- US/China: US headline CPI hit a three-year high, while core inflation stayed benign; China’s exports jumped amid resilient regional trade momentum and robust AI demand, while CPI data reflects subdued domestic consumption

- India: After RBI’s hawkish pause, we see two 25 bps hikes in 2HFY27 as inflation rises above target and spillover risks grow; strong 4QFY26 GDP growth aside, markets will watch FY27 risks from supply disruption and higher energy and food costs

- Singapore: Diverse capital inflows are sustained by strong macro fundamentals and unwavering stability despite increased geopolitical shocks; FDI inflows remain on an uptrend and will be supported by high competitiveness and future-ready strategies

- Indonesia: Following BI’s off-cycle 25 bps rate hike, we expect another 50 bps increase between 2Q-3Q26, with risks of more if the West Asia conflict spills over into 2H26, impacting inflation and currency movements

Related insights

- Booking Holdings23 Jun 2026

- Global Aerospace: Holding Altitude Amid Middle East Turbulence23 Jun 2026

- Research Library23 Jun 2026

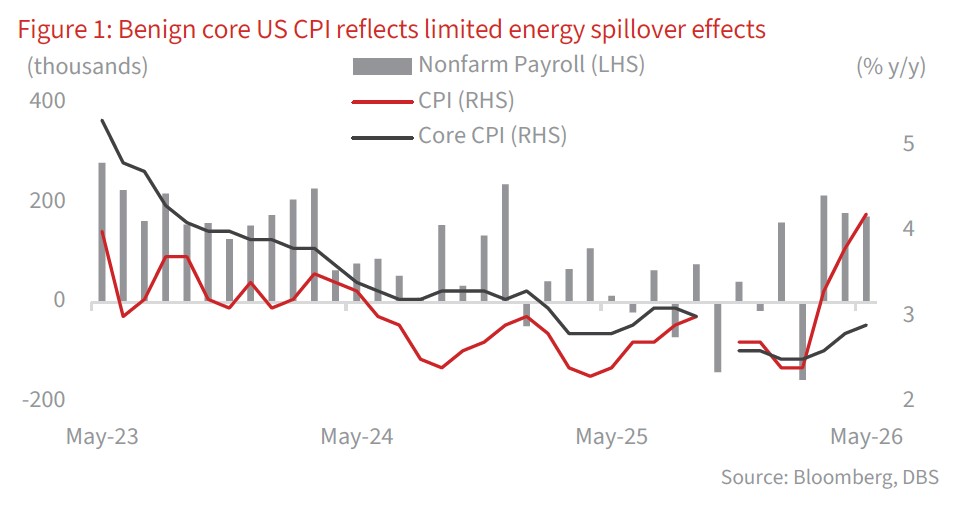

US/China: US headline CPI hit a three-year high, while core inflation stayed benign. The set of labour market data effectively ended all hope of Fed cuts, with the market pricing in a full cut by end-2026. Nonfarm payroll came in at 172k, beating consensus (88k) by a large margin. Moreover, there was 93k in net payroll revisions over the preceding two months. Amid steady unemployment, labour force participation, and still-elevated wage growth, the key takeaway is that the jobs market is doing well. That said, US headline CPI came in line with expectations at 4.2% y/y in May – the highest in three years - with the energy component driving the bulk of gains. The other components saw muted price increases, allowing core CPI to come in at 2.9% y/y. With no signs yet that price pressures are spreading, worries about imminent Fed hikes should ease. Against a backdrop of high inflation (due to energy prices) and no clear timeline for respite (with no Middle East deal announced yet), macro indicators are pointing towards an overheating US economy. This is unlikely to change even as new Fed Chair Kevin Warsh takes the helm at the upcoming FOMC meeting.

The 17 Jun meeting marks the official debut of newly confirmed Fed Chair Warsh, who faces the daunting task of establishing personal institutional integrity. Warsh will first need to balance President Donald Trump’s desire for rate cuts with the FOMC members’ increased data-dependent inclination towards a longer, more hawkish pause. He is likely to align with US Treasury Secretary Scott Bessent’s view that the wartime inflation surge was a transient blip that would naturally evaporate when the Middle East conflict ends, and the Strait of Hormuz reopens.

Meanwhile, China’s exports have jumped by 19.4% y/y in May. Beyond low base comparisons, resilient regional trade momentum and robust demand for AI products are serving as key catalysts. Outward shipments of hi-tech products have surged by 35.4%. External auto sales are soaring, as demand for Chinese EVs continues to boom alongside higher oil prices. An improving trade relationship with the US is providing an additional tailwind. Following the positive outcome of the recent Trump-Xi meeting, shipments to the US have climbed by 35.6%.

On the inflation front, PPI has grown by 3.9% y/y in May, reaching its highest level since Jul 2022. Among the key components, petroleum and natural gas prices, along with related processing costs, have surged by 35.7% and 18.4% respectively. However, downstream manufacturers and retailers are likely facing margin pressure from these rising input costs. CPI continues to lag well behind PPI amid still-tepid domestic demand. Headline consumer prices are holding at 1.2%, while core CPI has edged down to 1.1% from 1.2% in April. This indicates weak pricing power at the retail level and subdued domestic demand.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Booking Holdings23 Jun 2026

- Global Aerospace: Holding Altitude Amid Middle East Turbulence23 Jun 2026

- Research Library23 Jun 2026

Related insights

- Booking Holdings23 Jun 2026

- Global Aerospace: Holding Altitude Amid Middle East Turbulence23 Jun 2026

- Research Library23 Jun 2026