Related insights

- Research Library20 Apr 2026

- Agricultural Bank of China20 Apr 2026

- Ferrari NV20 Apr 2026

What Happened

The Iran conflict has introduced a critical inflection point for global markets, with the energy channel emerging as the dominant transmission mechanism. Disruptions around the Strait of Hormuz have pushed oil prices higher, lifting inflation expectations and complicating the global growth outlook. As we head into the second month of the conflict, economic pressure builds globally. The key market debate now shifts to what the implications are for equity markets from the risks of a prolonged conflict versus a potential de-escalation — with two distinct and binary scenarios emerging.

What It Means

Scenario 1: De-escalation and Gradual Normalisation

In a constructive outcome where the US and Iran reach an agreement to de-escalate, the Strait of Hormuz could begin to normalise over the next one to two months. Under this scenario, the impact on global growth is likely to remain limited. Energy prices may retrace from recent highs, although they are likely to remain above pre-conflict levels given that physical supply chains and inventories will take time — potentially a few months — to fully stabilise.

Scenario 2: Prolonged Conflict and Sustained Energy Shock

In a more adverse scenario where the US and Iran fail to reach an agreement and the Strait of Hormuz remains disrupted for several months, the risk of further damage to energy infrastructure from bombardment in the Gulf states will rise. The risks to the global economy would also increase materially with each passing week. Sustained elevated energy prices would act as a tax on global growth, disproportionately impacting energy-importing economies across Asia and emerging markets.

What differentiates energy and defence in the current context is that they are not binary trades tied to one outcome — they are beneficiaries across both scenarios, albeit with varying degrees of upside.

- In Scenario 1, energy benefits from a higher price floor, earnings resilience, and under-ownership, while defence is supported by sustained geopolitical risk and budget expansion.

- In Scenario 2, both sectors see accelerated upside, driven by supply shocks (Energy) and prolonged military engagement (Defence).

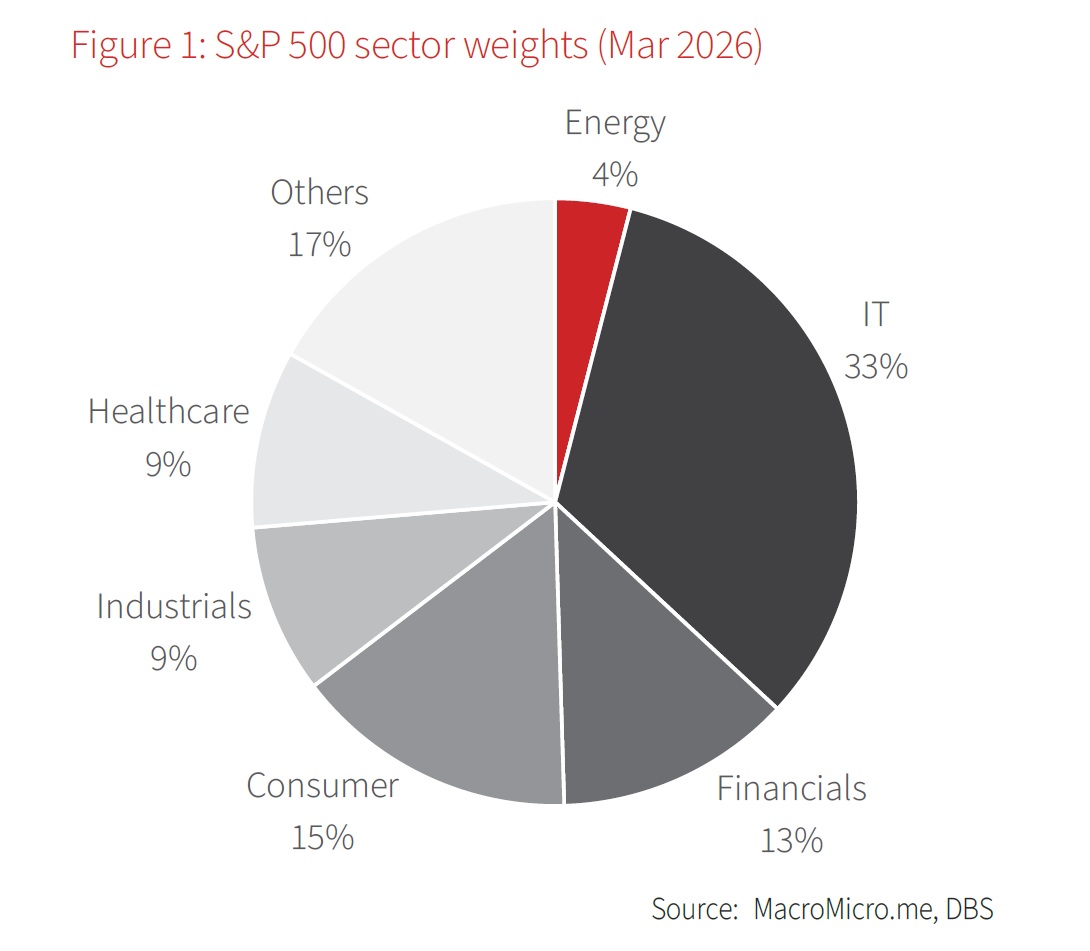

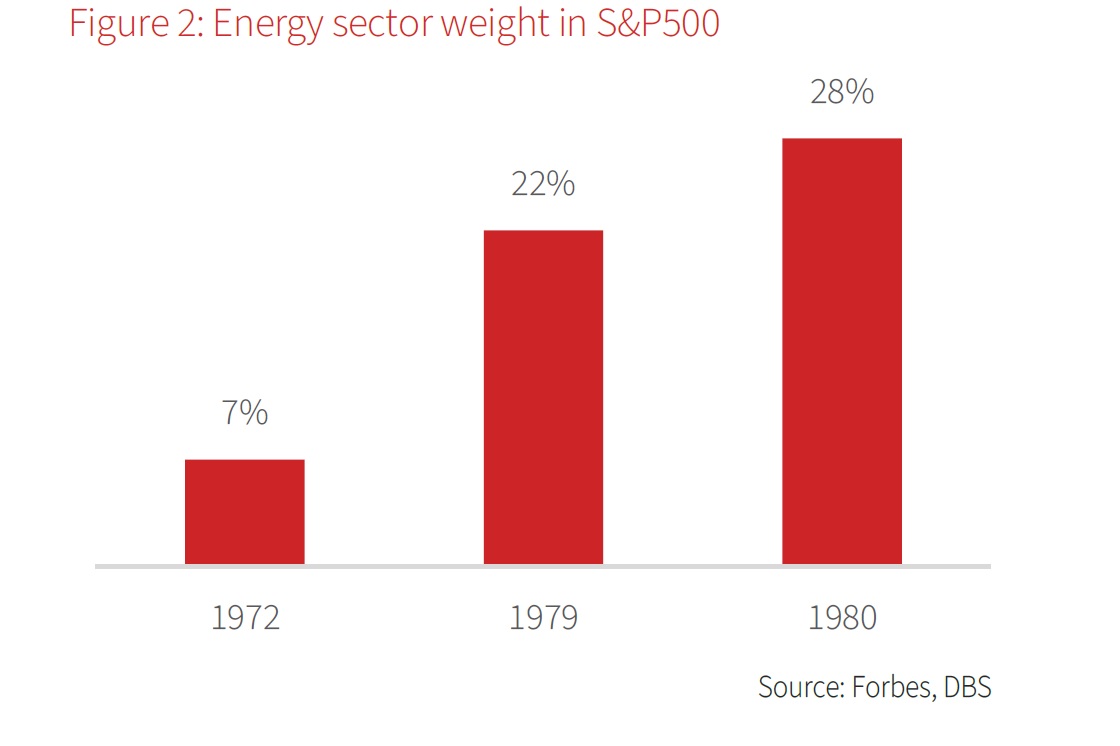

Despite the recent move in oil prices, energy remains underrepresented in equity indices, constituting only 4% of the S&P 500 as of Mar 2026, up from 2.8% in Dec 2005, but still well below historical peaks. By comparison, during the 1970s energy crisis, energy’s weight surged from 7% of the S&P 500 in 1972 to a peak of 28% in 1980.

How to Invest

The market outcome remains largely binary at this point and US-Iran actions over the next few days and weeks could help narrow the scenarios and shape a clearer narrative for market direction. A swift de-escalation reinforces the current narrative of resilient growth and corporate earnings, while a prolonged conflict risks triggering a more fragile macro backdrop and defensive positioning. While markets may be focused on whether the Iran conflict resolves quickly or escalates further, from an equity allocation perspective, energy and defence may stand out as consistent tactical and structural winners across both paths.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related insights

- Research Library20 Apr 2026

- Agricultural Bank of China20 Apr 2026

- Ferrari NV20 Apr 2026

Related insights

- Research Library20 Apr 2026

- Agricultural Bank of China20 Apr 2026

- Ferrari NV20 Apr 2026