- Korea equities delivered the strongest performance among global equity markets this year, supported by easing political uncertainty and the new government’s structural reforms

- Tactical correction in November has created new entry opportunities for investors to participate in Korea’s growth story, underpinned by robust earnings fundamentals, attractive valuations, and corporate governance initiatives

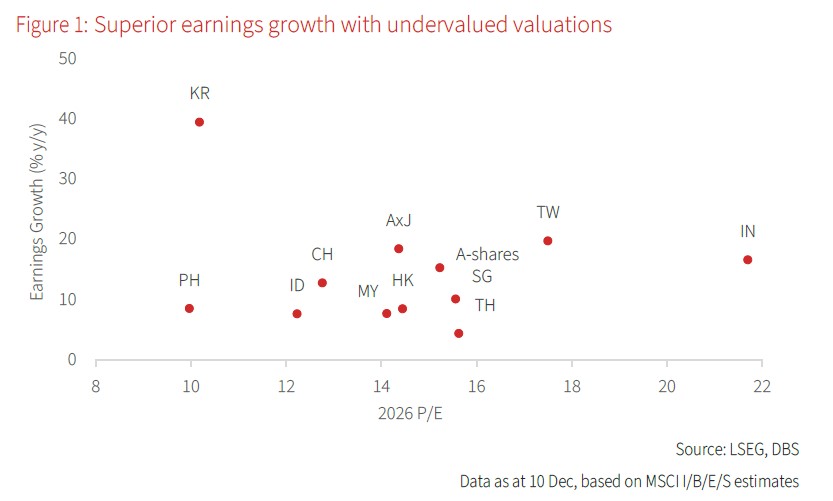

- The 2026 earnings growth forecast has been revised up sharply to 40% y/y from 17% in August, primarily driven by the technology sector. Other sectors are also experiencing earnings improvements, supported by a more favourable macro environment

- Select firms with stable earnings and attractive dividends, particularly those in dividend-centric sectors such as banks and communication services, are poised to benefit from corporate reforms

- Favour sectors demonstrating robust earnings growth with global competitiveness, including tech and industrials (defence, shipbuilding, and EPC)

Related insights

Tactical correction unlocks opportunities. Korea equities reached a new high on 3 Nov, delivering the strongest YTD performance of 76% among global markets. This outperformance was driven by diminishing political uncertainty, the new government’s structural reforms, and renewed foreign investors inflows. However, a sharp sell-off in November, triggered by the Fed’s hawkish stance and concerns on elevated tech valuations, led to significant foreign investors outflows. We view this pullback as a tactical correction rather than a sign of fundamental deterioration. The pullback should help reset market expectations, eliminating frothy positioning and creating a re-entry for investors who are positioned for Korea’s growth story.

Robust earnings and attractive valuations to underpin growth. The projected 2026 earnings growth for Korea equities has seen a remarkable upward revision from 17% in August to 40%, significantly outpacing regional peers. While the technology sector predominantly drives this revision on the back of global AI cycle, other sectors are also showing improved earnings. This is largely due to a reduction in US tariffs (from 25% to 15%) and an anticipated rebound in GDP growth in 2026.

Korea's GDP growth is projected to return to its normal trajectory of approximately 2% in 2026, up from an estimated low of 1% in 2025, driven by stronger domestic demand and a recovery in exports. Private consumption has begun its recovery in 2H25, supported by more accommodative fiscal and monetary policies and easing political uncertainties. Despite YTD performance, the market remains attractive at a 2026 P/E ratio of 9.8x, the lowest valuation among Asia ex-Japan (AxJ) markets.

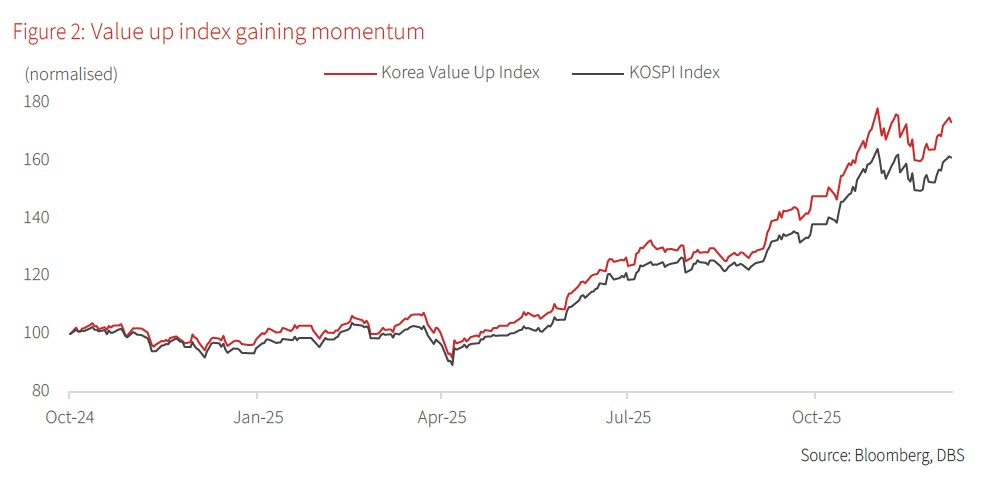

Accelerating corporate governance reforms. The government’s commitment to enhancing corporate governance remains a key catalyst for valuation re-rating. The first two amendments to the Commercial Act have been passed with most measures slated for implementation in 2H26. A third amendment mandating the cancellation of treasury shares is targeted for passage by the end of 2025. We anticipate these reforms will accelerate across firms in 2026, leading to improved ROE and P/B valuations for Korea equities.

Moreover, the government will implement separate lower taxation on dividend income next year for companies with a dividend payout ratio of 40% or higher, or those with a 25% payout ratio and a 10% or greater increase in dividends compared to the previous years. Select firms with stable earnings and attractive dividends will stand to benefit the most from these policies, notably from dividend-centric sectors like banks and communication services.

Easing KRW depreciation pressures in 2026, while recent weakness warrants attention. While recent KRW weakness — primarily due to resident outflows linked to foreign equity purchases — warrants attention, we expect KRW depreciation pressures to ease in 2026. The new trade deal will see South Korea invest USD350bn in the US over the next decade (USD200bn in direct investment and about USD20bn annually). This capital outflow appears manageable, given that approved direct investment to the US was USD22bn in 2024. Additionally, anticipated Fed rate cuts, a narrower KTB-UST yield gap, domestic economic recovery prospects, and a solid current account position should collectively support KRW stability and performance in 2026. To mitigate financial stability risks from excessive overseas investing, new regulations will require Korean retail investors to complete mandatory training and mock trading before accessing certain overseas-listed leveraged products, effective 15 Dec.

Given this backdrop, we prefer sectors with robust earnings growth on the back of structural reform and firms that are accelerating corporate governance reform. We outline the key structural sectors below:

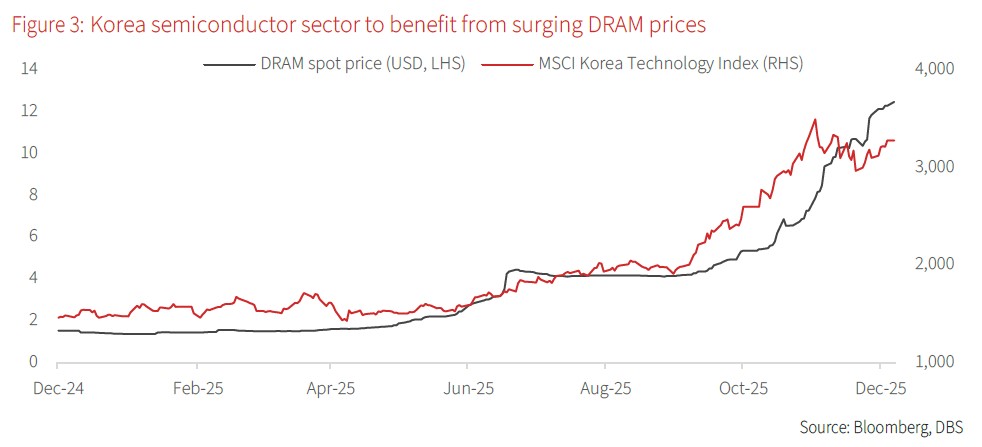

Technology: Korea’s semiconductor sector, a global powerhouse in DRAM, NAND, and high-band memory crucial for AI data centres, is entering a superior AI cycle. Despite market concerns regarding elevated AI valuation, the tech sector is forecasted to deliver an impressive earnings growth of 65% y/y in 2026, driven by surging AI-related demand and a significant uplift in memory prices. A prolonged supply deficit of memory chips, fuelled by insatiable demand, has propelled DRAM prices higher this year with the rally expected to extend through 2026. Despite lingering US tariffs, semiconductor exports to the US remain resilient, underscoring the sector’s critical role in the global technological landscape.

Industrials: The sector has outperformed this year, bolstered by a strong performance in defence and shipbuilding. While trading at +1 SD above 5-year historical P/E average, we believe the sector’s valuation is reasonable, given global competitiveness and its strong earnings fundamentals.

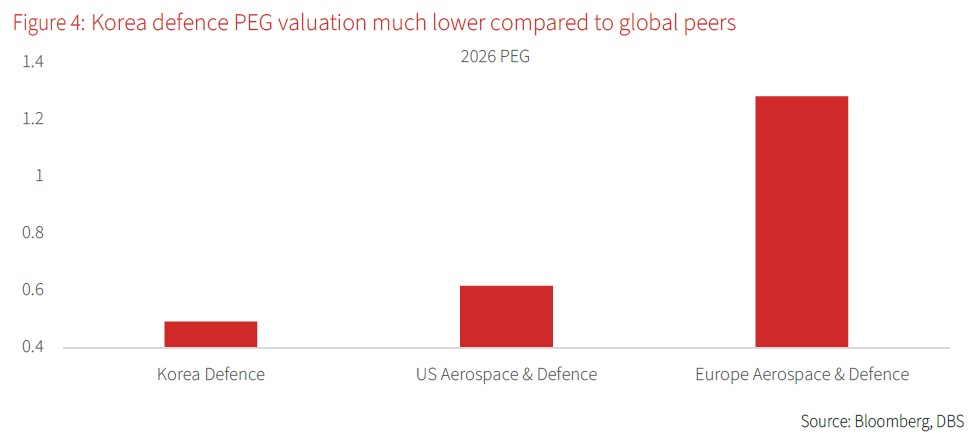

- Defence: As one of leading exporters with advanced technological capabilities, Korea defence firms are well-positioned to capitalise on Europe’s multi-year rearmament cycle, given the latter’s near-term limitations in scaling up production. Furthermore, Korea is anticipated to accelerate an increase in defence spending from the current 2.3% to 3.5% of GDP as soon as possible, in response to demands from President Trump. Despite YTD outperformance, Korea defence firms’ 2026 PEG remains lower than in US and Europe, supported by strong earnings growth and attractive valuation, underscoring market undervaluation. Potential deals with the Middle East and Latin America could be another driver for the sector.

- Shipbuilding and EPC: Korea’s shipbuilding and electrical, power, and construction (EPC) firms are expected to benefit from renewed US interest on its domestic shipbuilding and nuclear power plants. The US is anticipated to undergo substantial modernisation and innovation for the maritime sector, driven by strategic imperative to reclaim market share due to China’s dominant position. Concurrently, the US nuclear power sector (especially SMRs) is poised for accelerated growth due to the necessities of meeting escalating power demands from AI and securing supply chains away from Russia and China. Given the outstanding capabilities and technological expertise of Korean industrial players, strategic partnership and deals with the US and other developed nations are likely to significantly boost these industries, presenting compelling investment opportunities.

Korea’s rising influence in AxJ equities. The share of Korea equities in the AxJ Equity Benchmark Index has increased significantly to 14.5% from 7% on 11 Aug, as noted in our report “Korea Equities: From Turmoil to Take Off, Korean Market Roars On Reform”. Globally leading semiconductor players, Samsung Electronics and SK Hynix, are among the top 10 stocks in AxJ and account for 6% of the AxJ benchmark. With a robust earnings outlook, attractive valuation, supportive domestic policies, and strategic positioning in the global AI cycle and other structural growth themes, Korea equities are well-placed to accelerate further. These strengths reinforce our confidence in Korea’s growth story and bolster our positive view on the broader AxJ market.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.