- Asia’s structural opportunities to drive lifers’ growth; P&C underwriting performance supported by repricing actions and stable combined ratio

- Gains from high reinvestment yields expected to continue in 2H24 after multi-year lows and negative rates in developed countries

- We prefer selective names with enhanced shareholder returns

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Strong underwriting performance expected in 2H24. 1Q24 was a good start for the sector, evidenced by the key metrics of insurers under our coverage that surpassed market expectations. We expect the strong underwriting performance to continue in 2H24. In the life segment, the Asia market will continue to lead in 2H24 with high double-digit growth in value of new businesses (VNB), mainly driven by Hong Kong, China, and ASEAN, with their fast-growing affluent and middle-class customer bases and huge protection gap.

In Europe, we expect rising demand for savings due to better policy returns and a low base effect, supporting single-digit growth in premiums for European insurers’ life segment. In the P&C segment, we expect premiums to expand due to repricing actions. We forecast single-digit y/y growth in 2H24 for European insurers’ P&C segment, offsetting pressure from economic slowdown across major markets. We also expect their combined ratio (COR) to remain stable, with an improvement in the expense ratio offset by a higher loss ratio, reflecting our cautious view on natural disaster losses.

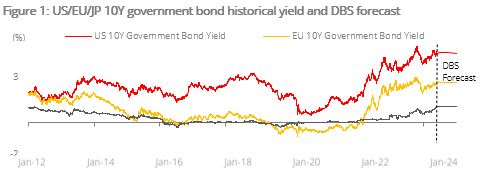

Investment returns to increase as interest rates remain elevated. After multi-year lows and negative interest rates in major developed countries, 10Y government bond yields are expected to stay elevated in 2H24F compared to the 10-year average (est. 4.5%/2.6%/1.1% on average in US/EU/JP in 2H24 vs. the 10-year average of 2.3%/0.5%/0.2%, respectively), despite 50 bps in policy rate cuts expected in the US and EU in 2H24. We expect gains from higher reinvestment yields to continue accruing in average portfolio yields, with new money invested at rates higher than those of the current portfolio, translating into better investment results for insurers under our coverage.

Selective names with enhanced shareholder returns. In the past two quarters, most large-cap insurers have updated their capital management policies and payout guidance. Global and regional insurers under our coverage guided for a total payout target of c.75% based on core net profit/net free surplus generation, including the majority by dividend payout and the rest by share buybacks. Based on our estimates, global and regional insurers offer a c.3%-6% dividend yield supplemented by a c.1.5%-5% capital return yield. The resulting combined yield would range from 6.9%-8.0%.

We believe the market will continue to favour stocks that could surprise on the upside from capital returns, and that global insurers remain a good source of reliable and defensive yield. We are turning increasingly positive towards regional and Chinese insurers and believe they are good choices as both dividend plays and for alpha-seeking investors. Reasons for this include 1) secular growth opportunities in the Asian life insurance sector which allow regional and Chinese insurers to deliver superior growth ahead of global peers, 2) we are less concerned over the China property sector since the Chinese Government’s policy support has surpassed expectations, and 3) China insurers are offering an attractive dividend yield of >7%.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025

Related insights

- Global Credit 1Q26 - Hedge and Seek12 Dec 2025

- Korea Equities: Growth, Reform, and Resilience12 Dec 2025

- FX Tactical Ideas: USD to Turn Sideways Post-FOMC12 Dec 2025