Related insights

- Research Library10 Jul 2026

- Credibility of Fed reforms taskforce and US-Iran threats 10 Jul 2026

- Indonesia and Philippines markets: Testing market resilience 10 Jul 2026

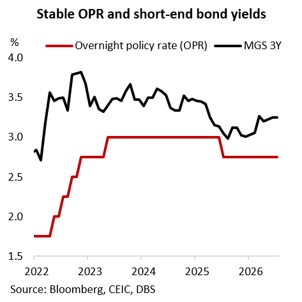

Bank Negara Malaysia (BNM) extended its monetary policy pause for a sixth consecutive meeting on July 9, maintaining its Overnight Policy Rate (OPR) at 2.75%. The decision reaffirmed that the central bank’s monetary policy stance remains appropriate amid resilient economic growth and price stability, despite ongoing geopolitical uncertainty. BNM acknowledged both upside and downside risks to its outlook, and will likely remain vigilant, particularly given the fragility of the US-Iran truce. However, barring another material shock, we expect BNM to remain on hold for the rest of 2026, keeping short-end bond yields stable.

BNM maintained a constructive outlook for 2026 growth, projecting the Malaysian economy to expand firmly within its 4-5% range. It highlighted resilient growth in 2Q26, supported by sustained domestic demand and firmer-than-expected exports amid global artificial intelligence-related tailwinds. Solid domestic demand, underpinned by a resilient labour market, supportive policies, and high investment realisation, will likely cushion the economy against external shocks. Although inflation rose in 2Q26 due to higher global costs, it remained contained at around its long-term average of 2.0% and within BNM’s expectations, due to subsidies and stable demand. While BNM sees elevated global commodity prices exerting upward price pressures, we expect policymakers to maintain a wait-and-see approach unless inflationary pressures become broad-based and persistent.

Although BNM did not explicitly address recent movements in the Malaysian ringgit in its monetary policy statement, we expect investors to remain assured by the central bank’s proactive commitment to ensuring orderly foreign exchange market conditions and its ongoing measures - including the Qualified Resident Investor (QRI) programme and engagements with government-linked entities - to encourage capital inflows, supported by Malaysia’s still-robust macroeconomic fundamentals. Malaysia’s foreign portfolio flows rebounded to positive territory of USD628mn in June 2026 from outflows of ~USD2bn in May. As such, we see little urgency for defensive policy rate hikes similar to those implemented by some regional central banks.

Topic

Explore more

E & S Macro StrategyGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related insights

- Research Library10 Jul 2026

- Credibility of Fed reforms taskforce and US-Iran threats 10 Jul 2026

- Indonesia and Philippines markets: Testing market resilience 10 Jul 2026

Related insights

- Research Library10 Jul 2026

- Credibility of Fed reforms taskforce and US-Iran threats 10 Jul 2026

- Indonesia and Philippines markets: Testing market resilience 10 Jul 2026