- Gold was off to a shaky start in 2024, but has remained relatively resilient, testing its 100-DMA just once on 14 Feb

- Gold’s resilience a result of geopolitical risk, but that factor could also be a potential source of supply chain pressure& inflation risk

- Central bank buying maintained full momentum in 2023; we expect this to continue, driven by de-dollarisation

- Private markets present significant investable opportunity set, offering enhance risk-adjusted returns

- Diversification is key given varied cashflow patterns and return profiles across private market strategies

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Gold

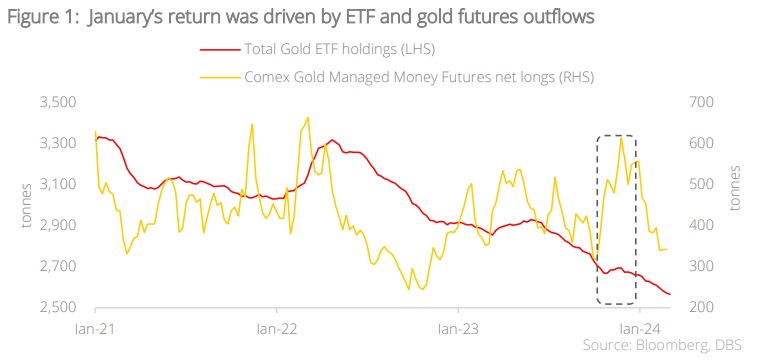

Retracing some of December’s gains. Gold was off to a shaky start in 2024, giving back some gains (- 0.9% YTD as at 29 Feb) after a stellar performance in December last year. This was somewhat expected given: i) profit-taking after such a substantial rally and ii) further developments on the rates front that tempered optimism for gold. On point (ii), there was a resurgence in inflation as well as continued labour market resilience in the US in the first month of 2024, which all but dashed hopes of early Fed rate cuts, resulting in a strengthening dollar and Treasury yields. This persistent US economic strength had an impact on short-term investment positioning for gold, with global gold ETFs seeing an outflow of 51 tonnes in January, and COMEX Gold Managed Money Futures seeing a reduction in net longs (-206 tonnes) in January.

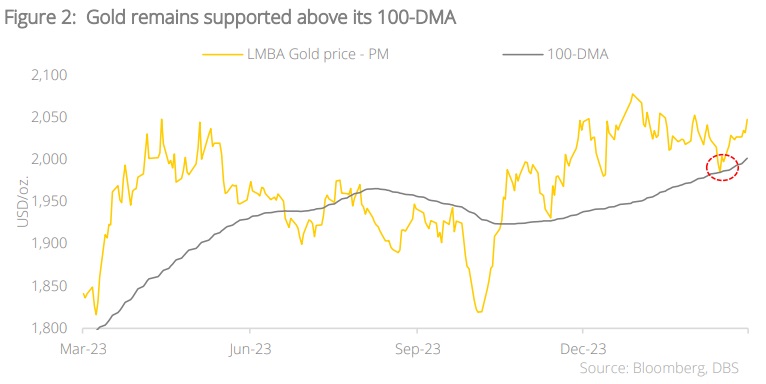

Resilience still a key theme for gold. Notwithstanding these retracements, it could be argued that gold remained relatively resilient. YTD, it tested its 100-Day Moving Average (100-DMA) just once, on 14 Feb. During the afternoon gold price-setting session, the LBMA price fell to USD1,985/ oz. — the same level as its 100-DMA. However, it rebounded shortly after. Since then, prices have remained comfortably above USD2,000/oz., which is similar to where levels were in late November last year, and this is despite the fact that the dollar and rates have strengthened marginally since then. This resilience suggests that the consensus view for gold is still fundamentally positive, and that expectations for future rate cuts are still alive and well, notwithstanding that the timing of these cuts might be later than initially expected due to the resilience of the US economy.

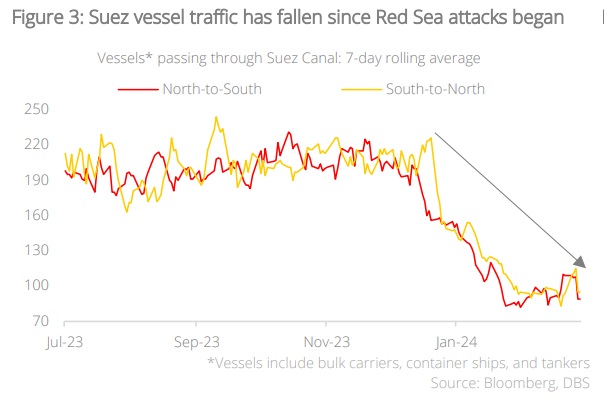

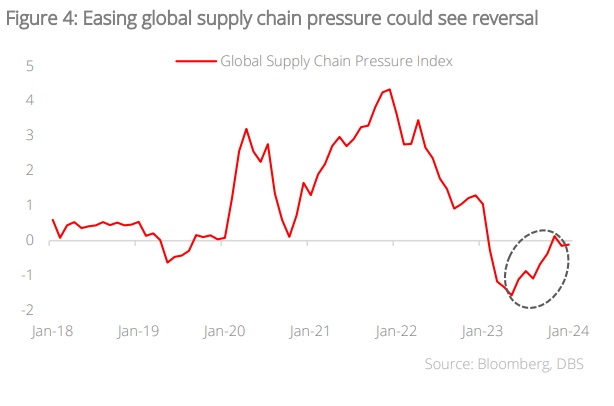

Geopolitical risk could be a double-edged sword. Part of gold’s resilience in the first two months of 2024 could also be attributed to the persistence of geopolitical risk. It has been more than two years since the inception of the Russia-Ukraine war, with no end in sight. What is more pertinent is the conflict in the Middle East between Israel and Hamas, which escalated last November in the form of proxy wars in the Red Sea conducted by pro Hamas Houthi militants. As a safe-haven asset, gold would no doubt have benefited from the prevailing geopolitical climate. However, the flipside of geopolitical risk is that it can be a potential source of supply chain pressure and inflation risk. Case in point, vessel traffic through the Suez Canal has fallen substantially since the Houthi attacks in the Red Sea began, and that has impacted freight cost and energy prices among other things. If inflation rises as a result, we could see yields back up further, which would be negative for gold.

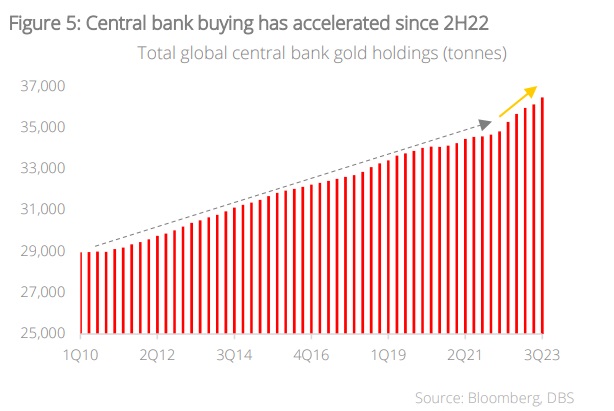

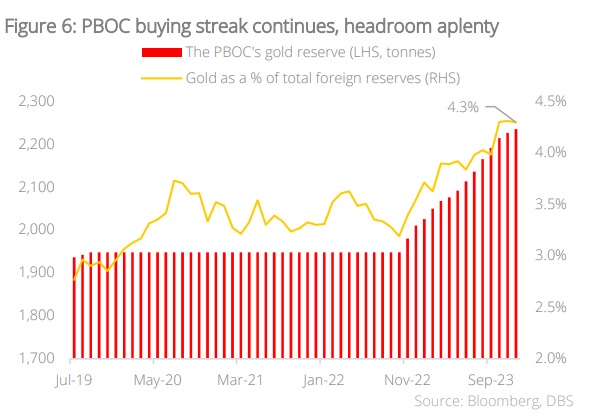

Central banks to the rescue. Amid the volatility of the past two years, the one thing that has remained consistent is strong central bank gold-buying. Looking at the long-term trend, we can see a marked differentiation between buying activity from pre-2Q22, and 2Q22 onwards; there has been a clear acceleration in purchases during the latter period. To provide an idea of how much buying has grown, 2022 was a record year for central bank gold-buying, with demand totalling 1,081.9 tonnes, with 2023 following closely behind (1,037.4 tonnes). We expect this trend to continue for two reasons: i) rising instances of international sanctions; and ii) increasing momentum in the long-term de dollarisation trend. On point (i), the world is more cognizant than ever of sanctions risk, especially following Russia’s invasion of Ukraine, and gold presents a way for countries to build resilience and possibly circumvent sanctions. On point (ii), the slow but steady shift towards a multi- polar world is increasing the appeal of gold to many countries. Even though there is no immediate threat to the dollar’s reserve currency status, countries both emerging and developed are increasingly looking to diversify their foreign exchange reserves to include neutral hard assets such as gold. The central banks of China, Poland, and Singapore were among the largest buyers in recent years. Notably, resilient central bank buying not only provides long-term support for gold, but also acts as a price stabiliser for the precious metal. Central banks are price-sensitive to some extent, and as such, when gold experiences sell-downs, it is not uncommon for some of them to partake in opportunistic buying.

Conclusion

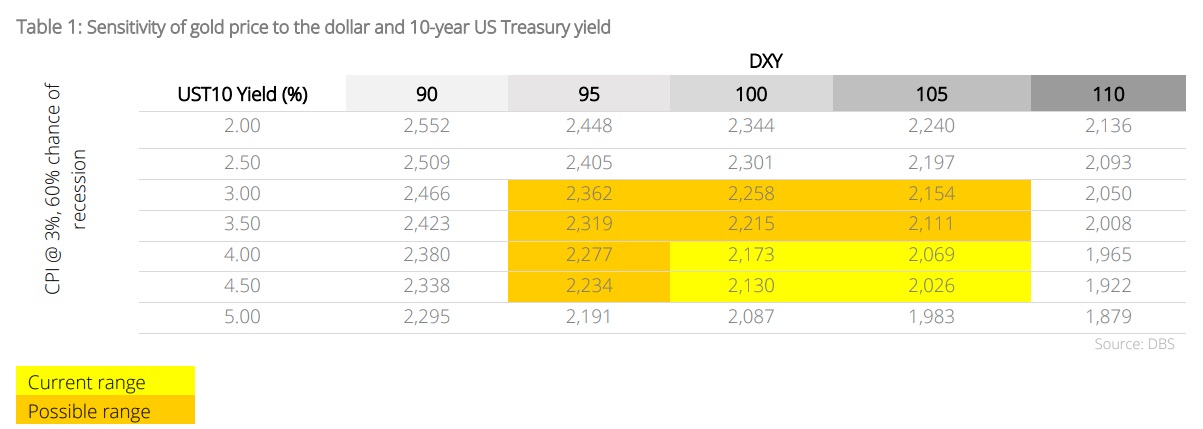

Destination remains but road ahead could be rocky. On the back of central bank buying, the shift towards a multi-polar world order, and strong demand from China and India, the long-term tailwinds for gold remain intact. In the short term, uncertainty in the form of conflict as well as a deluge of elections around the globe should also be a net positive for gold. However, all that will most likely play second fiddle to developments on the rate and dollar front. If inflation growth and employment data continue to surprise on the upside, we could see gold slide. However, even if macro data does come in hot and further rate hikes are implemented, there are silver linings for the precious metal; further rate hikes will increase the probability of recession overtime, and when recession does occur, rate cuts will most certainly take place. All in all, while we expect rate cuts to eventually come into play, the biggest uncertainty lies in its timing. We maintain our 12-month target price of USD2,250 on the back of these factors.

Private Assets

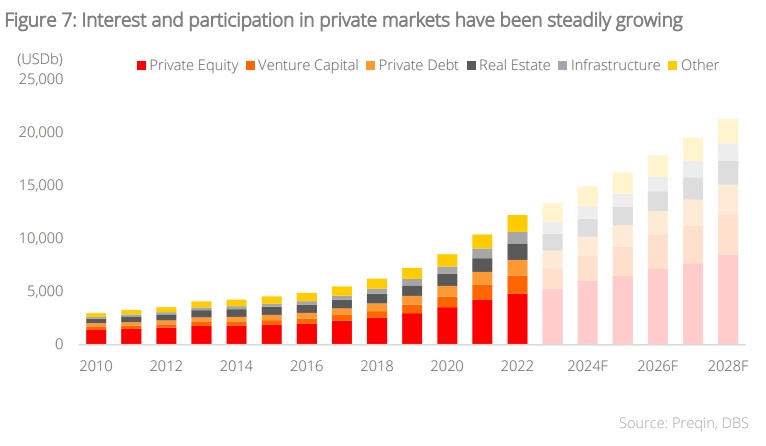

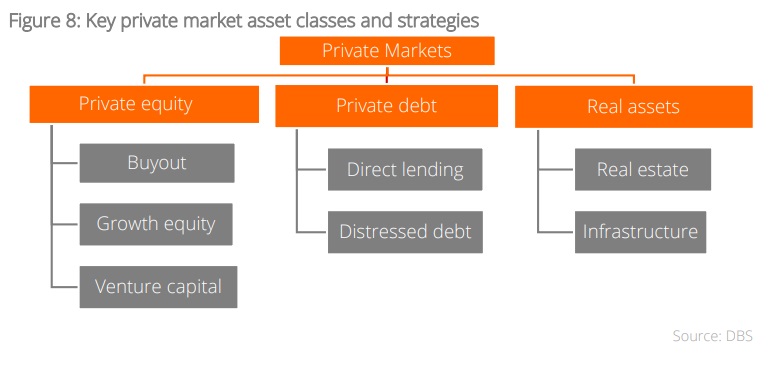

Private markets have rapidly risen in prominence over the past two decades. Businesses and investors alike are increasingly appreciating the benefits of remaining outside the public eye, both in terms of more value being created, and rising investor participation in the private markets. Today, many of the largest and most influential companies are privately owned. With private markets presenting a significant investable opportunity set, boasting the epicentre of corporate growth and value creation, and offering outsized returns, it is no wonder that investor interest and participation in the private markets remains steadily growing. As investor awareness and interest in the private markets builds, this article provides an introduction for investors looking to build an allocation to this space within their core portfolio.

Why invest in private markets? Benefits of investing in private markets include:

- A wider investment universe available on private markets. Many expressions of emerging innovations remain underrepresented in public markets, but investors can gain access to such opportunities widening their universe into private markets. Furthermore, rising concentration of performance on public markets also underscores a need to look to private markets as an important source of diversification.

- Value creation through active management. Due to substantial stakes and generally illiquid positions, private market firms tend to emphasise a long-term investment horizon. This, combined with their level of involvement in managing the investments, aligns their interest closely with those of limited partners, fostering a shared commitment to creating value through sustainable growth and success of portfolio companies, rather than focusing on immediate stock price fluctuations.

- Harnessing behavioural benefits of illiquidity. Although illiquid private asset holdings could make it challenging for investors to react to unforeseen changes or opportunities, this illiquidity also protects against impulsive selling tendencies that may arise during volatile market conditions, shielding the portfolio from inherent behavioural biases.

Features of private market investing. While the prospect of improved risk-adjusted returns and an expanded opportunity set on private markets may be enticing, practical issues in introducing private market exposure to a portfolio often prove a barrier to entry for even sophisticated investors. Complexities include:

- How much, and when, should we commit to reach allocation targets?

- What should we do with committed, uncalled capital?

- How do we maintain our allocations, as funds return capital to us?

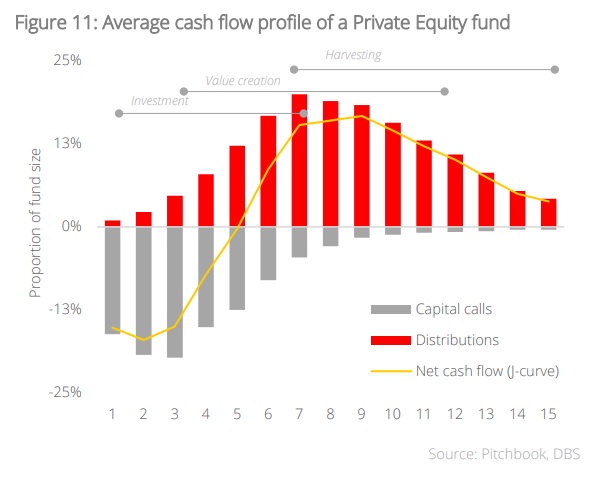

Investing in a typical private equity fund. Investing in private assets through a typical private equity fund works as follows: An investor commits as an LP to a new primary fund. This is a close-ended vehicle with a limited lifetime, that invests directly into private companies or assets. The fund does not typically call committed capital all at once. Instead, this is done gradually over a predetermined period as the fund makes investments in portfolio companies. The general partner would generally work with the portfolio investments’ management teams to enhance their value, until the investments are ripe for harvesting. In the later years of the fund’s lifetime, the fund sells its investments and this generates cash that is distributed back to its LPs. This overall cash flow pattern is referred to as the “J-curve”, represented below:

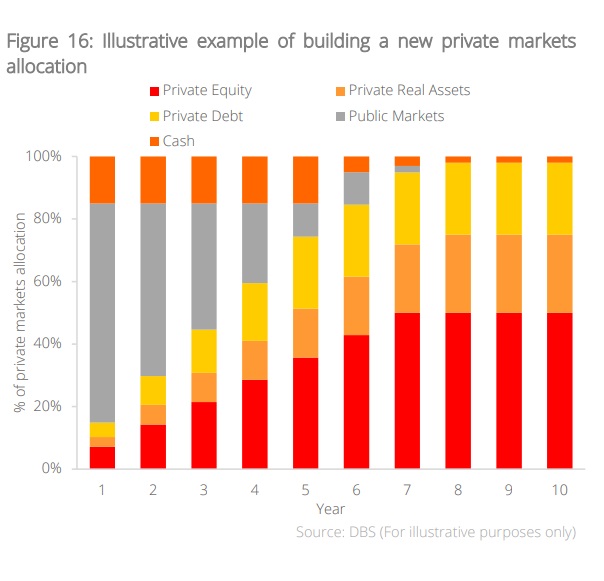

Reaching target allocations in private assets. This J-curve cash flow pattern typical of private market funds implies that, unlike public market investing, investors new to private markets would not be able to achieve their target exposure to any private market asset class with a single fund at one go. Instead, building and maintaining a private market programme is a multi-year process that entails cash flow planning, and pacing commitments to new funds in various asset classes.

Cash flow planning. Capital calls and distributions are uncertain and beyond an LP’s control. Hence investors must carefully plan for capital calls and distributions as they budget for cash flow needs at each stage of private markets investing.

- Capital calls. A commitment to a close-ended fund may take several years to be called, and LPs must ensure sufficient liquidity to meet these obligations. To avoid a cash drag on returns, investors may maintain capital earmarked for private market capital calls invested in liquid public instruments until it is needed – to capture beta of the market along the way, or held in cash or cash-equivalents for liquidity.

- Distributions and performance. As a fund’s portfolio of investments matures, underlying investment performance, and distributions during the investment period (which are uncertain at time of initial commitment) work against an investor’s allocation target. Consequently, maintaining a stable allocation to private assets entails consistently pacing allocations to fresh investments. Ultimately, by constructing a rolling programme of investing into private market funds, an investor’s portfolio will effectively become self-funding, as distributions from funds of earlier vintages would generally offset contributions to new funds, reducing additional cash outlay required from investors.

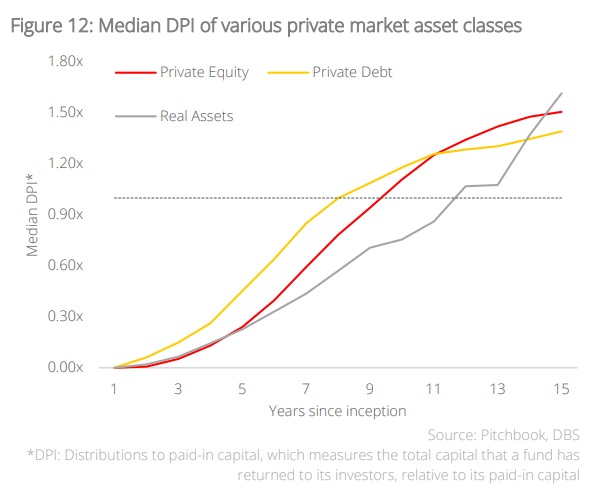

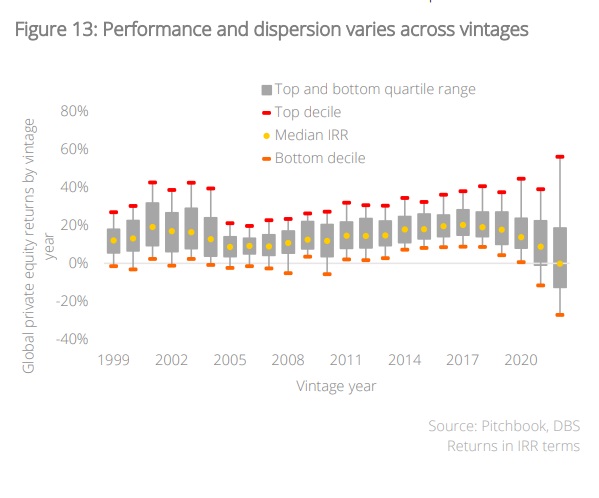

Diversification across strategies, vintages, and managers. Investors allocating to private markets must further note that private market strategies are not homogenous. For example, based on Pitchbook’s analysis, private debt funds on average call and distribute capital faster than private equity or real assets, while venture capital’s boom and bust cycle presents more volatile returns. Each different vintage year (starting year of a fund) has historically also seen differences in the dispersion of fund performance and median performance.

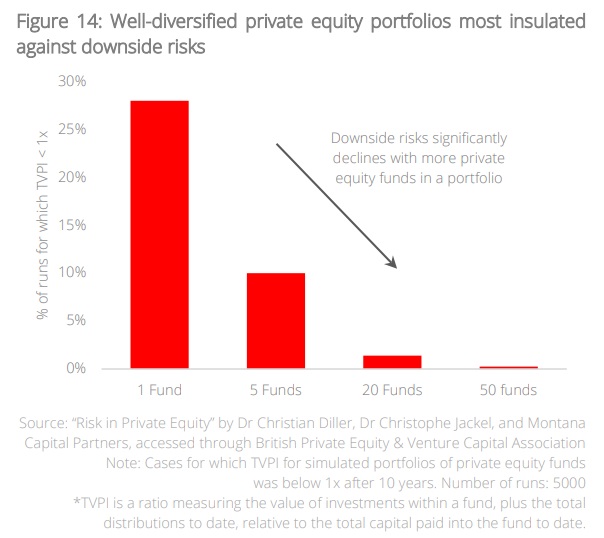

Varied cash flow and return profiles within private markets underscore the importance of diversification within private market allocations. Spreading commitments across geographies, managers, strategies, and vintage years, has been found to have a positive effect on the risk exposure of a private asset portfolio, by reducing reliance on any economic environment or manager. A study by Diller and Jackel found that risks of losing capital in a portfolio of randomly selected funds declines significantly as more funds are added. This reiterates that committing regularly to multiple new funds is necessary, not only to maintain a stable allocation over time, but also construct a diversified and resilient portfolio.

General guidelines for developing a private markets investment programme:

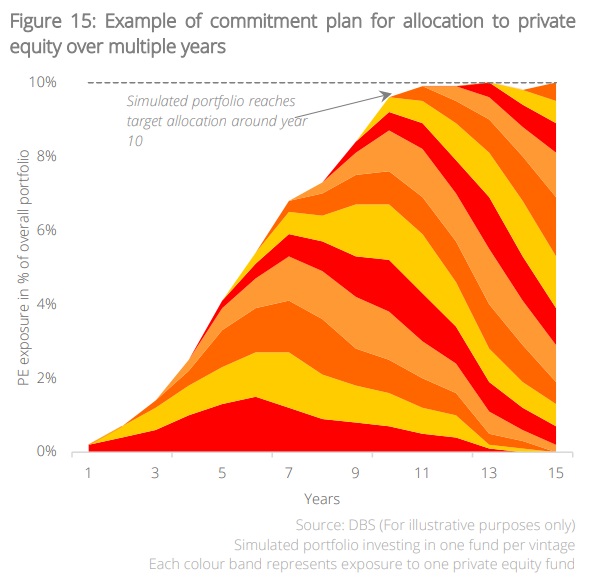

- Investors new to private assets may build their target exposure to each asset class over a number of years, working backwards from the length of time they expect to be fully allocated to private markets.

- By pacing allocations across different vintages, the private market programme eventually becomes “self-funding” as funds of earlier vintages eventually begin distributing capital, and this cash may be re-deployed to new funds.

How do I invest in the private markets? Given the relative complexity of investing in private market funds, exposure through primary funds is best pursued by investors with the necessary resources. Alternatively, individuals may choose to delegate these responsibilities to a discretionary program. Under such a programme, an investment advisor would not only provide the services needed to manage a funds programme, but also facilitate access to highly sought after, best-in-class fund managers. It is also worth noting that, in addition to primary funds, there are a range of different options available to investors seeking private markets exposure. The suitability of each approach depends on factors including an investor’s allocation size, level of expertise and preferred degree of involvement.

- Direct or co-investments. Investments can be made directly into private companies or assets. This typically involves a high level of resources and expertise to source, evaluate, and manage investments. It also requires scale, which makes it unsuitable for some investors seeking diversified exposure to private markets. Investors may also co-invest alongside a general partner (usually a private asset firm) which will undertake management responsibility, for a chance to invest alongside specific private asset fund managers.

- Secondary funds. Secondary funds purchase existing primary fund stakes from LPs. By purchasing interests in primary funds further down their performance cycle, secondary funds mitigate J-curve effects and reduce the duration of illiquidity for investors. Other than a shorter/ shallower J-curve, exposure to secondary funds may also be useful at inception of a primary market programme to provide quicker exposure and diversification across strategies, geographies, and vintage years.

- Fund of funds. Fund of funds pool investors capital to create a diversified portfolio of private market funds. Investors give up control over their investment, in exchange for a convenient means for first-time private markets investors to gain diversified exposure to hard-to-access top tier managers. Fund of funds are often selected by investors seeking diversified private market exposure, but for whom implementing a primary funds program may not be feasible.

- Semi-liquid funds. These are open-ended structures offering investors the option to subscribe and redeem shares on a regular basis. Liquidity in semi-liquid structures is often engineered through part of the portfolio being invested in liquid assets, which may dilute the exposure to private markets. Although there is typically no J-curve, lock up periods and fund-level gating may still apply. Consequently, while investors may fall back on liquidity mechanisms if individual circumstances require them to withdraw capital, this feature should not be relied on in market drawdowns or duress.

Balancing liquidity and capital needs. Ultimately, investors must consider the following in establishing how they choose to access the private markets: administration, portfolio diversification, cost, and the long-term commitment required to participate in a private markets program. For example, smaller scale individual investors may consider fund of funds or semi-liquid private assets as a portfolio construction tool, given the illiquid nature of private market investments and their limited amount of capital to deploy. Ultimately, to construct a successful private market program, investors should explore and understand the various facets to building a program that allows them to enjoy the benefits of investing in the private markets for years to come.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024

Related insights

- Equinix Inc 26 Jul 2024

- Strong 2Q GDP Highlights Economic Resilience26 Jul 2024

- Research Library26 Jul 2024