- Trade tariffs dragged 1H25 vehicle sales in Europe and North America as vehicle affordability deteriorates

- Supply chain disruptions to deepen; we now project a decline of 2-3% in US and Europe new vehicle sales in 2025

- Demand recovery unlikely to be significant in the near term despite some tariff offsets

- Remain cautious on the global auto industry; estimate vehicle sales to contract by 1% in both 2025 and 2026

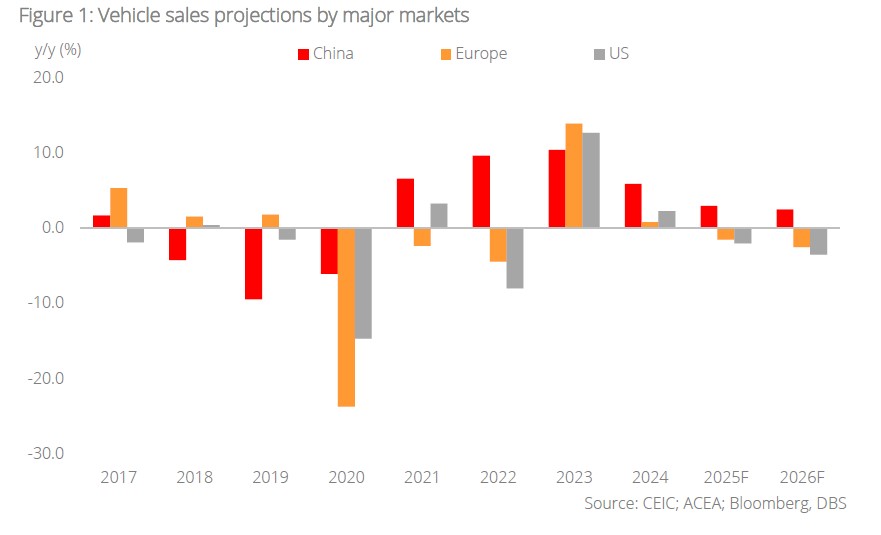

Vehicle sales in western markets feeling the tariff heat. The global auto market is shifting gears as tariffs and political uncertainty weigh on major auto market sales. According to COX Automotive, US light vehicle sales declined 4.2% y/y in June, following a 2.5% growth in May. 1H25 ended with a 4% y/y gain in light vehicle sales, driven largely by tariff-induced pre-emptive buying. Meanwhile, US electric vehicle (EV) sales posted two consecutive months of decline since April, signalling that higher vehicle prices are starting to dampen consumption, as the average transacted prices of all vehicles/EVs have risen by 0.3%/3.8% YTD in May. In Europe (EU + UK + European Free Trade Association), car sales totalled 5.6mn units in 5M25, remaining flat y/y, as macroeconomic uncertainty and tariff concerns curtailed consumer demand. Notably, petrol and diesel vehicle sales each declined by more than 20% y/y over the same period. EU car CPI index stood at an elevated 125 in Apr 2025, reflecting persistent concerns over vehicle affordability.

Major vehicle market shipments to slow in 2H as disruption deepens. Global auto supply chain disruptions are expected to intensify in 2H25, especially as the US concludes further trade negotiations. US consumers are likely to adopt a wait-and-see approach amid uncertainty surrounding trade policy, new vehicle prices, and model availability. New vehicle inventory in the US fell to 2.6mn units in May (average of consensus). Hence, full-year new vehicle sales in the US are projected to reach approximately 15.5mn units (seasonally adjusted) in 2025, representing a 2.5% y/y decline, while Europe’s sales are forecasted at about 12.7mn, down c.2%, suggesting that the bulk of the decline will be concentrated in 2H25. On the other hand, China’s auto industry continues to show resilience, especially the NEV sector, which is projected to post a y/y sales expansion of 17% to about 9mn units, even as intense price competition persists.

Demand recovery unlikely before 2026. The global auto industry is facing mounting headwinds as real demand weakens in response to rising vehicle prices, reduced affordability, and ongoing supply chain stress. Some mitigation may come from US policy measures, such as tariff offsets for domestically assembled vehicles, allowing duty-free parts imports of up to 3.75% of a car’s manufacturer’s suggested retail price until Apr 2026 and 2.5% until Apr 2027. Nonetheless, a material demand recovery in the US remains unlikely in the near term unless tariffs are eased, or trade deals are revised. As a result, we forecast global vehicle sales will decline by around 1% y/y in both 2025 and 2026.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.