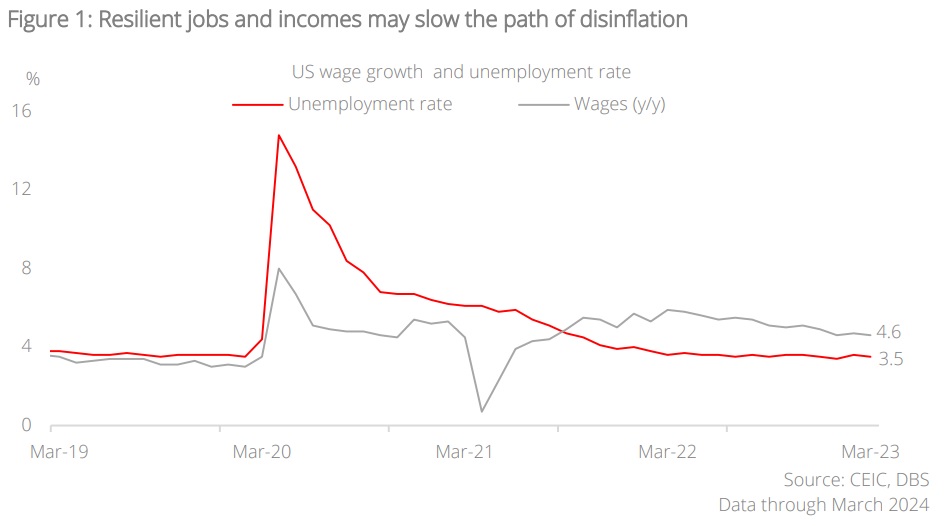

- US: March inflation data shows persistent price pressures; strong labour market may slow disinflation but sharp rebound in inflation is unlikely given spate of supply side reforms underway

- China: Official PMI returns to expansionary territory for the first time in six months amid weaker-than-expected March inflation data

- Taiwan: Economic recovery in Taiwan prompts considerations for policy tightening; cyclical upturn in the global semiconductor sector should continue to drive exports growth this quarter

- Thailand: BOT keeps policy rate unchanged, maintaining patience over current soft economic conditions; updated 2024 growth forecast of 2.6% at lower end of its previous range

相關見解

- 每周外匯速遞 - 日元跌至34年新低,關注美聯儲會議29 Apr 2024

- 2024年第一季: 美國利率將逐漸下降22 Apr 2024

- 黃金:再創歷史新高17 Apr 2024

US: Sticky inflation taking hold. The March inflation print marked the third month in a row that prices pressures surprised on the upside, triggering a spike in US yields across the curve. Headline and core CPI both came in at 0.4% m/m (higher than consensus of 0.3%). Shelter and gas prices were the two main culprits behind the elevated inflation print. Notably, categories including apparel, medical care, and transportation services also saw meaningful price increases, indicating that inflation is broad-based.

Implications of the strong labour market. Withstanding two years of monetary policy tightening, the US economy continues to chug away at above-trend growth rate, pulling up the labour market with it. The statistics are impressive across a wide range of measures. Unemployment is below 4%, weekly initial claims for unemployment insurance has been near historical lows for over two years, and the labour force participation rate is on the rise after a few years of pandemic-driven dip. Labour market would have been even tighter had it not been for the fact that immigration has picked up, boosting the supply of workers.

Sharp rebound in inflation unlikely. The difference with prevailing inflation and what was seen in 2022 is that it is taking place under favourable supply side conditions, ensuring a cap on potential upside risks going forward. However, clear signs of a high-pressure economy, characterised by strong growth and sticky inflation, is going to make it rather difficult for the Fed to (i) express comfort with the inflation trend and (ii) embark on a rate cut cycle any time soon. Our longstanding call has been rate cuts only in 2H24. That call remains intact, although the type of rate cuts plausible under the prevailing macro scenario is now mired in uncertainty.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

本資訊是由星展銀行集團公司(公司註冊號: 196800306E)(以下簡稱“星展銀行”)發佈僅供參考。其所依據的資訊或意見搜集自據信可靠之來源,但未經星展銀行、其關係企業、關聯公司及聯屬公司(統稱“星展集團”獨立核實,在法律允許的最大範圍內,星展集團針對本資訊的準確性、完整性、時效性或者正確性不作任何聲明或保證(含明示或暗示)。本資訊所含的意見和預期內容可能隨時更改,恕不另行通知。本資訊的發佈和散佈不構成也不意味著星展集團對資訊中出現的任何個人、實體、服務或產品表示任何形式的認可。以往的任何業績、推斷、預測或結果模擬並不必然代表任何投資或證券的未來或可能實現的業績。外匯交易蘊含風險。您應該瞭解外匯匯率的波動可能會給您帶來損失。必要或適當時,您應該徵求自己的獨立的財務、稅務或法律顧問的意見或進行此類獨立調查。

本資訊的發佈不是也不構成任何認購或達成任何交易之要約、推薦、邀請或招攬的一部分;在以下情況下,本資訊亦非邀請公眾認購或達成任何交易,也不允許向公眾提出認購或達成任何交易之要約,也不應被如此看待:例如在所在司法轄區或國家/地區,此類要約、推薦、邀請或招攬係未經授權;向目標物件進行此類要約、推薦、邀請或招攬係不合法;進行此類要約、推薦、邀請或招攬係違反法律法規;或在此類司法轄區或國家/地區星展集團需要滿足任何註冊規定。本資訊、資訊中描述或出現的服務或產品不專門用於或專門針對任何特定司法轄區的公眾。

本資訊是星展銀行的財產,受適用的相關智慧財產權法保護。本資訊不允許以任何方式(包括電子、印刷或者現在已知或以後開發的其他媒介)進行複製、傳輸、出售、散佈、出版、廣播、傳閱、修改、傳播或商業開發。

星展集團及其相關的董事、管理人員和/或員工可能對所提及證券擁有部位或其他利益,也可能進行交易,且可能向其中所提及的任何個人或實體提供或尋求提供經紀、投資銀行和其他銀行或金融服務。

在法律允許的最大範圍內,星展集團不對因任何依賴和/或使用本資訊(包括任何錯誤、遺漏或錯誤陳述、疏忽或其他問題)或進一步溝通產生的任何種類的任何損失或損害(包括直接、特殊、間接、後果性、附帶或利潤損失)承擔責任,即使星展集團已被告知存在損失可能性也是如此。

若散佈或使用本資訊違反任何司法轄區或國家/地區的法律或法規,則本資訊不得為任何人或實體在該司法轄區或國家/地區散佈或使用。本資訊由 (a) 星展銀行集團公司在新加坡;(b) 星展銀行(中國)有限公司在中國大陸;(c) 星展銀行(香港)有限責任公司在中國香港[DBS CY1] ;(d) 星展(台灣)商業銀行股份有限公司在台灣;(e) PT DBS Indonesia 在印尼;以及 (f) DBS Bank Ltd, Mumbai Branch 在印度散佈。

相關見解

- 每周外匯速遞 - 日元跌至34年新低,關注美聯儲會議29 Apr 2024

- 2024年第一季: 美國利率將逐漸下降22 Apr 2024

- 黃金:再創歷史新高17 Apr 2024

相關見解

- 每周外匯速遞 - 日元跌至34年新低,關注美聯儲會議29 Apr 2024

- 2024年第一季: 美國利率將逐漸下降22 Apr 2024

- 黃金:再創歷史新高17 Apr 2024