Highly customisable to investors’ specific needs

Ability to design product features in order to articulate a particular market view

Potential to earn enhanced yields, based on market price movements

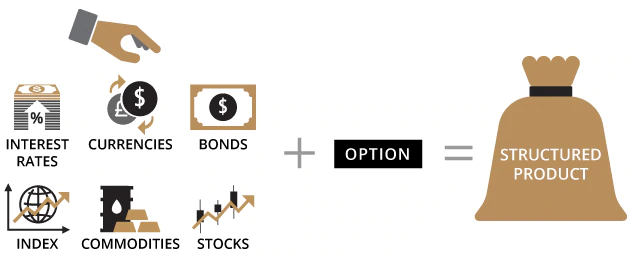

Structured products are financial instruments whose performance or value is linked to that of an underlying asset, product, or index. These may include market indices, individual or baskets of stocks, bonds, and commodities, currencies, interest rates or a mix of these.

Because of their huge variety, there is no simple definition—or uniform formula to calculate the risk and payoff—of structured products.

Generally, most structured products incorporate “options”, a type of derivative product that can give investors the right to buy or sell something at a pre-determined price (called “Strike Price") and date. It can also involve the investor giving a financial institution the right to buy from or sell to him something at a pre-determined price.

In a “call” option, the option holder has the right to buy the underlying asset at a certain price. In a “Put” option, the option holder has the right to sell the underlying asset at a certain price.

Return

Apart from fixed and/or variable returns, there may also be capital appreciation depending on the performance of the underlying asset at maturity.

However, investors may receive less than their principal at maturity if the underlying asset performs against them.

Principal

Investors may potentially lose part or their entire principal when the underlying asset performs against them.

The principal is also exposed to counterparty risk, as structured products typically involve derivative arrangements with counterparties.

Structured notes offer no principal guarantees (unless a third-party guarantees the payout of principal in the event the structured note issuer defaults).

Because there is a wide variety of structured notes in the market, there is no simple description of how they work. But they typically involve options: the structured note issuer either buys or sells an option on the reference asset or security, and the investor gives the issuer the right to put securities on or call securities from him/her.

Structured notes fall into two broad categories:

Some specific types of structured notes include:

Issuers can tailor structured products to meet investors’ differing financial circumstances and needs.

Structured products offer potential yield enhancement, if your view of the market proves correct and the product issuer is credit-worthy.

Some structured notes offer strike prices—the price at which a call or put option is exercised—that are significantly below market prices; for example, 90% or 95% strikes. So even if the underlying securities fall below the initial price, but above the strike prices, the investor can still receive the principal plus the agreed “coupon”.

If the prices of the stocks close on maturity above the initial price, the investor gets his principal plus coupon or the upside of the reference equity. If the underlying is a basket of stocks, the investor receives the upside of the worst-performing stock.

As a structured product’s performance depends on the underlying asset’s or index’s performance, adverse price movements may cause a loss of capital.

Generally, investors will have no access to their principal for the tenor (or term) of the structured note, without incurring some risk of loss on the principal.

If the structured deposit or structured product issuer goes into debt default, the investor risks losing his/her entire principal.

Structured product is considered as complex product, investor should exercise caution in relation to the product, Structured Notes is for Professional Investor only. Note that specific structured products also carry product-specific risks. Please refer to the individual product pages for more information.

The information herein is for information only. DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this publication or its contents

Investment involves risks. The information provided is based on sources which DBS Bank Limited and DBS Bank (Hong Kong) Limited believe to be reliable but has not been independently verified. Any projections and opinions expressed herein are expressed solely as general market commentary and do not constitute solicitation, recommendation, investment advice, or guaranteed return. The above information does not constitute any offer or solicitation of offer to subscribe, transact or redeem any investment product. Past performances are not indicative of future performances. You should make investment decisions based on your own investment objective and experience, financial situation and particular needs. You should carefully read the product offering documentation, the account terms and conditions and the product terms and conditions for detailed product information and risk factors prior to making any investment. If you have any doubt on this material or any product offering documentation, you should seek independent professional advice.

Securities trading is an investment. The prices of stocks fluctuate, sometimes dramatically. The price of a stock may move up or down and may become valueless. It is as likely that losses will be incurred rather than profits made as a result of trading stocks. The investment decision is yours but you should not invest in any stock unless you have taken into account that the relevant stock is suitable for you having regard to your financial situation, investment experience and investment objectives.

Customers should be aware that the prices of the Callable Bull / Bear Contracts and Warrants may fall in value as rapidly as they may rise and holders may sustain a total loss of their investment. The Bank does not provide securities advisory service. Any person considering an investment should seek independent advice on the investment suitability when considered necessary.

Bonds and Structured Notes (“the Product”) are investment products and some of them may involve derivatives. The investment decision is yours but you should not invest in the Products unless DBS Bank (Hong Kong) Limited who sells them to you has explained to you that the Products are suitable for you having regard to your financial situation, investment experience and investment objectives. The Product is NOT equivalent to and is not treated as substitutes for time deposits, not principal protected.

Foreign exchange involves risk. Customers should note that foreign exchange may incur loss due to the fluctuation of exchange rate.

The information provided above have not been reviewed by the Securities and Futures Commission of Hong Kong or any regulatory authority in Hong Kong.

24-hour Hotline: (852) 2961 2338 Or let us contact you Other hotlines

Ways to get our Help & Support