- Equities: US Equities reached record highs on expectations of rate cuts, supported by resilient consumer spending and over USD6t sitting on the sidelines

- Credit: Historical widening of credit spreads following a Fed pause underscores need for selectiveness in credit risks. Sweet spot remains with A/BBB Credit in 3-5Y duration segment

- FX: BOJ getting closer to ending its ultra accommodative monetary policy; Potential JPY recovery vs DM currencies amid weak USD bias

- Rates: USD rates undecided on direction after passing through US labour data; 2Y to 10Y yields close to the bottom of recent ranges

- The Week Ahead: Keep a lookout for US Initial Jobless Claims; Japan PPI Number

相關見解

- 每周外匯速遞 - 地緣政治添不確定性22 Apr 2024

- 2024年第一季: 美國利率將逐漸下降22 Apr 2024

- 黃金:再創歷史新高17 Apr 2024

US Equities reached all-time high as Fed signals potential rate cuts. Investor optimism surged as Fed Chair Jerome Powell's testimony before a Senate committee ignited hopes for rate cuts in the June Federal Open Market Committee (FOMC) meeting. Powell's remarks, suggesting the central bank was nearing a point where it could confidently begin reducing interest rates, provided the catalyst to propel US indices to unprecedented levels. The S&P 500 and Nasdaq rallied to record highs on Friday’s (8 Mar) trading session. This remarkable milestone was achieved despite mixed economic data. Despite a higher-than-expected unemployment rate of 3.9% for February, compared with the consensus estimate of 3.7%, the US economy added 275k jobs, surpassing the forecasted 200k figure.

We continue to remain constructive on US Equities as we head into 2024, buoyed by the prospect of the Federal Reserve initiating interest rate cuts as early as June. Complementing this tailwind is the remarkable resilience exhibited by consumer spending, underpinned by a robust labour market and solid wage growth. Moreover, the staggering USD6t parked in money market funds on the sidelines could further propel the rally.

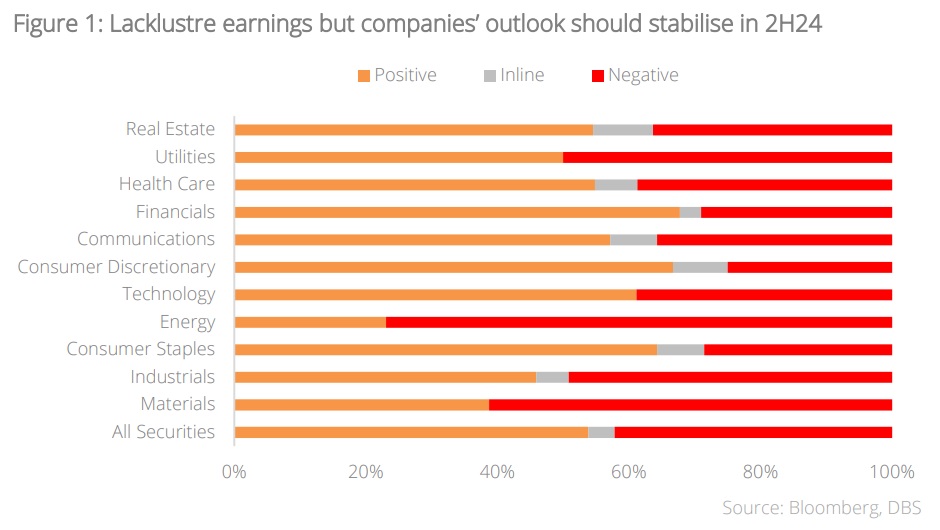

Topic in focus: Europe Equities – Sluggish outlook continue to weigh on earnings. With c.60% of companies having reported earnings, STOXX 600 EPS beats are at a near decade low. Consumer Discretionary, Consumer Staples, Technology, and Financials posted strong earnings beats, while Energy and Materials were among the weakest. Earnings revisions and expectations continue to trend south for Europe Equities, with consensus expecting mid-teens contraction in 1Q24.

On the back of abating inflationary pressures, a more accommodative European Central Bank (ECB), and cyclical recovery in the manufacturing sector, we believe Europe’s economy should show signs of stabilisation in the later half of the year. As we await pivotal factors for upward revaluation, we remain defensive on Europe Equities – we stay overweight on the Tech sector, focusing on upstream semiconductors. In Real Estate, we maintain specific interest in logistics and data centre-related assets. While European banks had a good year in 2023, we expect headwinds from slowing economic growth and declining interest margins. For the luxury sector, we advocate brands which align with the “Quiet Luxury” theme. Healthcare earnings should stay resilient through economic cycles, particularly those specialising in medicines for conditions such as obesity and cancer.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

本資訊是由星展銀行集團公司(公司註冊號: 196800306E)(以下簡稱“星展銀行”)發佈僅供參考。其所依據的資訊或意見搜集自據信可靠之來源,但未經星展銀行、其關係企業、關聯公司及聯屬公司(統稱“星展集團”獨立核實,在法律允許的最大範圍內,星展集團針對本資訊的準確性、完整性、時效性或者正確性不作任何聲明或保證(含明示或暗示)。本資訊所含的意見和預期內容可能隨時更改,恕不另行通知。本資訊的發佈和散佈不構成也不意味著星展集團對資訊中出現的任何個人、實體、服務或產品表示任何形式的認可。以往的任何業績、推斷、預測或結果模擬並不必然代表任何投資或證券的未來或可能實現的業績。外匯交易蘊含風險。您應該瞭解外匯匯率的波動可能會給您帶來損失。必要或適當時,您應該徵求自己的獨立的財務、稅務或法律顧問的意見或進行此類獨立調查。

本資訊的發佈不是也不構成任何認購或達成任何交易之要約、推薦、邀請或招攬的一部分;在以下情況下,本資訊亦非邀請公眾認購或達成任何交易,也不允許向公眾提出認購或達成任何交易之要約,也不應被如此看待:例如在所在司法轄區或國家/地區,此類要約、推薦、邀請或招攬係未經授權;向目標物件進行此類要約、推薦、邀請或招攬係不合法;進行此類要約、推薦、邀請或招攬係違反法律法規;或在此類司法轄區或國家/地區星展集團需要滿足任何註冊規定。本資訊、資訊中描述或出現的服務或產品不專門用於或專門針對任何特定司法轄區的公眾。

本資訊是星展銀行的財產,受適用的相關智慧財產權法保護。本資訊不允許以任何方式(包括電子、印刷或者現在已知或以後開發的其他媒介)進行複製、傳輸、出售、散佈、出版、廣播、傳閱、修改、傳播或商業開發。

星展集團及其相關的董事、管理人員和/或員工可能對所提及證券擁有部位或其他利益,也可能進行交易,且可能向其中所提及的任何個人或實體提供或尋求提供經紀、投資銀行和其他銀行或金融服務。

在法律允許的最大範圍內,星展集團不對因任何依賴和/或使用本資訊(包括任何錯誤、遺漏或錯誤陳述、疏忽或其他問題)或進一步溝通產生的任何種類的任何損失或損害(包括直接、特殊、間接、後果性、附帶或利潤損失)承擔責任,即使星展集團已被告知存在損失可能性也是如此。

若散佈或使用本資訊違反任何司法轄區或國家/地區的法律或法規,則本資訊不得為任何人或實體在該司法轄區或國家/地區散佈或使用。本資訊由 (a) 星展銀行集團公司在新加坡;(b) 星展銀行(中國)有限公司在中國大陸;(c) 星展銀行(香港)有限責任公司在中國香港[DBS CY1] ;(d) 星展(台灣)商業銀行股份有限公司在台灣;(e) PT DBS Indonesia 在印尼;以及 (f) DBS Bank Ltd, Mumbai Branch 在印度散佈。

相關見解

- 每周外匯速遞 - 地緣政治添不確定性22 Apr 2024

- 2024年第一季: 美國利率將逐漸下降22 Apr 2024

- 黃金:再創歷史新高17 Apr 2024

相關見解

- 每周外匯速遞 - 地緣政治添不確定性22 Apr 2024

- 2024年第一季: 美國利率將逐漸下降22 Apr 2024

- 黃金:再創歷史新高17 Apr 2024