- The quantum computing industry is enjoying a burst of momentum amid continued inflows of private capital, government grants and policy support, as well as materialisation of preliminary commercial revenues

- Global investment in quantum tech start-ups surged over six-fold in 2025, led by a significant surge in private capital; US government offered USD2bn under the CHIPS act to nine quantum firms in return for minority stakes

- The path to genuine economic impact for quantum technology remains long and uncertain; existing industry leaders to remain in net loss, with negative free cash flows over the next few years

- Investors would be better served staying with diversified technology ecosystems to participate in any eventual breakthrough, alongside measured exposure to direct players

Since our last publication on quantum computing (“Quantum Computing: Visionary Technology, Distant Commercial Reality”, published 20 Jan 2026), interest in the quantum computing industry has strengthened as private capital continues to flood in, governments write large cheques, and the first commercial revenues begin to materialise. Strategic implications—ranging from challenging existing encryption standards and exposing banking system vulnerabilities, to unlocking substantial economic value in pharmaceuticals and financial modelling—are also increasingly intriguing. Yet the technology’s path to genuine economic impact remains long, uncertain, and strewn with formidable technical obstacles. Investors tempted by the hype would do well to temper enthusiasm with realism.

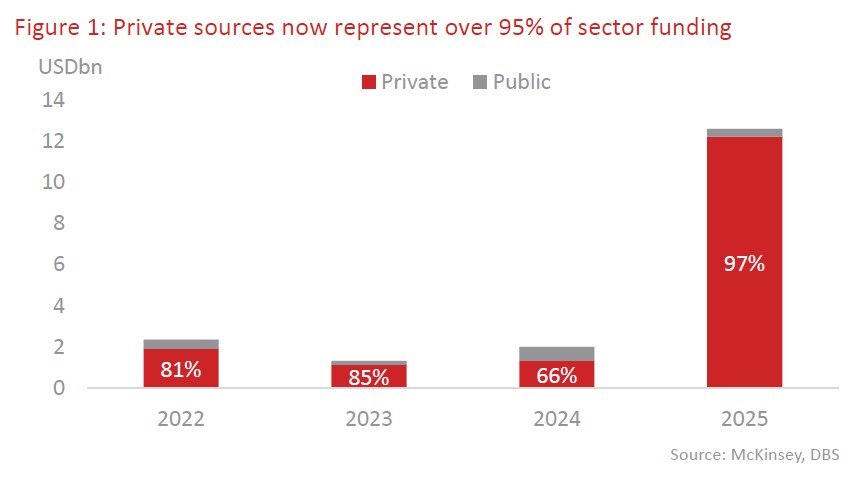

Private capital leads the charge. Global investment in quantum-tech start-ups reached USD12.6bn in 2025, a y/y increase of more than 6x. Private sources such as venture capital, private equity, corporations, and public markets account for 97% of total funding in the sector, up sharply from previous years. Public money, once dominant, has shrunk to a mere 3% of the pie. This shift suggests that quantum technology is gradually moving from laboratory curiosity towards something closer to a commercial proposition.

Government and corporate deals add ballast. In May, the US government signalled its strategic seriousness by offering USD2bn under the CHIPS and Science Act to nine quantum firms, taking minority stakes in return. IBM alone is set to receive USD1bn to build a domestic chipmaking venture; others, including GlobalFoundaries, D-Wave, Rigetti, and Infleqtion, will share the rest. Meanwhile, dealmaking is consolidating the supply chain. D-Wave’s USD550mn acquisition of Quantum Circuits in January gave it a second platform; IonQ’s USD1.8bn planned purchase of SkyWater Technology will secure US foundry capacity. Such moves are less about immediate profits and more about securing the hardware and expertise for scale.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.