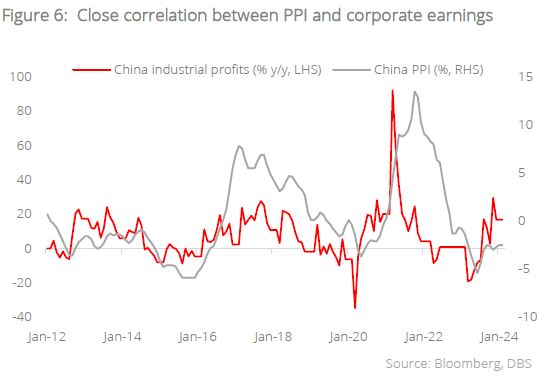

PPI inflation and industrial profits are closely correlated. Previous PPI data moved in tandem with the profit growth momentum. As PPI is expected to regain momentum towards 2H24, it should drive earnings revisions across China equities and support multiple expansions.

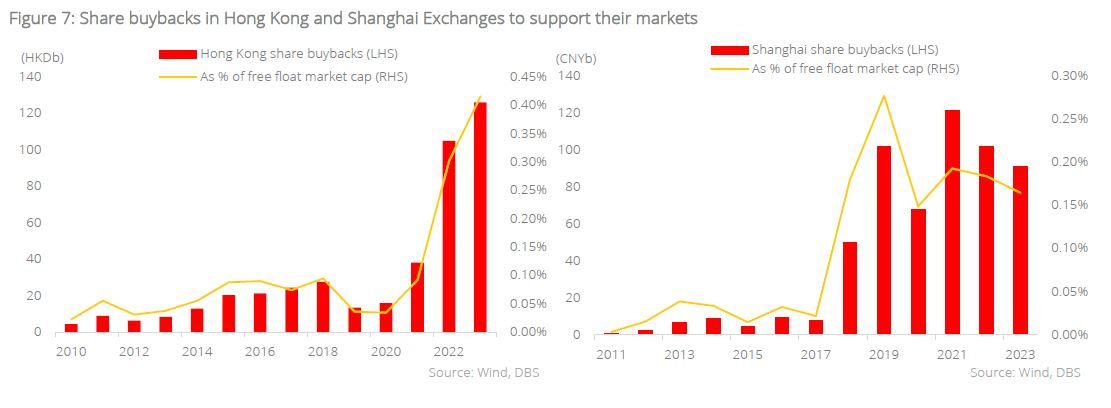

Increasing share buybacks in Hong Kong supportive of markets. The number of buyback announcements in Hong Kong has been rising and reached the highest level towards the end of 2023. It has been observed that whenever Hong Kong’s index reaches a bottom, buyback announcements would increase. It can be surmised that companies are increasingly turning to share buybacks to support their stock prices. Indeed, they spent a record high HKD125bn on buybacks in 2023.

A high level of share buybacks may reflect an increasing number of companies believing their shares are undervalued, having balance sheet strength, and expecting meaningful revaluation in the future. This signals the companies’ confidence in their prospects, which, in turn, helps bolster investor sentiment and builds a floor for stock prices.

In a bid to align its capital markets with global standards, and to better reflect the true value of listing entities, the government has introduced policy initiatives like tagging the market capitalisation of China state-owned enterprises as a key performance indicator for listed companies.

Government initiatives to provide upside for China. In China, slowing consumption and enduring issues facing the real estate sector continue to drag down sentiment. Furthermore, ongoing tensions with the West as well as slowing global growth exacerbate the bifurcated market returns between China equities and global peers.

To shore up the flagging capital markets, revitalise investors’ confidence in capital markets, and rekindle investors’ participation, China’s government has rolled out a series of policy initiatives. We expect the authorities to introduce additional measures to revive the real estate sector, especially to ensure the completion of halted projects and delivery of pre-sold new homes that are still under construction. This would help prevent further downward drag to the broader economy.

ASEAN and India

USD strength key determinant for ASEAN markets. The primary factor influencing ASEAN markets continues to be the USD, with foreign exchange playing a crucial role in equity performance. A decline in the USD is necessary for the region to see improved performance. There is potential for such conditions to materialise this year, especially as the US Federal Reserve considers rate cuts in the later half. Conversely, any resurgence in USD strength could pose challenges for ASEAN markets.

Having said that, sector-specific dynamics within domestic markets are expected to fuel alpha generation. There are promising opportunities in various sectors: Indonesian banks and telcos, Thailand’s tourism and industrial property, Singapore’s REITs and banks, as well as Malaysia’s construction sector. Additionally, the Vietnamese market may experience a re-rating due to the possibility of its index being included in global benchmarks.

Bright spots in the region

Indonesia: Indonesia’s market reacted positively after the presidential election in mid-February. Among the big caps, banks and telco performed well in February amid strong results and robust guidance. In terms of political leadership, until the inauguration in October, we believe President Joko Widodo will continue to execute existing policies to support the economy, including the Capital City project (IKN), social assistance programmes, and downstreaming policy on mineral resources. That said, even after the inauguration, we expect programmes initiated by Widodo to be maintained by the new president.

Singapore: S-REITs experienced a decline in sentiment amid the adjustment of Fed rate hike expectations and a pause in distributions per unit within the US office sector due to ongoing valuation challenges. We favour retail and hospitality REITs, which stand to gain from the “Swiftonomics” – a term describing pop star Taylor Swift’s boost to the local economy as she performs in various countries – and the upcoming series of major MICE events. Meanwhile, Singapore banks continue to pay good dividends amid strong sets of earnings.

Malaysia: There was notable interest in Malaysia’s prominent country-level themes, such as government stimulus efforts, the shift towards renewable energy, and the redevelopment of Johor’s property and economic sectors, which were galvanised by the establishment of a special economic zone between Johor Bahru and Singapore. Construction stocks stand out as primary beneficiaries of these developments.

Thailand: Sentiment towards Thailand remains subdued due to challenges facing the new government amid a sluggish economy and delays in fiscal stimulus measures like the digital wallet scheme. However, we anticipate a resurgence in FDI applications and tourist arrivals, alongside a gradual resolution of political divisions, which should propel the country towards a more stable growth trajectory this year.

Vietnam: Vietnam has emerged as one of the fastest-growing markets in ASEAN over the past five years, benefiting significantly from supply chain shifts amid geopolitical tensions, as businesses adopt strategies like China+1. With a CAGR of 7.1% since 2017, per-capita GDP surpassed USD4,000 in 2022. Despite substantial growth, Vietnam remains in the early stages of urbanisation, with only 38% of the population residing in urban areas as of 2021.

Thus, the government is committed to infrastructure investment to drive the urbanisation rate and GDP per capita. We anticipate a potential market re-rating, especially with considerations for Vietnam’s index to be included in global benchmarks possibly within the current year.

India: India’s economy has demonstrated remarkable resilience thus far and is poised to sustain its strong performance into the upcoming year. Moreover, earnings projections continue to exceed expectations, with anticipated growth of 14% over the next 12 months, a figure we deem realistic given India’s robust GDP expansion of over 8%. To navigate the elevated valuations while capitalising on attractive growth prospects, we suggest considering investment in small- or mid-cap funds. These funds are particularly appealing to domestic investors, who are experiencing ample liquidity. Moreover, recent regulatory cautions regarding such funds are expected to prompt enhanced risk management practices.

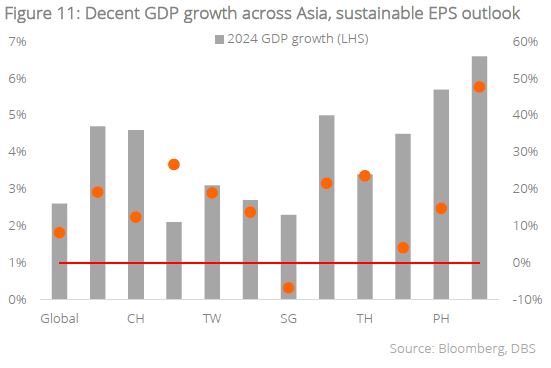

Overall, AxJ corporates are forecast to deliver earnings growth exceeding 15% in 2024, significantly outperforming global markets and marking a sharp recovery from the previous year. In North Asia, Taiwan, and South Korea, earnings are expected to grow between 15-25%, riding on a recovery in semiconductor demand. China firms, meanwhile, are projected to deliver earnings increase in the range of mid-teens.

This expectation is supported by the region’s robust GDP growth forecast of 4.7% and the bottoming of exports. Against this backdrop, Asia, led by India, the Philippines, Indonesia, and China, will maintain GDP growth rates considerably above global average. As earnings continue to improve and the path of recovery becomes clearer, this will prompt sustainable expansion in valuation multiples for AxJ companies.

The existing headwinds surrounding the region have been largely priced in by investors. At forward PE ratio of 11-12x, AxJ is trading at steep valuation discounts to historical average and global average. Thus, the emergence of any positive catalysts could support the downside and lead to a turnaround in sentiment.

Driven by investor preference for quality growth on the back of GDP deflator bottoming, rotation to AxJ equities is a trend to look out for this year. Catalysts include:

- Share buybacks and the impact on market confidence

- Fed rate cuts to drive down risk-free rates and revive investors’ risk appetite

- Steep valuation discount to global peers

- Possibilities of fiscal stimulus to be front-loaded

- Lower expectations after three consecutive years of underperformance

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024